Reaching 60 with $620K in superannuation puts you in a strong position to retire comfortably, but like all retirement planning, it requires careful consideration. Understanding how to make your money work, supplementing your super with the Age Pension, and planning for unexpected costs can make the difference between stress-free retirement and financial uncertainty.

Retire at 60 with $620K: What Lifestyle Can You Afford?

With $620K in super, you can enjoy a comfortable, modest retirement. Depending on your expenses and whether you are single or part of a couple, here’s what your super can cover:

- Household bills & utilities: Keep your day-to-day expenses covered without worry.

- Healthcare & medical costs: Access essential care and plan for unexpected medical expenses.

- Transport & mobility: Maintain a car or rely on public transport for daily life.

- Hobbies & travel: Enjoy local trips, hobbies, and social activities.

- Debt-free living: If you own your home, your super stretches even further.

Tip: Combining your super with careful budgeting and small supplementary incomes can significantly enhance your lifestyle.

Retire at 60 with $620K: The Role of the Age Pension

Once you turn 67, you may be eligible for the Age Pension, which is a valuable supplement to your super. This reduces the pressure on your own savings, giving you more flexibility.

- Single retiree: Approximately $28,500 per year

- Couple: Approximately $43,000 per year

By integrating your super with the Age Pension, you can enjoy a more secure and financially flexible retirement.

Smart Strategies to Retire at 60 with $620K

Even with $620K, smart planning is key to make your retirement last comfortably. Here’s how to optimise your funds:

Invest Wisely

Select a balanced investment portfolio combining growth assets like shares and ETFs with defensive options like bonds and cash. This ensures steady income while preserving your capital.

Budget Carefully

Track your retirement spending to ensure your lifestyle matches your income. Avoid overspending in early years to protect your long-term financial stability.

Supplement Your Income

Consider part-time work, freelance gigs, or rental income to provide extra financial cushion. These options can help bridge any gaps and maintain your lifestyle without draining super.

Relocating

Reducing housing costs by downsizing or moving to a more affordable location frees up funds for hobbies, travel, and healthcare.

Phased Retirement

Gradually reducing work hours before full retirement at 60 allows you to boost your super while easing into the retirement lifestyle.

📉 How Long Will $620K Last?

Assuming an average real return of 2.44% after inflation, here’s how long $620K might last depending on your yearly spending:

| Annual Spending | Estimated Longevity |

|---|---|

| $20,000/year | ~30+ years |

| $25,000/year | ~28–30 years |

| $30,000/year | ~25–27 years |

| $35,000/year | ~20–23 years |

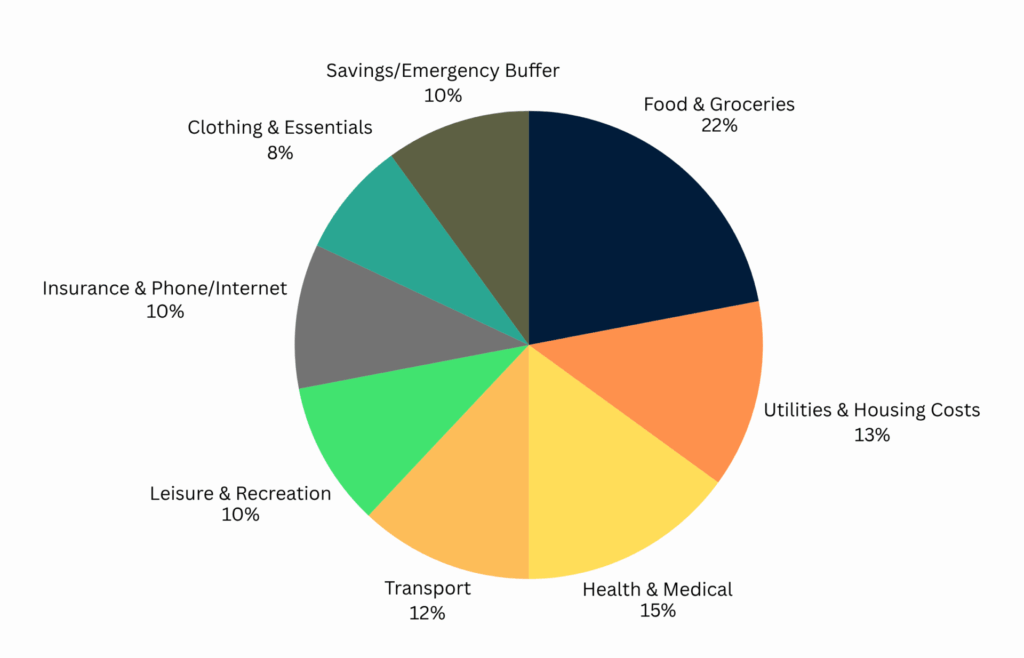

🧾 How Would You Budget $30K/Year?

If you plan a modest retirement lifestyle, here’s a breakdown of where your money might go:

| Category | % of Budget |

|---|---|

| Food & Groceries | 22% |

| Utilities & Housing Costs | 13% |

| Health & Medical | 15% |

| Transport | 12% |

| Leisure & Recreation | 10% |

| Insurance & Internet | 10% |

| Clothing & Essentials | 8% |

| Emergency/Savings Buffer | 10% |

This type of budget is realistic and can offer a fulfilling retirement if you’re careful and well-prepared.

What Happens at Age 67?

Once you reach 67, you’re likely eligible for the Age Pension, which significantly strengthens your retirement income:

| Pension Type | Annual Estimate |

|---|---|

| Single | ~$28,500 |

| Couple Combined | ~$43,700 |

By this stage, you can either reduce your reliance on your super or use it for top-ups, travel, or unexpected medical needs.

Common Pitfalls to Avoid

Even with $620K, here are things that could derail your retirement:

❌ Spending too much in the first 5 years

❌ Ignoring inflation and rising health costs

❌ Delaying investment optimisation

❌ Not understanding Age Pension eligibility

❌ Letting fear stop you from making a plan

FAQs: Retire at 60 with $620K

Q1: Is $620K enough to retire at 60 in Australia?

Yes, if you plan carefully, manage your spending, and supplement your super with the Age Pension and other income sources.

Q2: How long will $620K last in retirement?

With careful investment and budgeting, $620K can support a comfortable retirement for 25–30+ years, especially when combined with the Age Pension.

Q3: Should I invest differently at 60?

Yes, a more conservative investment strategy is recommended at retirement to preserve capital while still generating income.

Q4: Can I retire earlier than 60 with $620K?

You could retire earlier, but you’d need additional savings outside super to cover the years before you can access your super at 60.

Want to explore similar scenarios? Check out:

- Can I Retire at 60 with $670K in Australia? – Discover how slightly higher super changes your lifestyle options.

- Can I Retire at 60 with $720K in Australia? – Learn how to maximise a bigger super balance for a more luxurious retirement.

Plan Your Retirement with Confidence

Retiring at 60 with $620K is possible, but success depends on careful planning, smart investing, and budgeting. The earlier you start preparing, the more comfortable and stress-free your retirement will be.

📅 Book your free retirement strategy session today and let experts help you create a plan that ensures your super lasts and your retirement dreams come true.