Retiring at 60 with $500,000 in superannuation is possible for Australians aiming to live simply, especially if they are homeowners with no major debts. However, since you won’t be eligible for the Age Pension until 67, you must self-fund at least seven years of living expenses. Whether $500K is enough depends on your annual spending, investment returns, and overall financial .

Quick Overview

- You must self-fund your retirement for 7 years before Age Pension eligibility

- $500K could support a modest lifestyle or part-time work could stretch it further

- Your investment returns and cost of living will significantly affect outcomes

How Long Will $500K Last?

Here’s a simplified estimate assuming modest investment returns:

| Annual Spending | Estimated Duration |

|---|---|

| $30,000 | ~17–20 years |

| $40,000 | ~13–15 years |

| $50,000 | ~10–12 years |

🧠 Assumes ~2.4% real return (after inflation), compounding annually.

What Kind of Lifestyle Can You Afford?

Based on the ASFA Retirement Standard (2024–25):

- A modest lifestyle requires ~$32,000/year

- A comfortable lifestyle requires ~$51,000/year (single person)

👉 $500K may support a modest to moderate lifestyle until Age Pension kicks in — particularly if:

- You own your home

- You have no major debts

- You keep a tight budget

The 7-Year Gap to Age Pension

You become eligible for the Age Pension at age 67.

Until then, you need to rely on:

- Super withdrawals

- Investment income

- Casual or part-time work

- Personal savings

Ways to Stretch $500K Further

✅ Downsize or Relocate

Moving to a more affordable area can reduce costs and free up extra cash.

✅ Part-Time Work

Even 2–3 days a week could help delay dipping into your super too fast.

✅ Use a Transition to Retirement (TTR) Strategy

If still working, you can access some super while still contributing to it.

✅ Invest Smartly

Avoid overly conservative options. Aim for a balanced portfolio to outpace inflation.

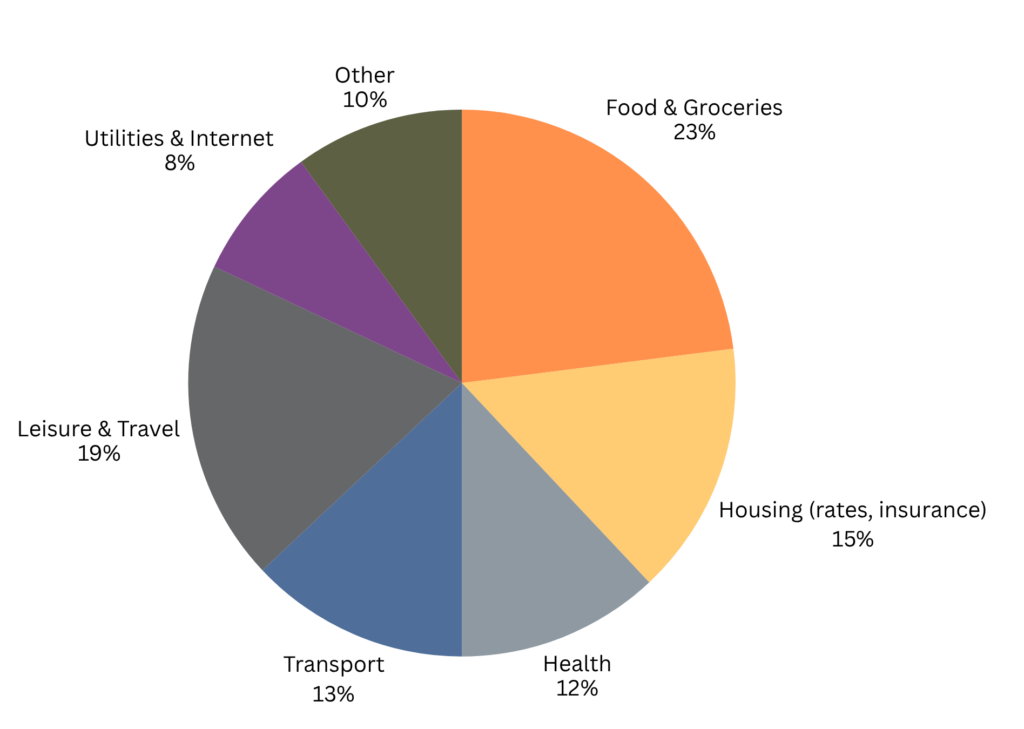

📊 Realistic Spending Breakdown (Annual Estimate)

According to ASFA, a modest retirement lifestyle includes:

| Category | Annual % | Notes |

|---|---|---|

| Food & Groceries | 23% | Cooking at home, limited dining out |

| Housing (rates, insurance) | 15% | Assuming you own your home |

| Health | 12% | Includes private health insurance |

| Transport | 13% | Basic car expenses or public transport |

| Leisure & Travel | 19% | Domestic travel and hobbies |

| Utilities & Internet | 8% | Electricity, water, phone, internet |

| Other | 10% | Clothing, household, unexpected costs |

Graphic: A pie chart visual showing this breakdown.

Pros & Cons of Retiring at 60 with $500K

| Pros | Cons |

|---|---|

| More time for leisure and lifestyle | Must fund 7+ years before Age Pension |

| Access to super at 60 | Risk of outliving savings |

| Can live modestly and debt-free | Limited buffer for emergencies |

✅ Final Verdict: Can You Retire at 60 with $500K?

Yes — if you:

- Own your home

- Can live on ~$30K–$40K/year

- Plan to bridge the 7-year pension gap

- Possibly work part-time or use a TTR strategy

You won’t be living lavishly, but a comfortable, simple life is possible with planning.