Retiring at 60 with $240,000 in super or savings might seem like a challenging goal, but it’s possible with careful planning, budgeting, and using the right strategies. If you’re asking “Can I retire at 60 with $240K in Australia?”, the answer is yes, but it requires discipline and smart financial management.

In this guide, we’ll break down how far $240K can stretch, what kind of lifestyle you can expect, and how you can make your money last until the Age Pension begins at 67.

What Happens Financially When You Retire at 60 with $240K in Australia?

At age 60, you can access your super tax-free, but you’ll need to self-fund your lifestyle until you’re eligible for the Age Pension at 67.

Here’s the financial breakdown:

- Preservation Age: You can access your super at 60, but you must ensure you don’t run out of funds before Age Pension eligibility.

- Self-Funding: For the first seven years (60–67), you must fund your lifestyle entirely, using only your super balance or other savings.

Can you retire at 60 with $240K and make it work? Yes, but only with strategic budgeting and disciplined withdrawals.

What Retirement Costs Look Like in Australia

According to the ASFA Retirement Standard (March 2024):

- A modest lifestyle for a single person costs around $32,000/year

- A comfortable lifestyle costs around $51,000/year

These estimates assume homeownership and public healthcare. A modest lifestyle includes essentials such as food, transport, and utilities, but excludes luxuries like overseas travel and premium private healthcare.

With $240,000, you’ll need to live below the modest standard ideally around $26,000–$28,000/year to make it last until the Age Pension begins. This ensures your super lasts during the 60–67 gap and beyond.

How Long Will $240K Last in Retirement?

Let’s look at a projection assuming:

- Annual withdrawals: $28,000–$31,000

- 3% annual growth on your super

| Year | Starting Balance | Withdrawal | Growth (3%) | Ending Balance |

|---|---|---|---|---|

| 60 | $240,000 | $28,000 | $6,300 | $218,300 |

| 61 | $218,300 | $28,500 | $5,800 | $200,700 |

| 62 | $200,700 | $29,000 | $5,000 | $176,800 |

| 63 | $176,800 | $29,500 | $4,300 | $151,600 |

| 64 | $151,600 | $30,000 | $3,700 | $125,300 |

| 65 | $125,300 | $30,500 | $2,600 | $97,700 |

| 66 | $97,700 | $31,000 | $2,000 | $68,900 |

| 67 | $68,900 | $10,000 | $1,900 | $55,300 |

By the time you reach 67, the Age Pension will ease the financial burden, and your super will continue to last longer with smaller withdrawals.

What Happens at 67?

At 67, you qualify for the Age Pension, which will significantly reduce your reliance on super withdrawals. The full Age Pension for a single person is currently around $29,000 per year (as of July 2024). This support will provide financial security, especially after your super is mostly drawn down.

Current Full Age Pension Rates (July 2024):

- Single: ~$29,000/year

- Couple (combined): ~$43,800/year

How to Make Retiring at 60 with $240K Work

1. Own Your Home

Owning your home outright removes one of the largest living expenses housing. Without rent or mortgage payments, your $240K will stretch much further, providing you with more funds to cover daily essentials.

2. Set Up an Account-Based Pension

Convert your super into an account-based pension (ABP). This ensures a regular, tax-free income and keeps your super invested, allowing it to grow while you draw down smaller amounts each year. It also helps you qualify for the Age Pension sooner.

3. Spend Below the ASFA Modest Standard

Aim to live on $26,000–$28,000 per year instead of the full $32,000. This means cutting back on luxuries like expensive travel, eating out, or shopping. Use government concessions, public transport, and community events to reduce costs further.

4. Keep Some Super in Conservative Growth Investments

Invest a portion of your super in low-risk, income-producing assets, like bonds or conservative managed funds, to preserve your capital. Ensure you have 1–2 years’ worth of living expenses in cash for emergencies or market fluctuations.

5. Consider Part-Time or Casual Work

Part-time or casual work in your early 60s even for just a few hours a week can significantly reduce pressure on your super. It can help preserve your balance and improve your Age Pension eligibility by reducing your assets.

Lifestyle Expectations on $240,000

| Category | What to Expect |

|---|

| Housing | Must own your home |

| Travel | Local only, limited interstate trips |

| Food & Essentials | Covered with careful budgeting |

| Healthcare | Use public system, limit private insurance |

| Extras | Few, must be planned in advance |

Pitfalls to Avoid When Retiring at 60 with $240k

- ❌ Taking large lump sum withdrawals drains your balance too quickly

- ❌ Assuming the Age Pension starts earlier than 67

- ❌ Underestimating inflation or rising health costs

- ❌ Holding all funds in cash may lose value over time

- ❌ Failing to get financial advice for drawdown strategies and Centrelink planning

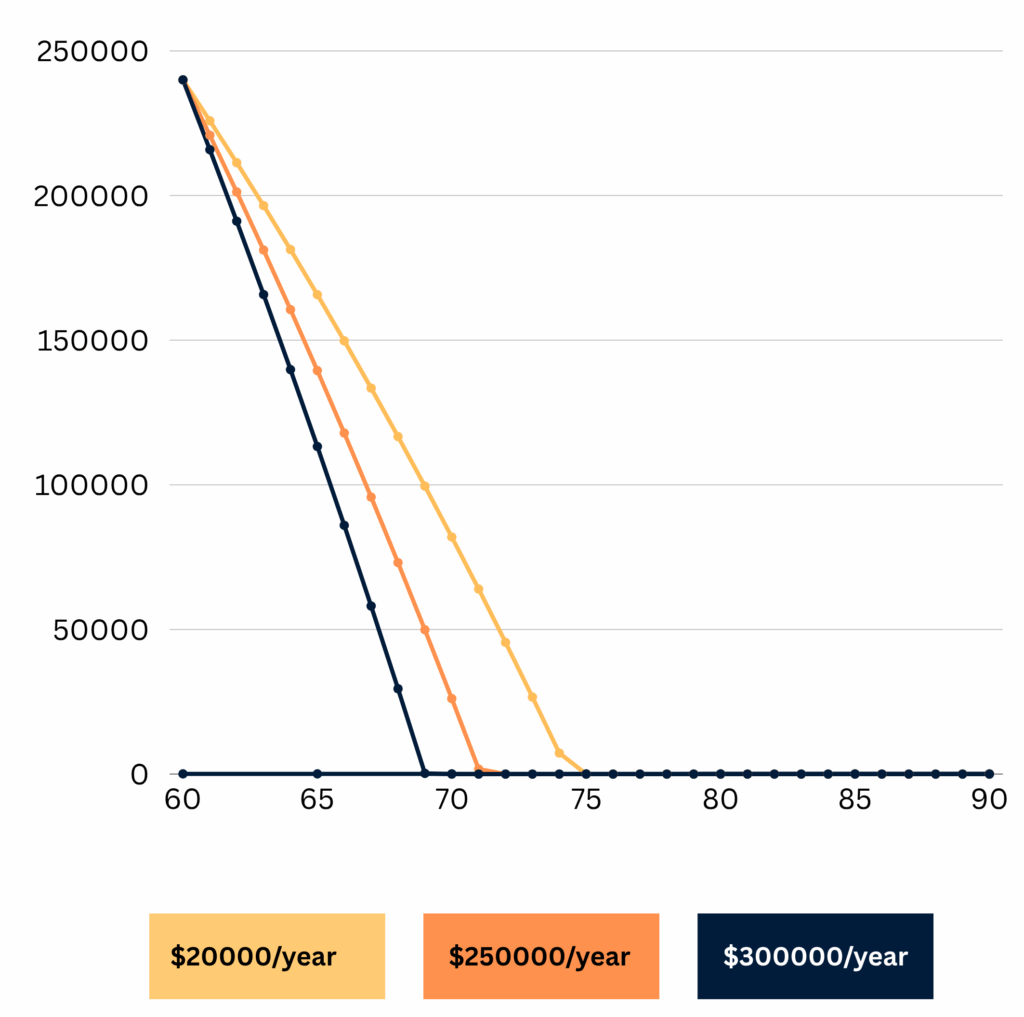

This Line Chart Shows $240K depletion from age 60 to 90 under 3 spending levels.

Retiring at 60 with $240k? Wealthlab Can Help You Maximise It

At Wealthlab, we specialise in helping Australians retire confidently even on smaller balances. We’ll model your income, align your goals with your budget, and help you access every benefit available.

✔️ Super income stream & drawdown planning

✔️ Budget modelling for modest retirement

✔️ Centrelink & Age Pension guidance