The short answer is that $580K in super at 60 can support a comfortable retirement for many Australians, particularly those who own their home and have no debt. But the numbers only tell part of the story. How long it lasts depends on how you draw it down, how it’s invested, what you spend, and when the Age Pension kicks in at 67.

This post walks through what $580K looks like in practice, what lifestyle it might support, and the key things to consider before you hand in your notice.

What Does $580K Actually Get You in Retirement?

A common starting point is the ASFA Retirement Standard, which estimates a couple needs around $690,000 in super (plus the Age Pension) to fund a comfortable retirement, and a single person needs around $595,000. (Source: ASFA, superannuation.asn.au)

At $580K, a single person sits just below that ASFA comfortable standard. A couple with $580K combined is further from it. But “comfortable” in ASFA terms is just one benchmark. Many Australians retire with less and live well. The Age Pension, a paid-off home and sensible spending habits can close the gap considerably.

The rough rule of thumb for drawing from super is around 4 to 5% a year to preserve your balance over the long term. On $580K, that’s $23,000 to $29,000 a year from your own savings. That figure looks modest in isolation, but once you factor in a part or full Age Pension from age 67, the picture shifts noticeably.

The Age Pension Factor

The Age Pension becomes available at 67. Current maximum rates from 20 March 2026 are:

- Single: approximately $31,223 a year

- Couple (combined): approximately $47,070 a year

(Source: Services Australia, current as at March 2026. Rates are updated each March and September.)

Whether you receive the full pension, a part pension or nothing depends on the assets test and income test. A homeowning single retiree with $580K in super and no other significant assets would likely be eligible for at least a part Age Pension at 67, once super starts drawing down.

This is worth planning for. The Age Pension can meaningfully extend how long your savings last.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

What Lifestyle Could $580K Support?

A lot depends on whether you own your home outright. Retirees with no mortgage or rent to pay have significantly lower essential costs, and $580K tends to stretch much further as a result.

For a homeowning retiree drawing around $35,000 to $45,000 a year from super and part-Age Pension combined, a modest but comfortable lifestyle is generally achievable. That covers essentials like groceries, utilities, transport, health cover and some discretionary spending on travel or hobbies. It is not a lavish retirement, but for many Australians it is genuinely enough.

A more stretched scenario is a retiree paying rent or still carrying a mortgage at 60. In those cases $580K needs to work much harder, and getting specific advice on structuring your drawdown and pension entitlements becomes much more important.

Our retirement planning page has more on how Wealthlab helps people think through these scenarios.

The Big Risk: Retiring Seven Years Before the Age Pension

One thing that catches many people off guard is the gap between when you retire at 60 and when the Age Pension begins at 67. That is a seven-year window where you are running entirely on your own savings.

We covered this in depth on the podcast in Episode 19: Is Early Retirement a Trap? The $150K Gap Most Aussies Miss. The episode looks at how retiring even a year earlier than planned can shift your numbers significantly. Worth a watch if you’re crunching the timing.

During the 60 to 67 window, drawing $40,000 to $50,000 a year (before any returns) eats through roughly $280,000 to $350,000 of your balance. By the time the Age Pension starts, your super balance may be substantially reduced, which then affects how long the remaining amount lasts alongside pension income. Getting the sequencing right matters.

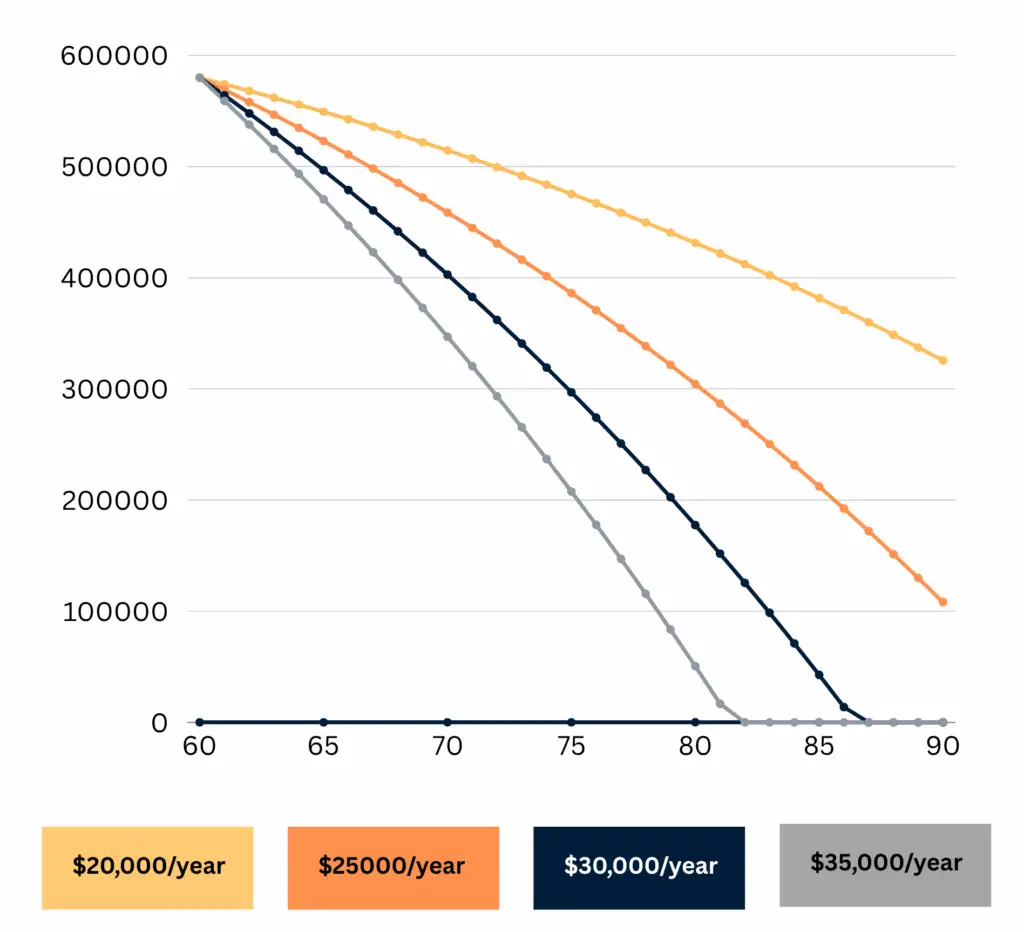

This Line Chart Shows how $580K super depletes from age 60 to 90 across different annual spending levels.

Your Investment Mix Matters More Than Most People Realise

A common mistake at 60 is shifting everything to a conservative or cash-heavy portfolio because it “feels safer.” The problem is that if your super is sitting in a low-growth fund for 25 to 30 years of retirement, it may not keep pace with inflation, let alone grow.

On the Wealthlab podcast, Episode 1: Why Playing It Safe in Retirement Can Cost You More, Scott and Phil walked through how a couple with $500K in super spending $75K a year can see their retirement fund last to their late 90s on a growth portfolio but run out 15 years earlier on a conservative one, despite the same average return. The only difference is the sequence of returns and the portfolio mix.

This does not mean everyone should be in high growth. Your investment strategy depends on your spending needs, your timeline, your risk tolerance and your overall financial picture. What it does mean is that superannuation strategy is worth thinking through carefully, not just defaulting to conservative because you are getting older.

A General Scenario: How the Numbers Might Flow

To make this more concrete, here is a rough illustrative example. A 60-year-old single homeowner with $580K in super, no debt, and modest spending of around $40,000 a year might see their finances broadly like this:

- Age 60 to 67: Drawing primarily from super. At $40K a year (before any investment returns), the balance reduces over this period, though investment growth offsets some of this drawdown.

- Age 67+: A part Age Pension supplements super drawings. Combined income from both sources may be around $45,000 to $55,000 a year, depending on the balance at that point and what the pension means test determines.

- Age 80+: Healthcare costs typically rise. This is worth budgeting for separately. Episode 19 on the podcast noted that 34% of retirement savings, on average, are consumed by healthcare costs.

None of this is a guarantee. Individual circumstances vary significantly. But this is broadly the shape of a retirement on $580K for many Australians.

Want to see how your own numbers might look? Run them through the free Wealthlab super calculator for a general snapshot.

Other Strategies Worth Knowing About

A few options that some retirees in this situation explore include:

Downsizer contributions. If you sell the family home and downsize, you may be eligible to contribute up to $300,000 per person into super under the Downsizer Contribution Scheme. We covered the detail and the traps in Episode 2: Downsizer Contributions: The Hidden Traps You Must Know. The 90-day deadline and the Age Pension assets test implications catch many people out.

Transition to retirement (TTR). At preservation age (60 for most people), some retirees use a transition to retirement strategy to reduce hours while drawing a limited income from super. Whether this suits your situation depends on a range of personal factors.

Part-time work. Even earning $10,000 to $15,000 a year for a few years post-60 can take meaningful pressure off super drawdowns and preserve more of your balance for later. Many retirees also find it helps the adjustment to retirement, which is its own process. Our Pension and Centrelink page covers how income affects your Age Pension entitlements.

FAQ: Retiring at 60 with $580K in Australia

Can I retire at 60 with $580K in super? For many Australians, yes. Whether it works comfortably depends on your spending, whether you own your home, your investment strategy and how you bridge the gap to the Age Pension at 67. Individual circumstances vary considerably.

How long will $580K in super last? At a 4 to 5% drawdown rate and assuming some investment growth, $580K could potentially last 20 to 30 years for many people. This estimate shifts significantly based on your actual returns, fees and spending. The Age Pension from 67 also extends how long your super needs to carry you.

Will I be eligible for the Age Pension with $580K in super? It depends on your total assets, whether you own your home and what income you have. A homeowning retiree whose super has drawn down over several years will often qualify for at least a part Age Pension at 67. Services Australia’s assets and income tests determine eligibility. Figures are current as at March 2026.

What is the risk of retiring at 60 rather than 65 or 67? The main risk is the seven-year gap before the Age Pension begins. You are drawing entirely from your own savings during this period, which significantly reduces the balance that has to last through the rest of your retirement.

Should I keep my super in a growth or conservative investment option? This depends on your individual situation, risk tolerance and retirement timeline. Many retirees benefit from maintaining some growth exposure through retirement rather than shifting entirely to conservative options. Speaking with a qualified financial adviser is the most reliable way to work through this for your circumstances.

What is the ASFA comfortable retirement standard? ASFA’s 2024/25 Retirement Standard estimates a single person needs around $595,000 in super (plus the Age Pension) for a comfortable retirement, and a couple needs around $690,000. These are general benchmarks, not personal targets. (Source: ASFA)

Talk It Through with Wealthlab

If you are approaching 60 with $580K in super and wondering whether the numbers stack up, the most useful thing you can do is sit down with someone who can look at your full picture, not just the super balance.

At Wealthlab, we work with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how these general principles might apply to your circumstances.

Not ready to book? Take the free Wealthlab retirement quiz for a general snapshot of where you stand.