Retiring at 60 with $480K in super is possible for many Australians, but it is probably the balance where planning starts to matter most. At this level, there is not a lot of room for error. Spending too much in the early years, sitting in the wrong investment option, or underestimating the gap before the Age Pension begins at 67 can all turn a workable retirement into a stressful one.

This post explains what retirement at 60 with $480K realistically looks like, what it can and cannot support, and the key factors that tend to determine whether the money lasts.

What Does $480K Mean Against the Retirement Benchmarks?

The ASFA Retirement Standard estimates that a single homeowner needs around $595,000 in super (plus the Age Pension) for a comfortable retirement, and a couple needs around $690,000. (Source: ASFA)

At $480K, a single retiree is around $115,000 below the ASFA comfortable benchmark. A couple with $480K combined is well below it. That does not mean retirement is impossible at 60, but it does mean the ASFA “comfortable” lifestyle is out of reach without other income sources or careful structuring.

The ASFA “modest” retirement standard, which covers essentials but little else, requires around $100,000 in super for a single person with the full Age Pension supplementing. That benchmark is well within reach. The question for most people at $480K is where between modest and comfortable their retirement ends up sitting, and how much planning shapes that outcome.

The Lifestyle $480K Can Realistically Support

The single biggest factor in whether $480K works for retirement at 60 is housing. A debt-free homeowner has fundamentally different options to someone still paying rent or a mortgage.

For a homeowning retiree drawing from super at a sustainable rate, retirement at 60 with $480K can generally cover:

- Regular household bills, groceries and insurance

- Private health cover and routine medical and dental costs

- Running a car or relying on public transport

- Modest hobbies, local outings and occasional domestic travel

- A small buffer for unexpected expenses

What it is unlikely to support comfortably is significant overseas travel, expensive hobbies, or any major ongoing debt repayment. A few unplanned large expenses in the early years, like a new car, a health issue or home repairs, can also set the plan back meaningfully.

Our retirement planning page has more on how Wealthlab works through retirement income scenarios with clients.

The 60 to 67 Gap: Where Most Retirement Plans at This Balance Come Unstuck

The Age Pension does not start at 60. It begins at 67, which means the first seven years of retirement at 60 run entirely on your own savings. That is the stretch where a balance of $480K is under the most pressure.

Drawing $30,000 to $35,000 a year from age 60 with no other income, and assuming modest investment growth, would consume somewhere between $180,000 and $210,000 before the Age Pension becomes available at 67. What remains at that point determines how the rest of retirement unfolds.

Scott and Phil discussed this gap in detail on the Wealthlab podcast in Episode 19: Is Early Retirement a Trap? The $150K Gap Most Aussies Miss. The episode found that the average couple retiring today has around $540K combined, and that even a one-year difference in retirement timing shifts the numbers significantly. For a balance of $480K, that point is particularly relevant.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.80s, especially with Age Pension stepping in from 67.

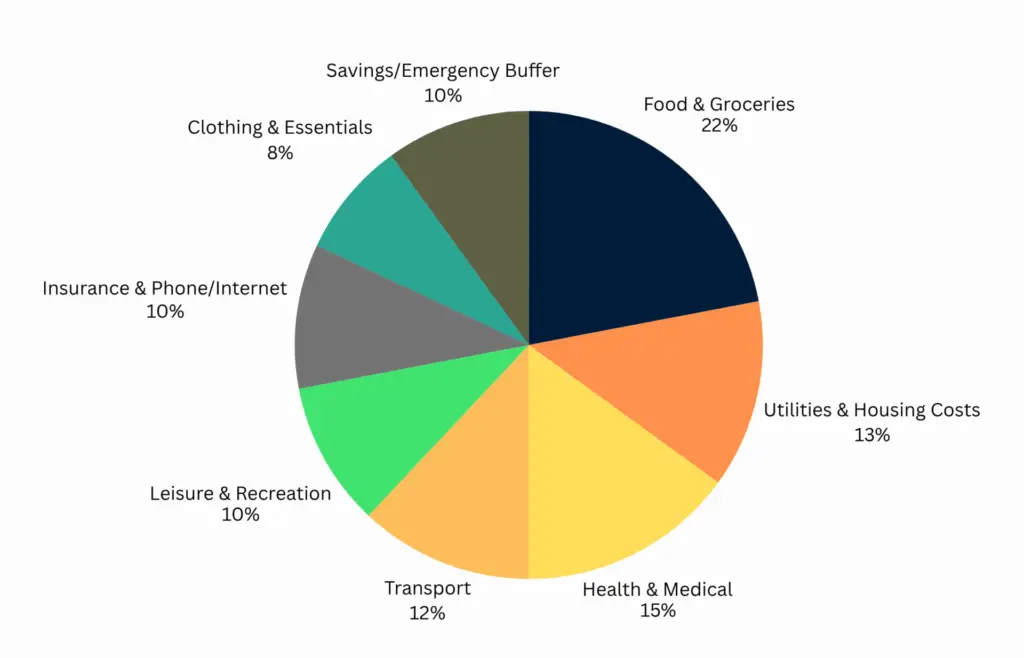

Sample Budget for $25K–$30K/year

Here’s how a modest retirement budget may be allocated:

| Category | % of Budget |

|---|---|

| Food & Groceries | 22% |

| Utilities & Housing Costs | 13% |

| Health & Medical | 15% |

| Transport | 12% |

| Leisure & Recreation | 10% |

| Insurance & Phone/Internet | 10% |

| Clothing & Essentials | 8% |

| Savings/Emergency Buffer | 10% |

This kind of lifestyle is common among Australians enjoying a simpler, debt-free retirement.

What the Age Pension Adds From 67

From age 67, the Age Pension can meaningfully improve retirement income for people whose super has drawn down to a level where they fall within the means-test thresholds.

Current maximum Age Pension rates from 20 March 2026 are:

- Single: approximately $31,223 a year

- Couple (combined): approximately $47,070 a year

(Source: Services Australia, current as at March 2026. Rates are updated each March and September by the Department of Social Services.)

For a retiree who started at $480K and has drawn down over seven years, the remaining balance at 67 may comfortably sit within homeowner asset-test thresholds, making a part or full Age Pension accessible. Combined with even a partial pension, retirement income of $40,000 to $50,000 a year becomes achievable for many people in this situation.

How the assets test and income test interact with your specific balance and circumstances is worth getting specific advice on. Our Pension and Centrelink page explains how these tests work in practice.

Investment Strategy in Retirement Matters More at Lower Balances

When your super balance is smaller, the impact of poor investment decisions is proportionally larger. A conservative or cash-heavy option might feel safe, but over a 25 to 30 year retirement it risks being eroded by inflation year by year.

At the same time, a high-growth strategy with $480K and no other income buffer carries real sequencing risk. If markets fall sharply in the first few years of retirement, a smaller balance has less time and room to recover.

The Wealthlab podcast covered this directly in Episode 1: Why Playing It Safe in Retirement Can Cost You More. Scott and Phil walked through how two retirees with the same average return but different portfolio mixes can end up with dramatically different outcomes over a 30-year retirement, purely because of the sequence of returns and how much they drew down during bad years.

For retirement planning at $480K, getting the investment mix right is genuinely consequential. Our superannuation page has more on how Wealthlab approaches this.

Strategies That Can Make $480K Work Better

A few approaches that some retirees in this situation explore:

Part-time or consulting work in early retirement. Even $10,000 to $15,000 a year in the first three to five years significantly reduces the pressure on super during the 60 to 67 window. It allows the balance to keep some growth momentum while drawing less. Many people also find that easing into retirement gradually suits them better personally.

Downsizing. If you own a home with significant equity, selling and downsizing can free up capital and, under the Downsizer Contribution Scheme, allow you to contribute up to $300,000 per person back into super. Scott and Phil covered the traps around this in Episode 2: Downsizer Contributions: The Hidden Traps You Must Know, including the 90-day deadline and how the proceeds affect your Age Pension assets test.

Catch-up concessional contributions before 60. If you are still working and under 60, and your super balance is below $500,000, you may be able to use unused concessional contribution caps from previous years to boost your super before retirement. Episode 10 of the podcast, How the Age Pension Really Works (With Real Case Studies), showed how catch-up contributions in the right year can save tens of thousands in tax while lifting the balance heading into retirement.

Want to see how these scenarios might play out for your numbers? Run them through the free Wealthlab super calculator for a starting point.

A General Retirement Income Scenario

To give a sense of how the numbers might flow, here is a rough illustrative example for a single homeowner at 60 with $480K in super and modest spending of around $32,000 a year:

- Age 60 to 67: Drawing primarily from super. Balance reduces over this period, partially offset by investment returns.

- Age 67+: Part or full Age Pension becomes available depending on assets at that point. Combined retirement income from super and pension may be around $40,000 to $48,000 a year.

- Longer term: Healthcare costs typically increase from the mid-70s onward. Factoring in a buffer for this, rather than assuming flat spending throughout retirement, leads to more realistic planning.

Individual outcomes vary significantly. This is an illustrative shape, not a projection for any specific person’s situation.

FAQ: Retiring at 60 with $480K in Australia

Can I retire at 60 with $480K in super? For many homeowning Australians with modest spending habits, retirement at 60 with $480K is possible. It requires a realistic spending plan, a considered investment strategy and an understanding of how the Age Pension fits in from 67. Individual circumstances vary considerably.

How long will $480K last in retirement? At a sustainable drawdown rate of around 4 to 5% a year with some investment growth, $480K could potentially support 20 to 25 years of retirement income for many people. Age Pension eligibility from 67 extends how far the remaining balance needs to stretch. Actual outcomes depend heavily on investment returns, fees and spending.

Will I qualify for the Age Pension with $480K in super? Eligibility depends on your total assets, whether you own your home and your income. A homeowner who has drawn down their super over the seven years from 60 to 67 will often find their remaining balance falls within the assets-test thresholds for at least a part Age Pension. Services Australia assesses eligibility under both the assets test and income test. Figures are current as at March 2026.

What investment strategy makes sense for retirement at this balance? This depends on your individual situation, risk tolerance and income needs. At $480K, the stakes of getting the investment mix wrong are proportionally higher than at a larger balance. Speaking with a qualified financial adviser before making any changes to your super investment option is worth doing.

Does owning my home make a big difference at $480K? Yes, significantly. A homeowner with no rent or mortgage has much lower essential costs than a renter, which means the same super balance goes considerably further. For retirees at this balance who do not own their home, the numbers are tight and other income or cost-reduction strategies become more important.

What if I retire at 60 but do some part-time work? Earning even a modest income in the early years of retirement can substantially extend how long your super lasts by reducing the drawdown during the critical 60 to 67 window. It can also improve your overall Age Pension position at 67 by preserving more of your balance.

Talk It Through with Wealthlab

If you are approaching 60 with around $480K and wondering whether the retirement numbers can work, the most useful step is getting a clear-eyed look at your specific situation, not just the average.

Wealthlab works with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how the general principles here might apply to your circumstances.

Not ready to book? Take the free Wealthlab retirement quiz for a general snapshot of where you stand.

If you want to compare how the numbers change at a slightly higher balance, our posts on Can I Retire at 60 with $520K? and Can I Retire at 60 with $580K? walk through similar ground.