Retiring at 62 with $365,000 in super is genuinely achievable for many Australians. At this balance and age, the question is not really whether you can retire. It is how you invest $365K to make retirement income last, which pension structure makes the most sense, and what the five-year gap to the Age Pension actually costs you in practical terms.

That is what this article covers. The real numbers, the investment options worth understanding, how the different pension structures compare, and what most people in this position get wrong before they stop work.

What $365K at 62 Actually Means

At 62, you are two years past preservation age. You can access your super tax-free if you have retired from the workforce. The Age Pension does not start until 67, so there is a five-year gap to self-fund.

$365K is a more comfortable base than the $260K to $280K range people retiring at 60 are often working with. Five years to bridge instead of seven. A larger opening balance. More runway before the Age Pension arrives and more options for how to invest what you have.

According to the ASFA Retirement Standard (February 2026), a single homeowner needs $35,199 a year for a modest lifestyle and $54,240 for a comfortable one. For couples, those figures are $50,866 and $77,375 respectively. At $365K, a single homeowner spending $38,000 to $42,000 a year through the gap years is in workable territory, provided the money is invested properly.

How Long Will $365K Last from Age 62?

The projection below assumes an account-based pension with a 5% net annual return and spending between $38,000 and $42,000 a year. This reflects a balanced investment mix, which is a realistic assumption for a retirement portfolio at this age.

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 62 | $365,000 | $38,000 | $16,350 | $343,350 |

| 63 | $343,350 | $38,500 | $15,243 | $320,093 |

| 64 | $320,093 | $39,000 | $14,055 | $295,148 |

| 65 | $295,148 | $39,500 | $12,782 | $268,430 |

| 66 | $268,430 | $40,000 | $11,422 | $239,852 |

| 67 | $239,852 | Pension starts | ~$220,000 |

At 67, roughly $220,000 remains and the Age Pension begins. For a single homeowner, this balance falls below the full pension assets test threshold of around $314,000 (current as at May 2026, Services Australia), which means near-full pension entitlements are very likely.

Combined income at 67, from near-full single pension of approximately $29,754 a year plus modest drawdown from $220,000, puts annual retirement income in the range of $40,000 to $50,000. That supports a comfortable retirement for a homeowner with no debt.

Please note: All figures are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

How to Invest $365K in Retirement: The Options Worth Understanding

This is where most people in this position do not spend enough time before they retire. How your $365K is invested in retirement has a larger impact on how long it lasts than almost any other decision you make.

Account-Based Pension

Converting your super into an account-based pension is the standard starting point for most retirees. You roll your super balance into a pension phase, which means investment earnings become tax-free (rather than taxed at 15% in accumulation phase). You draw a regular income, control the amount you withdraw above the legislated minimums, and the remaining balance stays invested.

The minimum annual drawdown rates for account-based pensions are set by the government:

- Age 60 to 64: 4% of balance per year

- Age 65 to 74: 5% of balance per year

- Age 75 to 79: 6% of balance per year

On $365K, the minimum drawdown at 62 is $14,600 a year. Most people in retirement need more than this, so drawing above the minimum is standard. The key is not drawing so much above the minimum that you burn through the balance before the Age Pension arrives.

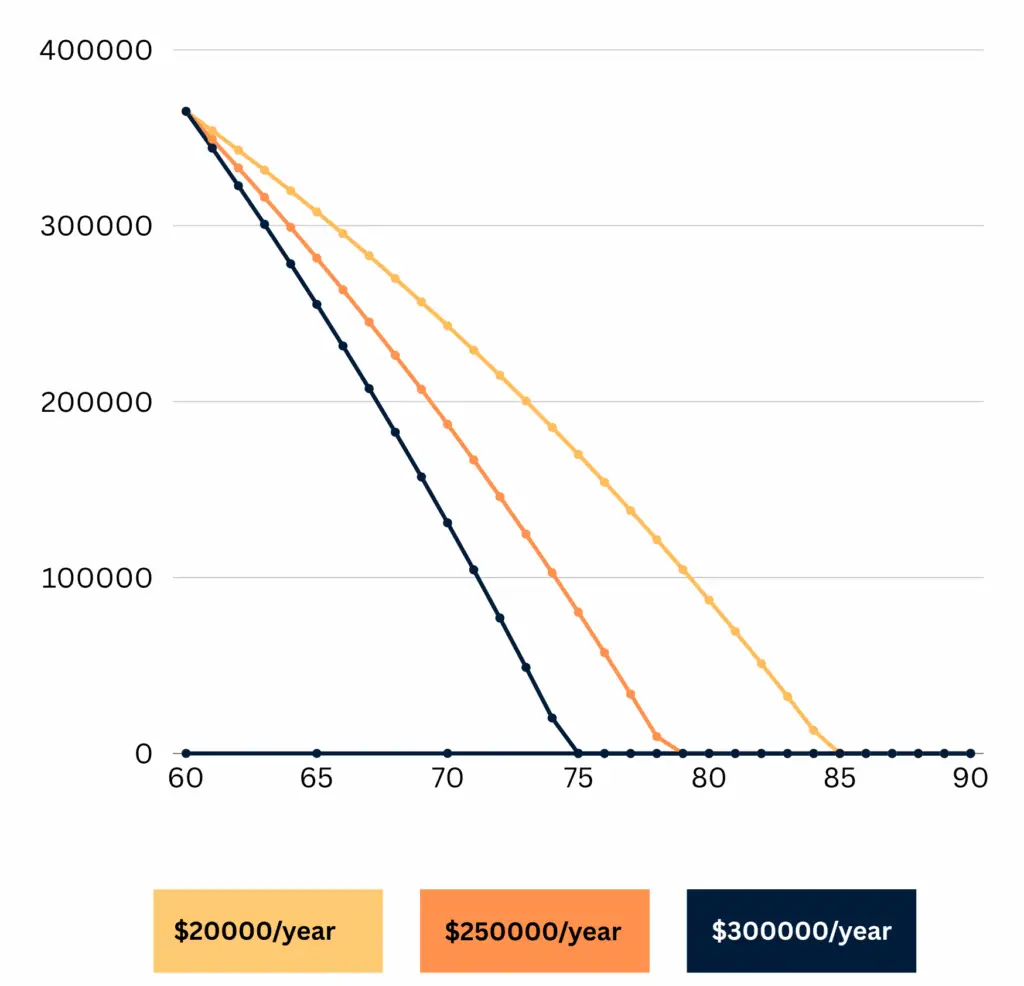

This Line Chart Shows How $365K Super Depletion from Age 60 to 90 Visualising how your balance depletes under different lifestyles helps you compare your options. Spending less can significantly extend the life of your super.

Which Investment Option Inside Your Pension?

This is where the “best way to invest” question gets practical. The most common options inside super or pension accounts are:

Conservative or capital stable: Mostly bonds, cash and fixed interest. Lower returns, lower volatility. Typically 2% to 3.5% net return in recent years. At this return rate, your balance loses ground to inflation even before withdrawals are considered. Generally suitable for very short investment horizons or money needed within one to two years.

Balanced: A mix of roughly 50% to 70% growth assets (shares, property) and the remainder in defensive assets. Returns have typically been in the 5% to 7% range over rolling ten-year periods. This is the most common choice for retirees in their 60s, and the assumption used in the projection above.

Growth or high growth: 80% to 100% in shares and property. Higher long-term returns, typically 7% to 9% over ten-year periods, but with more short-term volatility. Not suitable for money you may need to draw within two to three years, but worth considering for a portion of a larger balance.

Phil made a point worth understanding here: most super funds label their products in ways that do not reflect what is actually inside them. In Episode 22 of the Wealthlab Podcast, he noted that a “balanced fund is not a true balanced fund with most of these funds these days. They are every day of the week a growth fund that they slap the name balanced on.” Knowing what your fund actually holds, not just what it is called, matters. Watch Episode 22 on YouTube.

Scott covered the long-term impact of investment choice in retirement directly in Episode 1. A growth portfolio through a long retirement funded noticeably better than a conservative one, and the difference compounds over time. Watch Episode 1 here.

Cash Reserve Strategy

Rather than putting everything into one option, many retirees in this position keep one to two years of spending in cash or a high-interest savings account outside super. This covers near-term living costs without needing to sell growth assets during a market dip. The remaining balance stays invested in a balanced or growth option.

This approach means a market fall in year two of retirement does not force you to sell at a low point to fund groceries. It gives the growth portion of your portfolio time to recover. Speaking with a financial adviser about structuring this for your specific balance and spending is worth doing.

Which Pension Option Is Best?

The “best” pension option at 62 depends on how much flexibility you want, whether you are also receiving Centrelink payments, and your tax position.

Account-based pension is the most flexible. You control drawdowns, the balance remains part of your estate if you pass away, and earnings are tax-free. The trade-off is that the balance fluctuates with markets and there is no guarantee it will not run out.

Annuity (also called a lifetime income stream) provides guaranteed income for life or a fixed term regardless of market performance. You give up flexibility and the balance does not remain in your estate, but you cannot outlive the income. These are more useful as a component of a strategy rather than a complete solution, and they interact with the Age Pension assets test in ways that can be advantageous. This is an area where professional advice is worth getting before committing.

Account-based pension plus partial annuity is a structure some retirees use to guarantee a base income while maintaining flexibility with the remainder. The right split depends on your spending needs, other assets and Age Pension eligibility.

For a thorough look at how the Age Pension interacts with different retirement income structures, Phil and Dan covered real case studies in Episode 10 of the Wealthlab Podcast. Watch Episode 10 on YouTube.

Our pension and Centrelink page has more on how different retirement income structures affect Age Pension entitlements.

Age Pension Rates for 2026

Current Age Pension rates as at May 2026 (Services Australia):

- Single (including supplements): approximately $29,754 a year

- Couple combined (including supplements): approximately $44,856 a year

Updated each March and September by the Australian Government.

With roughly $220,000 remaining at 67 after five years of drawdown from $365K, a single homeowner will very likely receive near-full pension entitlements. Getting advice on how to position your assets in the two to three years before turning 67 is genuinely worthwhile. How your super and other assets are structured at pension age affects what you receive and when.

Episode 9 of the Wealthlab Podcast covers a real case study where super fund advice caused an avoidable Age Pension loss. The difference between independent advice and fund-level advice on this topic is significant. Watch Episode 9 here.

The Five-Year Gap: What Retiring at 62 Versus 67 Costs

The five-year gap between 62 and 67 is the central planning challenge at this balance. Understanding what it actually costs is more useful than a vague awareness that it exists.

At $40,000 a year spending with 5% net returns on the invested balance, the five-year gap from 62 to 67 draws the balance down from $365K to approximately $220,000. That is $145,000 drawn down over five years, partially offset by investment returns on the remaining balance.

The upside of having $220,000 still invested at 67 is that it continues growing even as the Age Pension supplements income. Combined drawdown of 3% to 4% from $220,000 plus near-full pension gives a total annual income of $37,000 to $39,000. With modest spending increases factored in, this supports a comfortable retirement well into the 80s for most homeowners.

The psychology of moving from an income dropping into your account every fortnight to that stopping is something Phil raised directly in Episode 1 of the podcast. It is real, and it affects how people manage those early retirement years. Watch Episode 1 here.

What to Do Before You Retire at 62 with $365K

Check your investment option now, not after you retire. Many people spend their accumulation phase in a default option that is not optimal for drawdown. Reviewing this and understanding what you actually hold inside your fund is a basic first step.

Consolidate super accounts if you have more than one. Multiple accounts mean multiple sets of fees eating into your balance. Consolidating before retirement is a simple admin task with a real dollar benefit over time.

Consider whether catch-up concessional contributions make sense in the final year or two of work. If your total super balance is under $500,000 and you have unused concessional cap from the past five financial years, you can contribute more than the standard $30,000 annual cap. At a top marginal tax rate, these contributions can be a meaningful way to boost your balance and reduce tax in your final working years. Phil and Dan walked through the catch-up contribution rules with a real worked example in Episode 10 of the podcast. Watch Episode 10 here.

Run your own numbers with the free Wealthlab super calculator to see how different investment returns and spending levels affect your balance through the gap years.

Our retirement planning page and superannuation page cover the broader structural decisions worth getting right before you retire.

FAQ: Retiring at 62 with $365K in Australia

Can I retire at 62 with $365K in Australia? For a single homeowner, yes. At $38,000 to $42,000 a year spending and 5% net return in an account-based pension, $365K leaves roughly $220,000 at age 67 when the Age Pension starts. Combined income at 67 from pension plus drawdown can support a comfortable retirement for a homeowner with no debt.

What is the best way to invest $365K in retirement? Most retirees in their early 60s use an account-based pension with a balanced investment option as the core structure. Keeping one to two years of spending in cash outside the pension gives stability while the growth portion remains invested. Whether a partial annuity makes sense alongside the pension depends on individual circumstances and is worth discussing with a financial adviser.

Which pension option is best for someone retiring at 62? An account-based pension offers the most flexibility and keeps the balance accessible and in your estate. A lifetime annuity offers guaranteed income but less flexibility. Many people use both, keeping a base guaranteed income through an annuity and maintaining flexibility through an account-based pension. The right split depends on your spending needs, other assets and how you want to interact with the Age Pension.

How much will I have at 67 if I retire at 62 with $365K? At $40,000 a year spending and 5% net return, approximately $220,000 at 67. Combined with near-full Age Pension entitlements, annual income from 67 is in the range of $37,000 to $42,000 for a single person, depending on drawdown rate from the remaining balance.

Which super funds offer the best transition to retirement options? TTR pensions are available through most large industry and retail super funds. The key variables are investment options available inside the fund, fees, and flexibility of drawdown. The fund’s “balanced” label does not always reflect what is actually held inside the product, which affects your real return. Comparing funds on investment options and fees, rather than just labels, is the more useful exercise. A financial adviser can compare specific funds against your situation.

Will I qualify for the Age Pension if I retire at 62 with $365K? Almost certainly by 67. Drawing down over five years from $365K typically leaves a balance approaching or below the full pension assets test threshold for a single homeowner, currently around $314,000 (May 2026). Your home is exempt. Whether you receive the full or part pension depends on all your assets and income at the time of application, not just super.

What is the minimum drawdown from an account-based pension? At age 62 to 64, the legislated minimum is 4% of your opening balance each year. On $365K that is $14,600 a year. You can draw more than the minimum, but most retirees need to in order to fund their actual lifestyle. Keeping drawdowns close to the minimum in the early years preserves more for later.

Is $365K enough for a couple to retire at 62? As a combined balance, it is workable for a modest retirement, but comfortable retirement as defined by ASFA at $77,375 a year for a couple would stretch this balance considerably. Couples in this position generally benefit from one partner continuing to work part-time through the early 60s, or from maximising the lower-balance partner’s super before retiring.

What to Do Next

If you are approaching 62 with around $365K in super, the most valuable step before you retire is to get clear on three things: what investment structure your money will be in during retirement, how you will manage the five-year gap before the Age Pension, and how your assets are positioned at 67. General projections are useful context, but your specific numbers, spending, tax position and other assets all affect the outcome.

Not sure where you stand? or take the free Wealthlab retirement quiz for a general read on your retirement position. Or book a free, no-pressure chat with the Wealthlab team to talk through the investment and pension structure questions with someone who handles this every day.