If you’re sitting on $520K in super and wondering whether 60 is realistic, the honest answer is: it depends. For many Australians, particularly homeowners with no debt and modest spending habits, $520K can support a genuine retirement. But it requires more careful planning than higher balances, and the seven-year gap before the Age Pension kicks in at 67 is the part that trips most people up.

This post walks through what $520K actually means in practice, what lifestyle it might support, and the key decisions that tend to determine whether the money lasts.

How Far Does $520K Actually Go?

A useful reference point is the ASFA Retirement Standard, which estimates a single homeowner needs around $595,000 in super (plus the Age Pension) to fund a comfortable retirement, and a couple needs around $690,000. (Source: ASFA)

At $520K, a single retiree is below that comfortable standard. A couple with $520K combined is meaningfully below it. That does not mean retirement is out of reach at 60, but it does mean planning and structure matter more, not less.

The commonly used drawdown guideline is 4 to 5% of your balance per year, which on $520K works out to around $20,800 to $26,000 a year from your own savings. That figure is tight if you have significant expenses, but it improves considerably once the Age Pension supplements it from age 67.

The Age Pension From 67

The Age Pension does not start at 60. It begins at 67, which means the first seven years of a retirement at 60 rely almost entirely on your own savings. Once you reach 67, and assuming your balance and other assets sit within the means-test thresholds, you may be eligible for a part or full Age Pension.

Current maximum rates from 20 March 2026 are:

- Single: approximately $31,223 a year

- Couple (combined): approximately $47,070 a year

(Source: Services Australia, current as at March 2026. Rates are updated each March and September.)

With a $520K balance at 60 drawing down at around $35,000 to $40,000 a year, a meaningful portion of that balance will be drawn by 67. That can actually work in your favour for Age Pension eligibility, as a lower super balance means the assets test is less likely to cut you out. A qualified adviser can help model how this plays out for your specific numbers.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

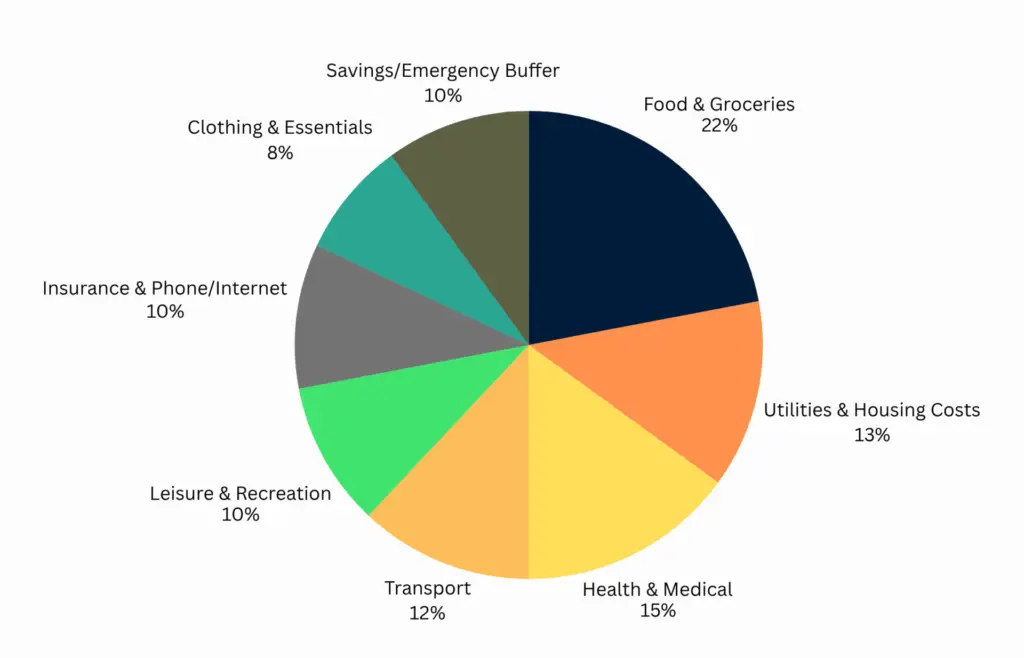

How Would a $30K Budget Look?

Here’s a typical breakdown for Australians living a modest but fulfilling retirement:

| Category | % of Budget |

|---|---|

| Food & Groceries | 22% |

| Utilities & Housing Costs | 13% |

| Health & Medical | 15% |

| Transport | 12% |

| Leisure & Recreation | 10% |

| Insurance & Communications | 10% |

| Clothing & Essentials | 8% |

| Emergency/Savings | 10% |

This budget assumes debt-free living and smart money management both essential for retirement success.

What Lifestyle Could $520K Support?

Owning your home outright makes a substantial difference at this balance. Without rent or mortgage payments, essential living costs drop significantly and the super stretches further.

For a debt-free homeowner spending around $35,000 a year from a combination of super and eventual Age Pension, a modest but comfortable retirement is achievable for many people. That covers groceries, utilities, transport, private health insurance, some leisure and occasional travel within Australia.

What $520K is unlikely to support comfortably is a retirement that includes expensive hobbies, frequent overseas travel, or significant ongoing debt repayments. If those are priorities, either the retirement date or the spending plan may need adjustment.

Our retirement planning page has more on how Wealthlab approaches these conversations.

The 60 to 67 Gap Is the Biggest Risk

Scott and Phil covered this directly in Episode 19: Is Early Retirement a Trap? The $150K Gap Most Aussies Miss. The episode found that retiring just one year earlier than planned can shift your projections significantly, and that the average couple retiring today has around $540K combined, around $150K below the ASFA comfortable standard.

With $520K at 60, that seven-year window before the Age Pension is the stretch where the numbers are under the most pressure. Drawing $35,000 to $40,000 a year with no other income source and minimal investment growth would consume $245,000 to $280,000 of your balance before you turn 67. Investment returns may offset some of this, but the sequencing matters. A run of poor market returns early in retirement can do real damage to a balance this size.

This is one reason why investment strategy at retirement is worth thinking through carefully, not just defaulting to whatever the super fund has you in by default.

Investment Strategy: Why Conservative Is Not Always Safer

A lot of people approaching 60 shift their super into conservative or cash-heavy options because it feels like the right thing to do when you’re close to retirement. The problem is that with a 25 to 30 year retirement ahead of you, a portfolio that barely keeps up with inflation can erode your purchasing power year by year.

Episode 1 of the Wealthlab podcast, Why Playing It Safe in Retirement Can Cost You More, worked through a real example of how a conservative portfolio and a growth portfolio with the same average return can produce dramatically different outcomes based on sequencing alone. For a balance of $520K, those differences compound over decades.

This is not a case for putting everything in high-growth shares. It is a case for making a deliberate, informed decision about your investment mix rather than defaulting to whatever sounds safest. Our superannuation page covers how we approach this with clients.

Strategies That Can Help the Numbers Work

A few options that people in this situation commonly explore:

Staying in part-time or consulting work for a few years. Even $10,000 to $15,000 a year from part-time work in the early years of retirement significantly reduces the pressure on super and lets the balance keep growing. Many retirees also find it helps them adjust to the rhythm of not working full-time, which is its own transition.

Downsizer contributions. If you sell the family home and downsize, you may be able to contribute up to $300,000 per person into super under the Downsizer Contribution Scheme. There are traps around the 90-day deadline and how the cash from the sale affects your Age Pension assets test. Scott and Phil covered these in detail in Episode 2: Downsizer Contributions: The Hidden Traps You Must Know.

Understanding the Age Pension means tests. The assets test and income test can be navigated strategically. With the right structure, some retirees who expect to receive nothing from the Age Pension find they are entitled to a part pension that meaningfully improves their income. Our Pension and Centrelink page covers how this works.

Want to see how your own numbers might look across different scenarios? Run them through the free Wealthlab super calculator for a general starting point.

A General Scenario: What the Numbers Might Look Like

To make this concrete, here is a rough illustrative example for a single, debt-free homeowner at 60 with $520K in super spending around $35,000 a year:

- Age 60 to 67: Drawing primarily from super. At $35,000 a year before investment returns, the balance reduces over this period.

- Age 67+: Part Age Pension becomes available depending on assets and income at that point. Combined income from super drawdown and pension may be around $40,000 to $50,000 a year.

- Healthcare costs: Worth budgeting separately. Episode 19 noted that healthcare tends to consume around 34% of retirement savings on average, and spending spikes significantly in the final years of life.

Individual circumstances vary widely. This is a general shape, not a projection for your situation.

FAQ: Retiring at 60 with $520K in Australia

Can I retire at 60 with $520K in super? For many Australians who own their home and have modest spending habits, $520K can support retirement at 60. The key variables are spending level, investment strategy and how well the balance holds up during the seven years before the Age Pension begins at 67. Individual circumstances vary significantly.

How long will $520K in super last? At a 4 to 5% drawdown rate with some investment growth, $520K could potentially last 20 to 25 years for many people. That timeframe shortens if returns are poor in the early years or if spending is higher than planned. Age Pension eligibility from 67 extends how far the remaining balance needs to stretch.

Will I qualify for the Age Pension with $520K? Eligibility depends on your total assets, income and whether you own your home. A homeowning retiree who has drawn down their super over the first seven years will often qualify for at least a part Age Pension at 67. Services Australia assesses eligibility based on the assets test and income test. Rates are current as at March 2026.

Is $520K enough without owning a home? If you are renting or still paying off a mortgage, $520K is likely to be stretched quite thin. Housing costs in retirement are a significant factor, and a balance this size works much harder when there is no rent or mortgage to cover.

What investment strategy is appropriate at 60? This depends on your individual risk tolerance, spending needs and retirement timeline. Many financial planners find that maintaining some growth exposure through retirement tends to support better outcomes over a 25 to 30 year period than shifting entirely to conservative options. Getting specific advice for your situation is worth doing before making any changes.

What if I want to retire before 60? Superannuation generally cannot be accessed before 60 unless you meet specific conditions of release. Retiring earlier means relying on other savings, investments or income to bridge the gap to when super becomes available. Our post on can I retire early in Australia with low super covers the options.

Talk It Through with Wealthlab

If you are approaching 60 with $520K and trying to work out whether the numbers stack up, getting some clarity on the specifics of your situation is worth more than any general article, including this one.

Wealthlab works with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how these general principles might apply to your circumstances.

Not ready to book? Take the free Wealthlab retirement quiz for a general snapshot of where you stand.

If you want to see how the numbers compare at a slightly higher balance, our post Can I Retire at 60 with $580K in Australia? walks through a similar analysis.