$285,000 in super at 60 is a position that gets more workable than most people expect, particularly once you map out how the Age Pension fills the gap from 67. It’s not the ASFA comfortable benchmark. It’s not without constraint. But for a homeowner with no mortgage, it’s a genuine retirement foundation when structured properly.

Here’s the straight answer on what $285K covers, how the numbers look at different spending levels, and what the smartest moves are in the years before and after you stop work.

Super Access at 60: Confirmed

Preservation age is 60 for anyone born after 1 July 1964. At 60, once you retire or cease an employment arrangement, your full $285,000 is accessible and completely tax-free. No income tax on lump sums, no income tax on account-based pension income. That tax-free status applies immediately from age 60 for anyone in a taxed super fund, which covers the overwhelming majority of Australians.

Source: ATO: Super withdrawal options (Current as at May 2026)

Please note: All figures, projections and scenarios in this article are for general illustration only. Individual outcomes depend on personal circumstances, spending levels, investment returns, fees and government policy. This is general information, not personal advice.

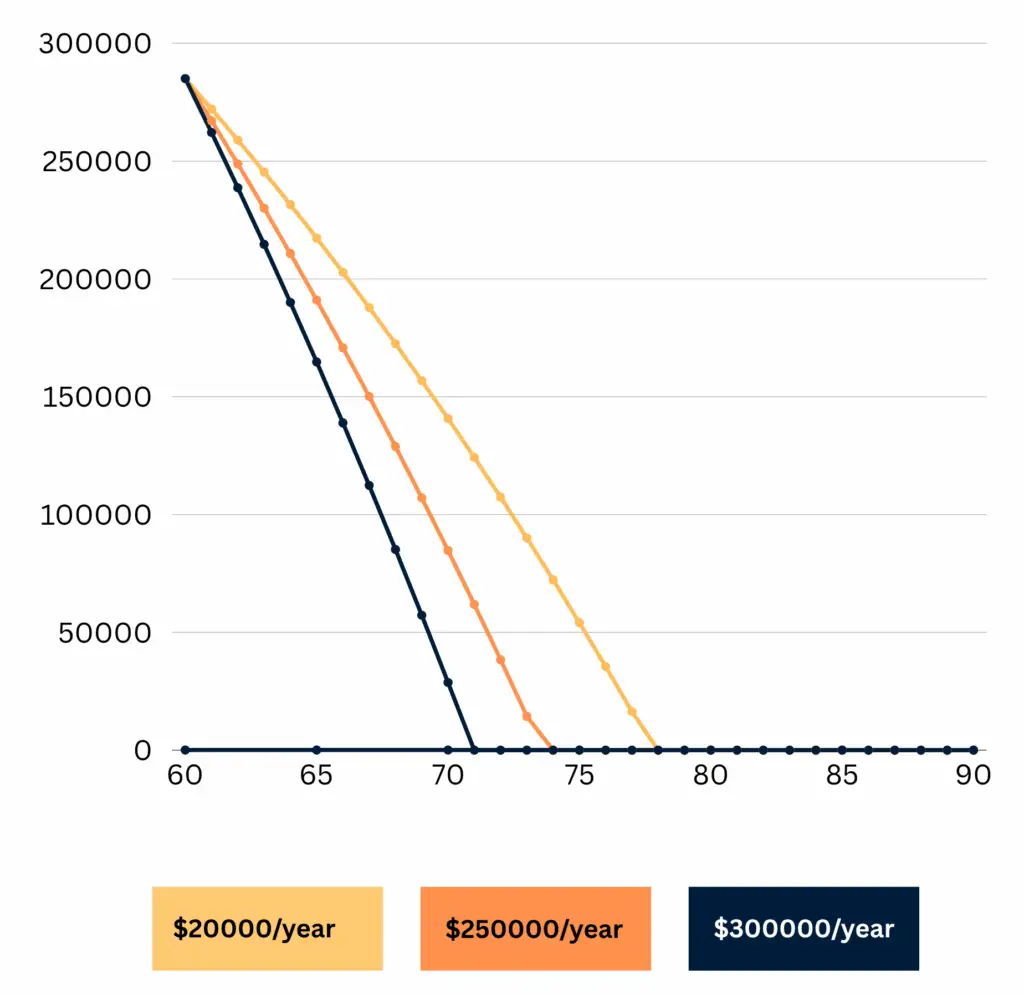

How Long Will $285,000 Last? The Numbers at Every Spending Level

Using a net annual return of 5% after fees and investment tax in a balanced account-based pension option, here is how $285K tracks from age 60:

| Annual spending | Balance at age 67 | Balance at age 75 | Notes |

|---|---|---|---|

| $18,000 per year | ~$227,000 | ~$163,000 | Full Age Pension likely from 67 |

| $22,000 per year | ~$185,000 | ~$98,000 | Full Age Pension likely from 67 |

| $28,000 per year | ~$129,000 | ~$27,000 | Full Age Pension likely from 67 |

| $33,000 per year | ~$76,000 | Depleted ~74 | Full Age Pension from 67 supplements |

| $38,000 per year | ~$25,000 | Depleted ~69 | Primarily Age Pension-funded from 67 |

What the “notes” column means: At every spending level up to $38,000 per year, a single homeowner arriving at 67 is likely to qualify for the full Age Pension of approximately $29,000 per year. The single homeowner full pension threshold for 2026 is $321,500 in total assessable assets. At every balance shown at age 67 in the table above, you’re below that threshold.

The practical picture from 67: full Age Pension of $29,000 per year plus whatever you choose to draw from remaining super. A retiree who spent $28,000 per year during the bridge years, arriving at 67 with $129,000, can now reduce their super drawdown to $10,000 to $12,000 per year and receive $29,000 from the Age Pension, total income of $39,000 to $41,000 per year. For a homeowner with no debt, that’s a comfortable and stable retirement.

Source: Services Australia: Age Pension (Current as at May 2026)

The Seven-Year Bridge: Why Age 60 to 67 Is the Whole Game

Retiring at 60 means seven full years of self-funded retirement before Age Pension eligibility at 67. During that window, your $285K is doing all the work. There’s no employer SG coming in, no government supplement, nothing.

At $28,000 per year that’s $196,000 in total drawdown over seven years. On a $285K starting balance, that leaves approximately $129,000 at 67. Still workable because the full Age Pension kicks in at that point.

At $38,000 per year, you draw $266,000 over seven years and arrive at 67 nearly empty. Completely reliant on the pension. That’s not a retirement failure, the Age Pension is designed for exactly this,but it leaves no buffer for unexpected costs, healthcare, or helping family.

The single most impactful decision at $285K is not which fund you’re in or what investment option you choose. It’s what you spend during the bridge years. Every $5,000 less per year in drawdown over seven years adds $35,000 to your balance at 67 and provides significantly more flexibility from that point.

What $285K Actually Supports at 60

Single homeowner, no mortgage:

Drawing $22,000 to $28,000 per year, this is a genuine if modest retirement. It covers:

- Weekly groceries and household costs

- Utilities, rates, insurance and basic maintenance

- A reliable car and running costs

- Basic private health insurance or reliance on Medicare and Commonwealth Seniors Health Card

- Occasional dining out and modest social spending

- Annual domestic travel, particularly by car or budget interstate

From 67, the Age Pension supplement lifts total income to $39,000 to $42,000 per year for someone who drew conservatively during the bridge. For a homeowner with no debt and the pensioner concession card reducing healthcare, pharmacy and utility costs, that income level supports a genuinely comfortable lifestyle.

Couple with combined super near $285K to $450K:

For a couple, the picture is more comfortable. Two sets of living costs are shared, two Age Pension entitlements become available from 67, and the couple’s full pension of approximately $43,700 per year combined provides a stronger floor. A couple with $285K combined super and a paid-off home can live well from 67 onward on the combined pension plus modest drawdown.

If you’re still renting:

Renting materially changes the calculation. Add $20,000 to $28,000 per year in rent to your spending and the $285K bridge becomes very thin very quickly. A renting retiree drawing $48,000 to $56,000 per year total (rent plus living costs) would exhaust $285K in under six years. If you’re renting at 60 with $285K, a frank conversation about whether full retirement now versus working another three to five years is the right call is essential.

Carrying a mortgage:

If you have a remaining mortgage, the same maths apply: mortgage repayments are competing with every other living cost for a share of $285K. Working to clear the mortgage before retiring or using a partial lump sum from super at 60 to clear the balance are both legitimate strategies, but each has implications for your drawdown runway and Age Pension eligibility that need to be modelled.

$285K Against the National Benchmarks

Average super balance for Australians aged 60 to 64 (APRA data):

- Men: approximately $396,000

- Women: approximately $313,000

At $285,000, you’re below the national average for both genders. You’re in the same position as a large proportion of Australians planning retirement, which is exactly why the Age Pension exists and why it’s structured as a genuine income supplement rather than a token payment.

ASFA Retirement Standard (February 2026):

- Comfortable single at 67: $630,000

- Modest single at 67: $110,000

- Comfortable couple at 67: $730,000 combined

$285K sits between modest and comfortable for a single person, and closer to the modest end. But the ASFA comfortable benchmark assumes retirement at 67 with limited Age Pension. Someone retiring at 60 with $285K and drawing into the Age Pension from 67 can achieve a combined income that puts them closer to the comfortable standard in practice from that point.

Source: ASFA Retirement Standard, February 2026

Four Strategies That Improve the $285K Picture Before You Retire

1. Catch-up concessional contributions before June 2026

If your total super balance is under $500,000 and you’ve had unused concessional cap space in the past five years, you can make catch-up contributions on top of the standard $30,000 annual cap. Unused amounts from the 2020/21 financial year (when the cap was $25,000) expire permanently on 30 June 2026. For a 60-year-old still working, checking your carry-forward balance in myGov now and making a catch-up contribution before the financial year ends could add $15,000 to $25,000 to your balance at no extra marginal tax cost compared to taking it as salary. Scott and Phil covered this in Episode 7 of the Wealthlab Podcast.

2. Salary sacrifice in your final working months

Every dollar into super via salary sacrifice is taxed at 15% rather than your marginal rate. If you’re planning to retire in mid-2026, maximising salary sacrifice contributions between now and your last day adds to the balance while reducing your final income tax liability. On a $90,000 salary at 37% marginal rate, each $10,000 of salary sacrifice saves approximately $2,200 in tax.

3. Keep super invested in a balanced or growth option through the bridge

A common mistake at $285K is switching to cash or conservative when retiring at 60 because it feels safer. A 60-year-old’s money potentially needs to last 30 years. At 2% in cash versus 5% in a balanced fund, the difference on $285K over seven years is roughly $47,000 in foregone growth. That is not a trivial number at this balance level. Scott covered the real cost of being too conservative in Episode 1 of the Wealthlab Podcast: “Why Playing It Safe in Retirement Can Cost You More.”

4. Transition to Retirement pension if still working

If you’re 60 and not quite ready to fully retire, a Transition to Retirement pension lets you draw up to 10% of your balance per year as income while still working. On $285K that’s up to $28,500 per year to supplement a reduced salary, allowing you to drop to three or four days a week while your employer continues paying SG on your work income. The balance keeps accumulating from employer contributions and investment returns while you draw down a modest supplement. See our retirement planning page for how TTR works in practice.

Before You Stop Work: Five Things to Sort

Convert to an account-based pension on day one. Accumulation phase taxes investment earnings at up to 15%. Pension phase: zero. Contact your fund before your last day and have the switch set up to activate immediately. Every month in accumulation after retiring is unnecessary tax.

Set a drawdown rate deliberately. Don’t guess. Work out what you actually need per year. The bridge from 60 to 67 is where the balance either holds or depletes. A deliberate drawdown rate beats an aspirational spending number.

Check insurance inside super. Default life and TPD cover in accumulation often doesn’t automatically transfer to pension phase. If you have financial dependants, confirm what cover you hold and what happens to it before switching.

Update beneficiary nominations. Binding nominations expire every three years at most funds. A lapsed nomination means your super may not go where you intend. Check and renew it before retiring.

Apply for the Commonwealth Seniors Health Card. From 60, eligible retired Australians can access cheaper PBS medications, bulk-billed GP visits at many practices, and state concessions on rates and utilities. The combined annual value is easily $2,000 to $3,500 per year. Apply through Services Australia before you retire.

Should You Retire at 60 or Work a Little Longer?

The financial case for working even one or two more years at $285K is more meaningful than it is at higher balance levels, because the percentage improvement to your starting position is larger.

Working one additional year at $80,000:

- Adds approximately $9,600 in employer SG (12%)

- Avoids $22,000 to $28,000 in super drawdown

- Allows $285K to grow rather than shrink for one more year (approximately $14,250 at 5%)

- Combined effect: approximately $45,000 to $52,000 improvement in retirement position

That’s a 16% to 18% improvement on $285K from one additional year. At higher balances the same year adds a smaller percentage improvement. At $285K, each additional year matters more proportionally.

That said, this is a personal decision, not just a financial one. Health, work conditions, energy and the years when you can most actively enjoy retirement all factor in. Phil put it simply in Episode 5 of the Wealthlab Podcast: “Financial planning is a funny thing. You’ve got one answer on a spreadsheet, but you’ve got the other answer that takes into account living, breathing people with emotions.” The numbers are a guide, not a verdict.

Frequently Asked Questions

Can I retire at 60 with $285K in super in Australia?

Yes, particularly as a homeowner with no debt. Drawing $22,000 to $28,000 per year in a balanced investment option, $285K can bridge you through the seven years to Age Pension eligibility at 67, arriving with a meaningful balance and qualifying for the full Age Pension of approximately $29,000 per year from that point. Combined income from 67 of $39,000 to $42,000 per year is workable for a homeowner with low fixed costs.

How long will $285,000 in super last?

At $22,000 per year spending with 5% net returns, approximately 18 to 20 years in isolation. With the Age Pension supplementing income from 67 and reducing the required super drawdown, the balance extends considerably further. At $28,000 per year, the balance lasts through the bridge to 67 with approximately $129,000 remaining, at which point the Age Pension takes over much of the load.

Will I get the full Age Pension at 67 with $285K?

Almost certainly, yes, if you’re a single homeowner. The full Age Pension threshold for a single homeowner is $321,500 in total assessable assets. At every spending level above $22,000 per year during the bridge years, you arrive at 67 with assets below that threshold. Full Age Pension of approximately $29,000 per year would apply from 67.

What is the Age Pension age in Australia?

67, for anyone born on or after 1 January 1957. Retiring at 60 means seven full years of self-funded retirement before the Age Pension begins.

What is a catch-up concessional contribution and can I use one?

If your total super balance is under $500,000 and you haven’t used your full concessional cap in past years, you can carry forward unused amounts from the previous five financial years and contribute them on top of the standard $30,000 cap in a single year. Unused amounts from 2020/21 expire permanently on 30 June 2026. Check your available carry-forward balance in myGov now.

What is the minimum annual drawdown from super at 60?

The minimum account-based pension drawdown for someone under 65 is 4% of the opening balance per year. On $285,000 that is $11,400 per year. You can draw more than the minimum at any time. Drawing close to the minimum in the early bridge years preserves more capital for when the Age Pension starts at 67.

Is $285K above the national average super balance at 60?

No. The average for men aged 60 to 64 is approximately $396,000 and for women approximately $313,000. At $285K you’re below the average for both. But the Australian retirement system is designed for a broad range of balances, and the Age Pension is a genuine and substantial income source from 67 for most people with this balance level.

See What Your Retirement Actually Looks Like

The numbers above are general illustrations. Your actual retirement income depends on what you spend, whether you own your home, your partner’s situation, and what the Age Pension pays at your specific asset level at 67.

The free Wealthlab super calculator runs your own numbers in a couple of minutes and shows how different spending levels and the Age Pension change the picture.

If you’d like a proper retirement income plan built around your specific situation, book a free chat with the Wealthlab team. No jargon, no pressure.