Retire at 60 with $285K might seem challenging, especially when compared to media headlines suggesting a million-dollar superannuation balance for a comfortable retirement. But the truth is, retiring at 60 with $285K in Australia is possible with the right planning, budgeting, and a modest lifestyle.

In this guide, we’ll explore how far $285K can go, the lifestyle you can afford, and how to manage your super and income before the Age Pension begins at 67.

What Happens Financially When You Retire at 60 with $285K?

Reaching age 60 is a major milestone in retirement planning. Here’s what happens financially:

- You reach your preservation age, so you can access your super tax-free if retired.

- However, you’re still seven years away from qualifying for the Age Pension, which starts at 67.

- This means you will need to self-fund your lifestyle for at least seven years, covering housing, food, healthcare, and other living costs.

With $285K, you can make it work, but it will require careful planning to ensure your funds last until the Age Pension starts.

What Retirement Costs Look Like When You Retire at 60 with $285K

According to the ASFA Retirement Standard (March 2024), the cost of retirement can vary based on your lifestyle choices:

- Modest lifestyle (single): ~$32,000/year

- Comfortable lifestyle (single): ~$51,000/year

These figures assume you own your home and rely on public healthcare. If you can keep your annual expenses around $28,000–$30,000/year, you will likely have enough to make $285K last until 67, assuming moderate spending and careful withdrawals.

How Long Will $285K Last When You Retire at 60 with $285K?

Here’s a basic projection assuming annual withdrawals of $28,000 and a 3% annual return on your super:

| Year | Starting Balance | Withdrawal | Growth (3%) | Ending Balance |

|---|---|---|---|---|

| 60 | $285,000 | $28,000 | $8,550 | $265,550 |

| 61 | $265,550 | $28,500 | $7,900 | $245,950 |

| 62 | $245,950 | $29,000 | $7,200 | $224,150 |

| 63 | $224,150 | $29,500 | $6,500 | $201,150 |

| 64 | $201,150 | $30,000 | $5,400 | $176,550 |

| 65 | $176,550 | $30,500 | $4,400 | $150,450 |

| 66 | $150,450 | $31,000 | $3,000 | $122,450 |

| 67 | $122,450 | $10,000 | $1,700 | $114,150 |

This projection shows that $285K can sustain you until 67, but you’ll need to budget carefully to make it work.

What Happens at 67 When You Retire at 60 with $285K?

At 67, you will be eligible for the Age Pension, which will supplement your income. The full Age Pension for a single person is approximately $29,000 per year (as of July 2024).

By this point, your super balance will be lower, but the Age Pension will help reduce your reliance on super withdrawals, providing financial security.

Current Full Age Pension Rates (July 2024):

- Single: ~$29,000/year

- Couple (combined): ~$43,800/year

What Happens Financially When You Retire at 60?

Turning 60 is a significant moment in the Australian retirement system. At this age:

- You’ve reached your preservation age, which means you can access your super tax-free if retired.

- However, you’re still seven years away from qualifying for the Age Pension (which begins at 67).

This means you’ll need to cover all your living expenses housing, food, healthcare, and lifestyle from your super, personal savings, or other income sources for those seven years.

To make retirement work at 60, your plan must address:

- When and how Age Pension support will begin

- Whether you own your home

- How much you need to spend annually

- How to manage your super withdrawals efficiently

What Retirement Costs Look Like When You Retire at 60

According to the ASFA Retirement Standard (March 2024), here’s a breakdown of the estimated costs for a single person in retirement:

- Modest lifestyle: ~$32,000/year

- Comfortable lifestyle: ~$51,000/year

These figures assume you own your home, rely on public healthcare, and live independently without financial dependants.

With $285,000 in super, if you can keep your annual spending around $28,000–$30,000, you can comfortably cover most of your needs until the Age Pension begins at 67. However, it’s important to adjust your budget, especially in the early years, to avoid depleting your super too quickly.

How Long Will $285,000 Last When You Retire at 60?

Here’s an example projection assuming annual withdrawals of $28,000 and a 3% annual investment return:

| Year | Starting Balance | Withdrawal | Growth (3%) | Ending Balance |

|---|---|---|---|---|

| 60 | $285,000 | $28,000 | $8,550 | $265,550 |

| 61 | $265,550 | $28,500 | $7,900 | $245,950 |

| 62 | $245,950 | $29,000 | $7,200 | $224,150 |

| 63 | $224,150 | $29,500 | $6,500 | $201,150 |

| 64 | $201,150 | $30,000 | $5,400 | $176,550 |

| 65 | $176,550 | $30,500 | $4,400 | $150,450 |

| 66 | $150,450 | $31,000 | $3,000 | $122,450 |

| 67 | $122,450 | $10,000 | $1,700 | $114,150 |

This shows that $285,000 can last from 60 to 67, but you’ll need to keep a careful watch on your withdrawals to make it last through the early retirement years.am management, $285k can last through your early retirement phase, with a small balance remaining when Age Pension begins.

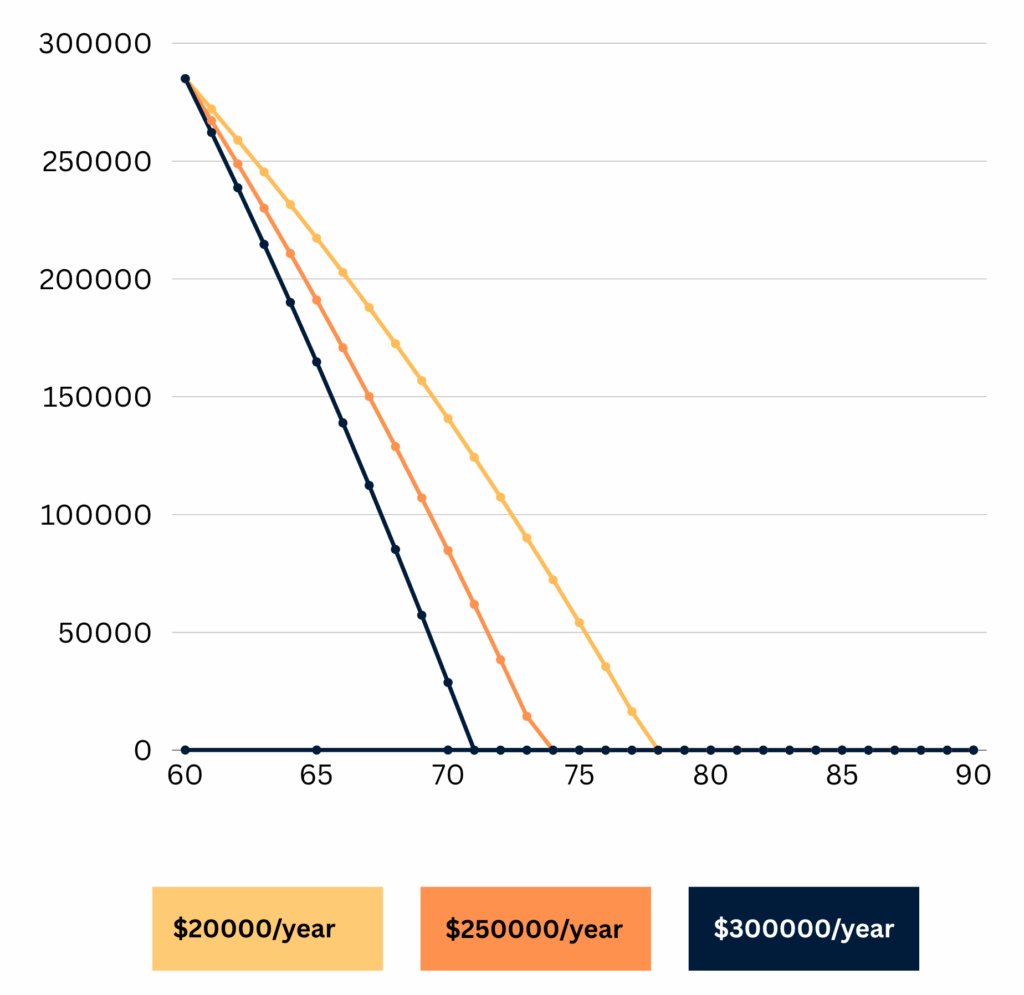

This line chart showing how your super balance changes from age 60 to 90 at spending levels of $20K, $25K, and $30K/year. This visual helps you easily compare lifestyle trade-offs over time.

💸 Budgeting a Modest Retirement Lifestyle

Here’s a sample annual budget for someone spending ~$25K per year and owning their home:

| Category | % of Budget |

|---|---|

| Living Essentials | 50% |

| Healthcare | 20% |

| Leisure & Travel | 15% |

| Emergencies | 10% |

| Miscellaneous | 5% |

A retirement like this is modest but realistic for many Australians particularly if you’re debt-free and already own your home.

What Happens at Age 67?

At 67, you become eligible for the Age Pension, assuming you meet the income and assets test. With your super balance drawn down to ~$125k, there’s a high chance you’ll qualify for at least a part pension possibly the full rate.

Current Full Pension Rates (July 2024):

- Single: ~$29,000 per year

- Couple (combined): ~$43,800 per year

Once you start receiving the Age Pension, your need to withdraw from super decreases significantly helping stretch your remaining savings well into your 80s or beyond.

How to Make Retirement Work on $285,000

1. Own Your Home Before You Retire

Paying off your home is essential. Without rent or mortgage costs, your basic living expenses drop, making a modest retirement much more achievable. If you’re mortgage-free at 60, you’ve already removed one of your biggest financial hurdles.

2. Use a Super Income Stream

Set up an account-based pension to draw regular income from your super. This approach is tax-free after age 60, offers flexible withdrawals, and helps preserve eligibility for the Age Pension by keeping your balance managed.

3. Live Below the Modest Lifestyle Standard

Aim to spend around $28,000–$30,000 annually rather than the full $32,000. Using public healthcare, accessing government concessions, and limiting discretionary expenses can make a big difference.

4. Maintain Conservative Growth Investments

Keep a portion of your super in balanced or income-focused investment options to generate stable returns. Hold 1–2 years’ worth of expenses in cash or liquid assets to buffer against market drops and cover short-term needs.

5. Consider Flexible Work or Side Income

Even part-time or freelance work until age 62–63 can delay super withdrawals, help preserve capital, and increase your future Age Pension. Plus, it keeps you active, engaged, and connected to community or purpose.

Common Mistakes to Avoid

❌ Withdrawing large lump sums too early

❌ Underestimating how long the 60–67 period can feel

❌ Overestimating future investment returns

❌ Ignoring health costs or insurance premiums

❌ Failing to get retirement income advice early

Retiring on $285k? Wealthlab Can Help You Build a Plan

At Wealthlab, we specialise in helping Australians with modest super balances retire confidently. Whether you’re planning ahead or retiring now, we’ll help you stretch your savings, optimise your drawdown strategy, and understand what support you can access.

- Superannuation drawdown planning

- Age Pension eligibility & modelling

- Retirement lifestyle budgeting

📞 Book a free consultation now to plan your next steps