If you’re approaching 60 with $270,000 in super and wondering whether you can retire, the short answer is: yes, for the right person in the right circumstances. But the more useful question is not whether you can retire at 60 with $270K. It’s whether your $270K can actually last long enough to carry you through to the Age Pension at 67 and beyond.

That’s what this article focuses on. Not just whether retirement at 60 with $270K is technically possible, but how to make the money last, what the real numbers look like, and what most people in this position get wrong before they hand in their notice.

What Retiring at 60 Actually Means in Australia

Sixty is preservation age for anyone born after 1 July 1964. Once you stop working and retire, you can access your super tax-free through an account-based pension. That part is straightforward.

The harder part is the seven-year gap between retiring at 60 and the Age Pension starting at 67. During those seven years, every dollar of living expenses comes from your own pocket. No government supplement, no pension, just your super and whatever else you’ve saved.

That gap is what makes retiring at 60 with $270K a meaningful planning challenge. It’s not insurmountable, but it demands a clear picture of your numbers, not optimism.

How Long Does $270K Last If You Retire at 60?

The projection below assumes an account-based pension with a 5% net annual return and spending between $28,000 and $31,000 a year. This growth rate reflects a balanced investment mix, which is more realistic for a retirement portfolio than the near-cash rates sometimes used in generic projections.

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 60 | $270,000 | $28,000 | $12,100 | $254,100 |

| 61 | $254,100 | $28,500 | $11,278 | $236,878 |

| 62 | $236,878 | $29,000 | $10,394 | $218,272 |

| 63 | $218,272 | $29,500 | $9,439 | $198,211 |

| 64 | $198,211 | $30,000 | $8,411 | $176,622 |

| 65 | $176,622 | $30,500 | $7,306 | $153,428 |

| 66 | $153,428 | $31,000 | $6,121 | $128,549 |

| 67 | $128,549 | Pension starts | ~$118,000 |

At 67, there is still roughly $118,000 remaining and the Age Pension begins supplementing income. For a single homeowner, that balance falls comfortably under the full Age Pension assets test threshold of around $314,000 (current as at May 2026, Services Australia), which means near-full pension entitlements are likely.

Please note: All figures are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

What Retirement Costs Look Like in 2026

According to the ASFA Retirement Standard (February 2026 update), annual retirement costs for a homeowner are:

- Single, modest lifestyle: $35,199

- Single, comfortable lifestyle: $54,240

- Couple, modest lifestyle: $50,866

- Couple, comfortable lifestyle: $77,375

At $28,000 to $30,000 a year, the scenario above sits below the ASFA modest standard for a single person. That is the honest read on retiring at 60 with $270K. It is a modest retirement for a debt-free homeowner, not a comfortable one in ASFA’s terms. For couples, the numbers are tighter still unless both partners contribute to the balance.

What ASFA’s figures do not fully capture is that actual spending for many retirees in their early 60s tends to be lower than benchmark figures suggest, particularly for people who own their home, have no commuting costs and have already paid off consumer debt. Real-world retirement spending often only climbs sharply in the mid-70s when healthcare costs increase.nce. A lower super balance at pension age often means more Age Pension. The system is designed that way.

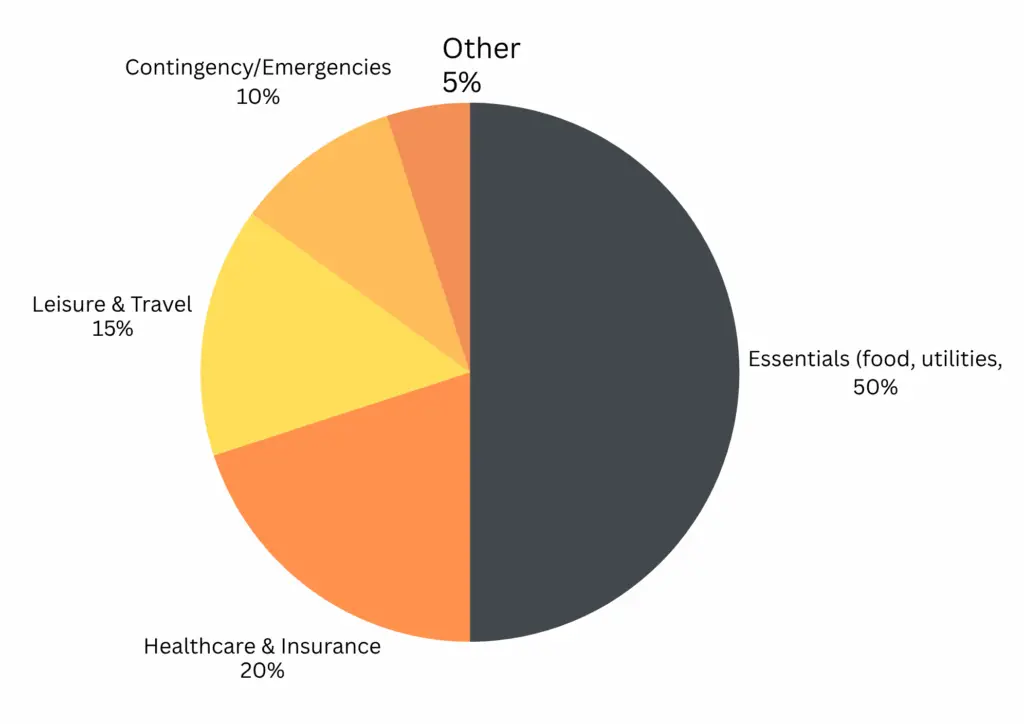

Sample $25K Budget Breakdown (if you own your home)

Here’s how a modest $25,000/year lifestyle might look:

| Category | % of Budget |

|---|---|

| Essentials (food, utilities, transport) | 50% |

| Healthcare & Insurance | 20% |

| Leisure & Travel | 15% |

| Contingency/Emergencies | 10% |

| Savings Buffer | 5% |

This assumes you own your home and maintain a modest lifestyle.

The Age Pension: What Changes at 67

Current Age Pension rates as at May 2026 (Services Australia):

- Single (including supplements): approximately $29,754 a year

- Couple combined (including supplements): approximately $44,856 a year

These are updated each March and September.

Once the Age Pension kicks in, the dynamics shift completely. Someone spending $30,000 a year who qualifies for near-full single pension has most of their annual costs covered by the government payment alone. Their remaining super balance then only needs to fund the gap, which dramatically extends how long the money lasts.

With roughly $118,000 at 67 and full pension eligibility, combined income for a single retiree is in the range of $35,000 to $40,000 a year from pension plus modest drawdown. That is a workable retirement income for a homeowner with no debt.

Phil and Dan walked through exactly this kind of scenario with real numbers in Episode 10 of the Wealthlab Podcast, including how the assets test and income test interact with different super balances at 67. Worth a listen if you want the full breakdown. Watch Episode 10 on YouTube.

Five Ways to Make $270K Last Longer in Retirement

Own your home before you retire. This one point changes the numbers more than almost anything else. Without rent or a mortgage, your annual spending drops significantly, and the projections above become far more achievable. If you are carrying a mortgage into retirement at 60, clearing it first or at least substantially reducing it is worth serious consideration before you stop work.

Set up an account-based pension, not a lump sum withdrawal. Converting your super into a regular income stream rather than taking it as a lump sum keeps your money invested and growing while you draw it down. It also gives you a clear picture of your drawdown rate and helps prevent the common mistake of spending too freely in year one.

Keep growth assets in your investment mix. Retiring does not mean switching everything to cash. In fact, doing so is one of the most common ways people end up underfunded a decade into retirement. Inflation at 3% a year means cash is losing real value every year. An investment mix that includes growth assets alongside more stable income assets is generally worth maintaining through the early years of retirement. Scott covered this directly in Episode 1 of the Wealthlab Podcast, looking at what happens to retirement outcomes when a growth portfolio is compared to a conservative one over a long retirement. Watch Episode 1 here.

Aim to spend below the ASFA modest standard in the early years. $26,000 to $28,000 a year in your early 60s preserves more capital for the later years when healthcare costs tend to rise. Seniors card discounts, bulk billing, pensioner concessions on utilities and public transport all contribute to keeping spending down without a dramatic lifestyle sacrifice.

Consider part-time work in your early 60s. Even $15,000 to $20,000 a year in part-time income between 60 and 63 means you draw much less from super during that period, leaving a significantly larger balance by 67. It can also improve your Age Pension position, as a higher balance at pension age that is then drawn down still gets you to the same entitlement point, just with more left over. Many people find part-time work in familiar roles or consulting a useful transition rather than a full stop.

Want to model how different spending levels and work scenarios affect your specific balance? The free Wealthlab super calculator takes about two minutes and gives a clearer picture than any general table can.

The Biggest Retirement Mistakes at This Balance Level

Taking a large lump sum in year one. A kitchen renovation, a holiday, helping the kids with a house deposit. These are all understandable, but pulling $30,000 to $50,000 from a $270K base in year one is extremely difficult to recover from. The compounding effect of that decision plays out over 20 to 30 years.

Assuming the Age Pension is automatic. It is not. You need to apply through Centrelink, and Centrelink will assess your assets and income at the time of application. Getting advice on how to structure your super and other assets before you hit 67, not the week after your birthday, makes a meaningful difference to what you receive and when.

Forgetting about healthcare costs in retirement. Medical expenses are low for most people in their early 60s, but they tend to rise significantly in the 70s and 80s. Building a buffer for this from the start is far smarter than assuming it will not be an issue. Phil raised this directly in Episode 19 of the podcast when he and Scott unpacked why 34% of retirement savings typically go to healthcare. Watch Episode 19 here.

Not getting independent advice. Super fund advice is not the same as independent financial advice, and what your fund tells you can sometimes cost you significantly, including affecting your Age Pension entitlements in ways you do not see coming. Episode 9 of the Wealthlab Podcast covers a real case study where a super fund’s advice caused an avoidable Age Pension loss. Watch Episode 9 here.

Our retirement planning page and pension and Centrelink page cover both the structural and government support side of this in more detail.

FAQ: Retiring at 60 with $270K in Australia

Can I retire at 60 with $270K in Australia? For a single homeowner spending around $28,000 to $30,000 a year, retiring at 60 with $270K is workable. It funds a modest retirement during the seven-year gap before the Age Pension starts at 67, provided you manage drawdowns carefully and keep your super invested with some growth exposure.

How long will $270K last in retirement? At $28,000 to $30,000 a year spending and 5% net return inside an account-based pension, $270K leaves approximately $118,000 remaining at age 67. From there, the Age Pension supplements income and the remaining balance extends well into the 80s for most homeowners.

What lifestyle can I expect when I retire at 60 with $270K? A modest lifestyle for a homeowner with no debt. Groceries, utilities, healthcare, some domestic travel and modest social spending. Below ASFA’s modest standard of $35,199 a year, but achievable and comfortable for many people whose actual retirement spending is lower than benchmarks suggest.

Will I qualify for the full Age Pension if I retire at 60 with $270K? Almost certainly by 67. Drawing down gradually over seven years from $270K typically leaves a balance well under the full pension assets test threshold for a single homeowner, currently around $314,000 (May 2026). Your home is exempt from the test. A financial adviser can help you structure assets to maximise entitlements.

What is the biggest risk when retiring at 60 with $270K? Spending too much too early. The first two to three years of retirement often involve higher spending, and from a modest base, drawing heavily in those early years compounds into a funding shortfall a decade later. Sequencing of drawdowns matters significantly at this balance level.

Is $270K enough for a couple to retire at 60? It is tight for a couple. ASFA’s modest lifestyle standard for a couple is $50,866 a year, and bridging seven years to 67 on a combined $270K is very challenging. A couple in this position generally benefits from at least one partner continuing to work part-time, or from delaying retirement until a higher combined balance is reached.

What happens to my super when I retire at 60? You can convert it into a tax-free account-based pension, which provides regular income payments and keeps the remaining balance invested. Withdrawals from super after age 60 are tax-free for most Australians. See our superannuation page for more on access rules and conditions of release.

What to Do Next

If you are approaching 60 with around $270K in super and want to know whether retirement is genuinely within reach, the most useful thing you can do is get a clear picture of your specific numbers before you make any decisions. Spending levels, housing situation, investment structure and Age Pension timing all interact in ways that general projections cannot fully capture.

Not sure where you stand? or take the free Wealthlab retirement quiz for a general read on your retirement readiness. Or if you want to talk through your situation with someone who looks at these numbers every day, book a free chat with the Wealthlab team. No pressure, no jargon.