Retire at 60 with $235K If you’re 60 and have $235,000 in super or savings, you might be wondering: “Is it enough to retire now?” The answer is yes, retiring at 60 with $235k is possible but it requires careful planning, a modest lifestyle, and smart use of both your super and future Age Pension entitlements.

In this blog, we’ll explore how far $235k can take you, how to manage the crucial 60–67 pre-pension years, and what kind of retirement lifestyle you can realistically expect.

Why Retiring at 60 Takes Extra Planning

By age 60, you’ve reached preservation age, so you can access your superannuation tax-free if you’ve officially retired. However:

- You’re still seven years away from the Age Pension, which begins at 67.

- You’ll need to fully self-fund your lifestyle until government support becomes available.

- The decisions you make now including how much you draw and how you invest will shape your financial future for decades.

So, can $235,000 last long enough? Let’s find out.

How Much Does Retirement Cost in Australia?

According to the ASFA Retirement Standard (March 2024):

- A modest lifestyle for a single person: ~$32,000/year

- A comfortable lifestyle: ~$51,000/year

These figures assume you own your home, live independently, and rely on public health systems.

With $235k, you’ll likely need to spend below the modest standard but it can still be enough to cover the 60–67 gap and set you up for a stable, simple retirement.

How Long Will $235k Last? A Retirement Projection

Let’s assume:

- Annual drawdown: ~$28,000

- Investment return: ~3% annually

| Age | Starting Balance | Withdrawal | Growth (3%) | Ending Balance |

|---|---|---|---|---|

| 60 | $235,000 | $28,000 | $6,200 | $213,200 |

| 61 | $213,200 | $28,500 | $5,500 | $190,200 |

| 62 | $190,200 | $29,000 | $4,900 | $166,100 |

| 63 | $166,100 | $29,500 | $4,300 | $140,900 |

| 64 | $140,900 | $30,000 | $3,700 | $114,600 |

| 65 | $114,600 | $30,500 | $2,900 | $87,000 |

| 66 | $87,000 | $31,000 | $2,100 | $58,100 |

| 67 | $58,100 | $10,000 | $1,700 | $49,800 |

With these assumptions, $235k can carry you through to Age Pension eligibility at 67, and still leave a modest buffer for later years.

What Happens at Age 67?

At age 67, you become eligible for the Age Pension, provided you meet the income and assets tests.

Full Pension Rates (July 2024):

- Single: ~$29,000/year

- Couple combined: ~$43,800/year

By this point, your super balance may be low enough to qualify for the full pension or close to it.At age 67, you become eligible for the Age Pension, provided you meet the income and assets tests.Once you begin receiving the pension, you’ll likely only need to draw down small amounts from any remaining super helping it last even longer.

How to Make Retirement Work on $235,000

1. Pay Off Your Home First

Owning your home before retiring removes one of the largest ongoing expenses from your budget. Without rent or mortgage repayments, your superannuation stretches much further. It also gives you long-term stability, especially if property values rise. If possible, prioritise clearing this debt before exiting the workforce.

2. Use a Super Income Stream

Converting your super into an account-based pension gives you a steady, tax-free income from age 60. It’s more efficient than taking lump sums and helps you manage cash flow across the 60–67 gap. You can adjust payments as needed while retaining investment flexibility. This strategy also helps reduce assessable assets for the Age Pension.

3. Budget Below the ASFA Modest Standard

The ASFA modest standard sits around $32,000/year, but spending $25k–$28k can make your super last longer. That means prioritising needs over wants and avoiding lifestyle creep. Leverage community discounts, healthcare cards, and concession schemes to cut costs. Small changes now can prevent financial stress later.

4. Keep Some Growth in Your Portfolio

Keeping all your funds in cash may feel safe but risks falling behind inflation. A balanced mix of growth and defensive assets provides capital protection and potential income. Maintain 1–2 years’ expenses in liquid assets for stability. Regular reviews help you adjust risk as your needs evolve.

5. Supplement Income with Flexible Work (If Needed)

Even 1–2 days of part-time work each week can preserve thousands in super. Consider freelance, consulting, or casual roles that suit your skills and energy levels. It not only boosts your finances, but keeps you socially active and mentally engaged. Ending work gradually can make retirement more sustainable and enjoyable.

Expected Lifestyle on $235,000

| Category | Expectation |

|---|

| Housing | Must own home |

| Food & Essentials | Covered with budgeting |

| Travel | Local or regional trips; no major holidays |

| Health | Public system; some out-of-pocket costs |

| Extras | Modest discretionary spending |

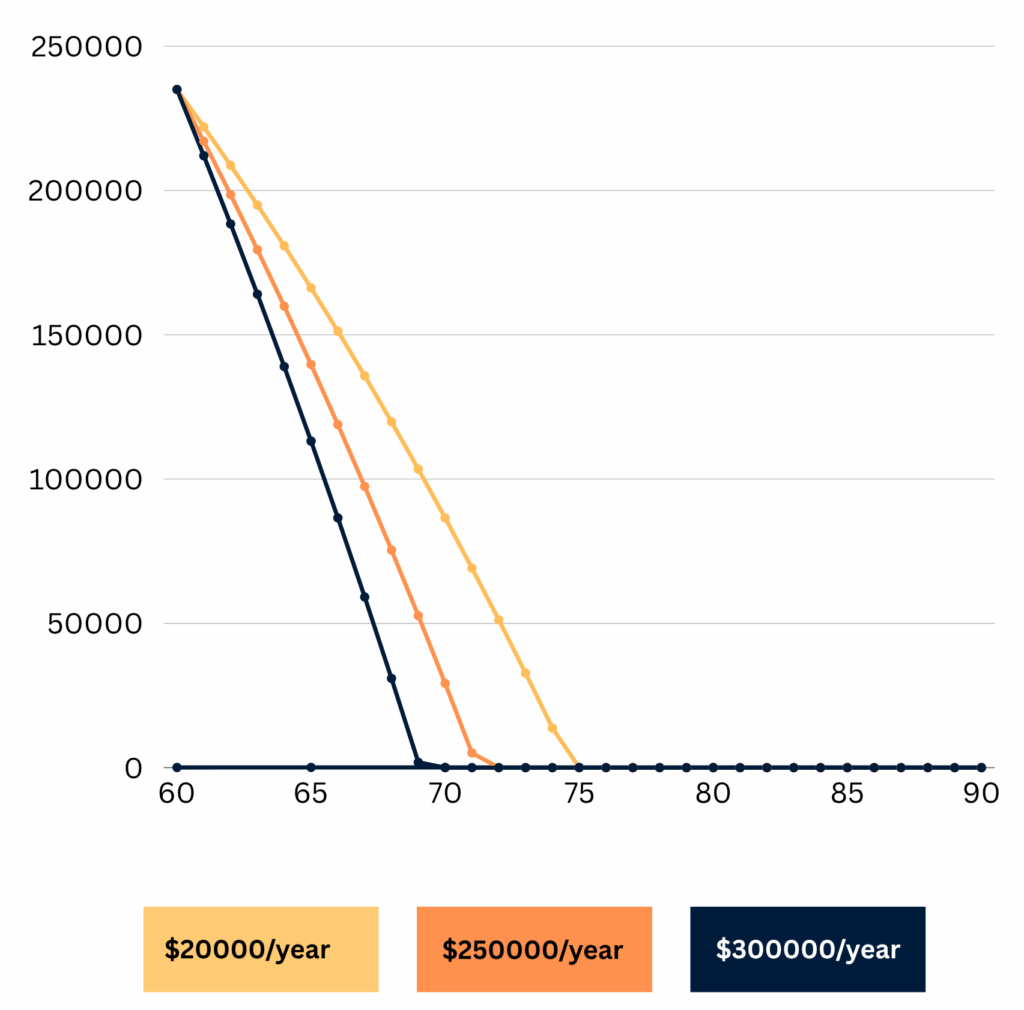

This Line Chart showing how $235K depletes from age 60 to 90 at 3 spending levels ($20K, $25K, $30K).

Mistakes to Avoid with $235k in Super

- ❌ Withdrawing large lump sums without a plan

- ❌ Assuming Age Pension starts before 67

- ❌ Overestimating returns or underestimating inflation

- ❌ Neglecting long-term healthcare planning

- ❌ Not getting professional advice tailored to your assets

Retiring at 60 with $235k? Let Wealthlab Help You Plan Confidently

At Wealthlab, we help Australians make the most of what they’ve saved no matter the number. We’ll model your income, test your strategy, and show you how to retire early without financial stress.

✔️ Super drawdown and income stream planning

✔️ Age Pension eligibility optimisation

✔️ Long-term retirement budgeting and investment advice

📞 Book your retirement planning session today

🔗 Talk to a Wealthlab Adviser