If you’re 65, own your home, and have $300,000 in superannuation, you’re in a stronger position than you might think.While $300k isn’t a large nest egg by Australian standards, owning your home significantly lowers your annual expenses. With smart planning, frugal living, and the support of the Age Pension from 67, you can retire at 65 and do so with confidence.

Let’s explore what retirement looks like with this setup, and how to make it work long term.

What Happens Financially at 65?

At 65, you’re eligible to access your super tax-free even if you keep working. But if you’re retiring now, there’s a catch:

You’ll need to self-fund your lifestyle for two years until Age Pension begins at 67.

That means your $300k will need to cover approximately $60,000–$65,000 in those two years alone. After that, the Age Pension can ease the burden, and you can draw less from super each year.

✅ Owning your home gives you a huge head start.

✅ Keeping spending modest is the next key step.

What Retirement Costs Look Like

The ASFA Retirement Standard (March 2024) provides widely accepted cost-of-living estimates:

- Modest lifestyle (single homeowner): ~$32,000/year

- Comfortable lifestyle (single homeowner): ~$51,000/year

These figures assume:

- You live independently

- Use public healthcare

- Have no housing costs

💡 With $300k and a paid-off home, you can realistically aim for a modest lifestyle especially if you live on $28,000–$30,000 per year and access the Age Pension after 67.

What Happens at Age 67?

Once you turn 67, you become eligible for the Age Pension, as long as you meet income and assets test limits.

Current Full Pension Rates (July 2024):

- Single: ~$29,000/year

- Couple (combined): ~$43,800/year

If you draw down your super carefully between 65 and 67, you’ll likely qualify for a part or full pension, giving your retirement income a big lift and helping your super last longer.

How to Make Retirement Work on $300k at 65

1. Own Your Home

With no rent or mortgage, you’ve eliminated your biggest expense. This gives you flexibility and security, allowing you to live comfortably on a more modest income.

2. Convert Super Into a Super Income Stream

Rolling your super into an account-based pension allows for regular payments, is tax-free from age 60, and gives your savings a chance to grow —while maintaining Age Pension eligibility.

3. Stick to a Modest Lifestyle Budget

Aim to spend between $28,000–$30,000 per year. You can live well by accessing public healthcare, using concession cards, and minimising unnecessary purchases. This lifestyle keeps your savings intact longer.

4. Keep Some Super in Growth Investments

Don’t go all-in on cash. Holding 30–50% of your super in conservative growth or income-producing assets helps your balance grow steadily and combat inflation. Keep 1–2 years of spending in cash for stability.

5. Use the Age Pension Strategically

From 67 onward, the Age Pension will likely cover more than half your living costs. Combined with smaller super withdrawals, this can stretch your funds well into your 80s or beyond.

Projecting the Numbers

Here’s a rough example of how it might play out if you retire at 65 and spend ~$30,000/year:

| Age | Super Balance | Annual Drawdown | Earnings (3%) | End Balance |

|---|---|---|---|---|

| 65 | $300,000 | $30,000 | $7,500 | $277,500 |

| 66 | $277,500 | $30,000 | $6,900 | $254,400 |

| 67 | $254,400 | $12,000 (reduced drawdown with Age Pension) | $6,300 | $248,700 |

| 70 | ~$230,000 | Ongoing drawdowns ~10–15k/year | Ongoing growth | ~$200,000 |

| 80+ | ~$100,000 | Smaller top-ups | +Age Pension | Balanced income |

Even with modest returns, your super can support you well into your 80s, especially if your Age Pension kicks in after 67.

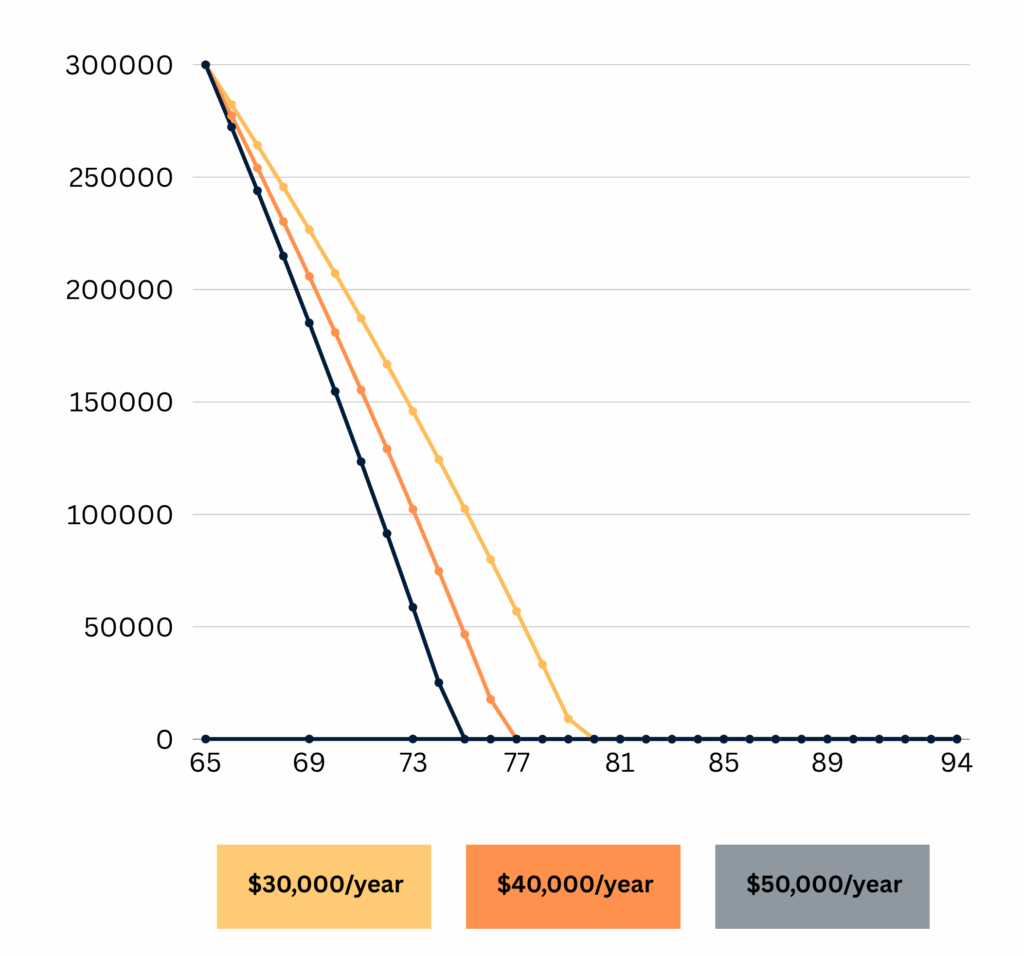

This Line Chart Shows Depletion of $300K over time under different spending levels.

Common Mistakes to Avoid

❌ Spending too much before Age Pension kicks in

❌ Leaving your super in all-cash (loses value to inflation)

❌ Taking lump sums for big-ticket items

❌ Not planning for healthcare or rising living costs

❌ Assuming Age Pension will cover everything from day one

Final Thoughts: Yes, You Can Retire

Retiring at 65 with $300k and no housing costs is possible and more realistic than many people think. The key is structure: use your super wisely, limit early withdrawals, and transition into Age Pension smoothly.

You may not live a luxury lifestyle, but you can have a secure, independent, and fulfilling retirement.

This Pie Chart Shows Budget allocation for a $25K–$30K yearly lifestyle.

Need Help Navigating Your $300k Retirement?

At Wealthlab, we help Australians:

✔️ Maximise super drawdowns

✔️ Build Age Pension strategies

✔️ Stretch savings for decades

✔️ Plan for the unexpected

📞 Book your free 30-minute consultation today. Let’s make your retirement plan real not just a guess.