If you’re 60 with around $155,000 in super and wondering whether you can retire, you deserve a straight answer rather than vague reassurance. So here it is: $155K at 60 is a genuinely thin position for full retirement, and understanding why matters more than feeling good about the number.

The national average super balance for Australians aged 60 to 64 is approximately $396,000 for men and $313,000 for women. At $155K you’re well below both. That doesn’t mean retirement is impossible at 60, but it does mean that planning, the Age Pension, and realistic expectations about lifestyle all need to work harder than they do for someone with $400K or $500K.

Here’s the full picture: what $155K actually funds, what the Age Pension does for you, and what your real options are.

Can You Access Super at 60?

Yes. Preservation age is 60 for anyone born after 1 July 1964. Once you retire or cease an employment arrangement, your full balance is accessible tax-free. Withdrawals from a taxed super fund after age 60 attract zero income tax.

So the access question is settled. The harder question is whether $155K is enough to fund the retirement you want, and for how long.

Source: ATO: Super withdrawal options (Current as at May 2026)

Please note: All figures, projections and scenarios in this article are for general illustration only. Individual outcomes depend on personal circumstances, spending levels, investment returns, fees and government policy. This is general information, not personal advice.

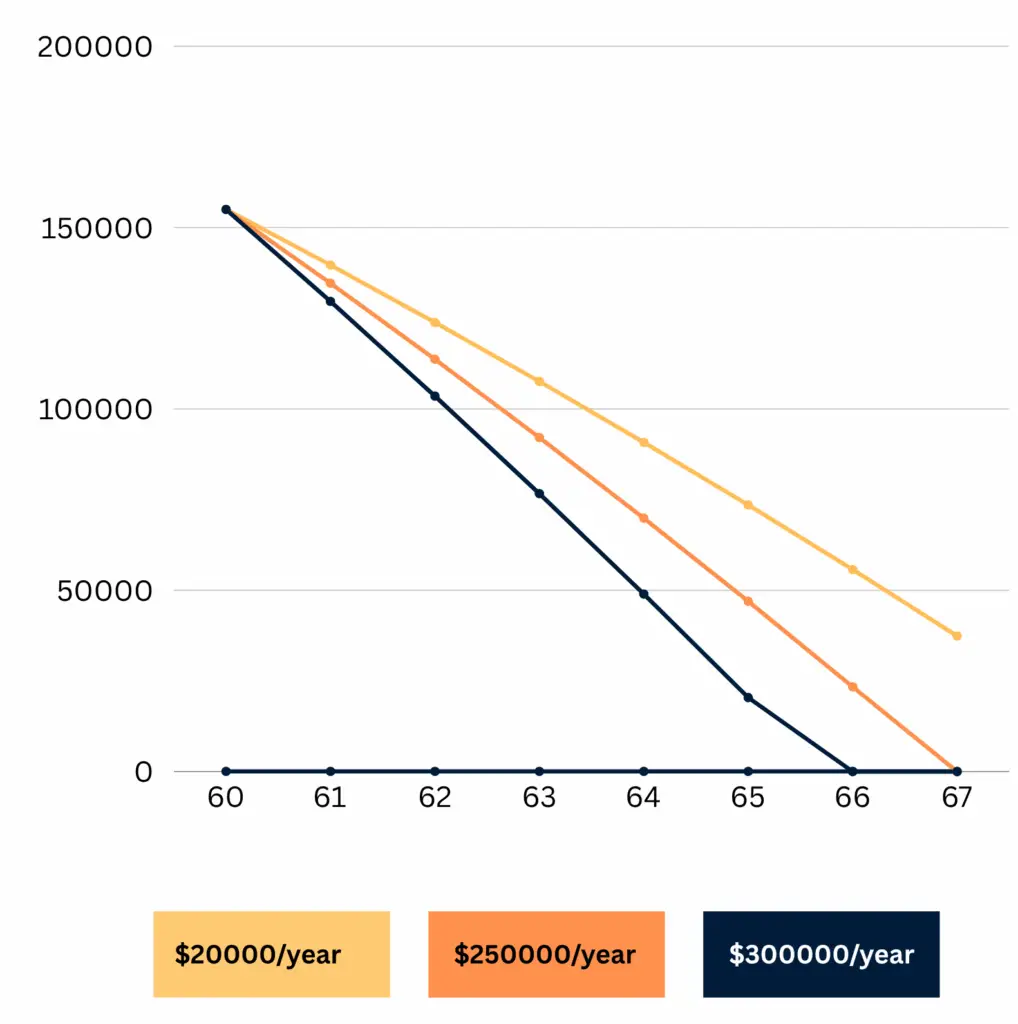

How Long Will $155,000 Last in Retirement?

Using a net return of approximately 5% per year after fees and tax in a balanced account-based pension, here is how $155K tracks at different spending levels.

| Annual spending | Balance at age 67 | Balance at age 75 |

|---|---|---|

| $15,000 per year | ~$87,000 | ~$23,000 |

| $20,000 per year | ~$44,000 | Depleted by ~73 |

| $25,000 per year | ~$5,000 | Depleted by ~68 |

| $30,000 per year | Depleted by ~65 | Gone |

The table is sobering. At $25,000 per year spending, a $155K balance is nearly gone by the time the Age Pension starts at 67. At $30,000, it runs out before 67 entirely.

This is not meant to alarm. It’s meant to show clearly that at $155K, the Age Pension is not a supplement to your super. It is your retirement income. The super bridge gets you to 67, and from there the Age Pension carries the load. That’s a legitimate and real retirement structure, but it requires understanding and planning, not assumptions.

This line chart comparing $155K under different spending levels shows how quickly your super may run out before pension kicks in.

The Age Pension Is the Real Foundation Here

Let’s be honest about what retirement at 60 with $155K actually looks like: you’re planning a retirement that’s primarily funded by the Age Pension from 67, with super as a bridge to get there.

That’s not a bad plan. It’s how the Australian retirement system was designed to work for a large portion of the population. But it means seven years (60 to 67) of self-funding on a thin balance before any government support kicks in.

Current full Age Pension rates (from March 2026, including all supplements):

| Per fortnight | Per year | |

|---|---|---|

| Single | ~$1,116 | ~$29,000 |

| Couple combined | ~$1,682 | ~$43,700 |

Source: Services Australia: Age Pension (Current as at May 2026)

For a single homeowner with $155K arriving at 67, your total assets are well below the full Age Pension threshold of $321,500. You would likely qualify for the full Age Pension of approximately $29,000 per year from the moment you become eligible.

$29,000 per year as a single homeowner with no debt is tight but workable. It covers basic groceries, utilities, a modest car, basic health cover through the pensioner concession card, and limited discretionary spending. It’s the ASFA modest retirement standard, roughly. It’s not ASFA comfortable, but it’s a real and stable income that doesn’t run out.

For a homeowner couple both accessing the Age Pension from 67, $43,700 per year combined is more comfortable. Two people sharing fixed costs (rent, utilities, rates) on $43,700 per year with no mortgage can live reasonably well.

The Seven-Year Bridge: Your Biggest Challenge

The real planning problem at 60 with $155K is not retirement itself. It’s the seven years between 60 and 67 when you have no government support.At $20,000 per year spending, you draw $140,000 over those seven years. On a $155K starting balance, you arrive at 67 with around $44,000 remaining, having used most of your super to bridge the gap. The Age Pension then takes over as your primary income.

At $25,000 per year, you’re almost out of super by 67. That’s a very tight bridge.

What makes the bridge work better:

Keep working, even part-time. This is the single most impactful thing you can do at this balance level. Working even two days a week at $25,000 to $35,000 per year between 60 and 67 dramatically changes the picture. Employer SG contributions continue building your balance. Your super drawdown drops to near zero or nothing. You arrive at 67 with most of your $155K still intact plus whatever has accumulated, and the Age Pension then supplements rather than replaces.

Draw only the minimum. The minimum account-based pension drawdown for under-65s is 4% per year. On $155K that’s $6,200 annually. For most people that’s not enough to live on, but keeping drawdowns as low as possible while supplementing with part-time income preserves the balance for longer.

Consider what “retiring” actually means for you. Full retirement at 60 on $155K is difficult. Semi-retirement, where you reduce to part-time work while starting to draw down super, is much more sustainable and is completely legal. You can cease a full-time employment arrangement, access your super as an income stream, and take on casual or part-time work simultaneously from age 60.

What Lifestyle Does $155K Support at 60?

For a single homeowner with no mortgage:

$155K can bridge you to 67, but it requires spending below $20,000 per year during that period, which is genuinely lean. If you have a partner with their own super or income, a paid-off home, and low fixed expenses, this becomes more manageable. If you’re relying solely on $155K for all living costs for seven years, you’ll need to be very disciplined, or supplement with some income.

From 67, the full Age Pension of $29,000 per year provides a stable base. For a homeowner with no debt and the pensioner concession card reducing healthcare and utility costs, $29,000 per year is liveable at the modest standard.

For a couple with combined super near $155K to $310K:

Two people with modest combined super arriving at 67 with limited assets both qualify for a meaningful Age Pension. The couple full pension threshold is $481,500 in combined assets. If your combined super is $155K to $300K combined by 67, you’d likely qualify for the full couple pension of $43,700 per year. Shared living costs make this more workable than the same income for a single person.

For someone still renting:

Retiring at 60 with $155K while renting is extremely difficult. The Age Pension at $29,000 per year does not cover rent in most Australian capital cities plus reasonable living expenses. If you’re renting and have this balance level, continuing to work until closer to 67 and building the balance further is likely the most important financial decision you can make.

Options Worth Seriously Considering

At $155K at 60, the conventional “retire and draw down super” path is harder than it would be at higher balance levels. But there are several genuine alternatives worth thinking through.

Work part-time from 60 to 65 or 67. This is the most financially powerful option at this balance level. Even $20,000 to $30,000 per year from casual or part-time work combined with minimum super drawdown preserves your balance almost entirely. You arrive at 67 with a significantly larger balance and full Age Pension eligibility. The lifestyle impact of two to three days per week is much lower than full-time work, and many 60-year-olds find this genuinely preferable to stopping entirely and watching a thin balance drain away.

Transition to Retirement (TTR) pension. If you’re still working but want to reduce hours, you can start a TTR pension at 60 without fully retiring. You can draw up to 10% of your balance per year from the TTR pension as income, which can allow you to drop to three or four days a week while maintaining similar take-home pay. Your employer continues paying SG on your remaining work income, which keeps building the balance. See our full breakdown of transition to retirement strategies.

Downsize if you own a larger property. If you own your home and it has significant value, the downsizer contribution rules allow you to put up to $300,000 per person into super from the proceeds of a home sale. This could dramatically change your retirement position. Selling a larger home and moving to a smaller, lower-maintenance property doesn’t just free up equity: it can inject a significant lump sum into super and reduce your ongoing living costs simultaneously.

Debt recycling or investment outside super. If you have assets outside super or capacity to invest, building wealth outside the super system is also an option from 60. It’s taxed differently, but it’s accessible, and it diversifies the income base you’re relying on.

What the Age Pension Assets Test Means for You

Because $155K is well below every Age Pension assets test threshold, your focus shouldn’t be on avoiding the Age Pension or trying to qualify for it. You will almost certainly qualify for a full Age Pension at 67 with this balance level. The focus should be on making the seven years to 67 work without exhausting the balance prematurely.

Current homeowner assets test thresholds (from March 2026):

| Full pension threshold | Part pension cut-off | |

|---|---|---|

| Single | Assets below $321,500 | Assets up to ~$695,500 |

| Couple combined | Assets below $481,500 | Assets up to ~$1,045,500 |

At $155K in super with no other significant assets, you’re well under the full pension threshold. From 67, you get the full pension. That’s the floor that makes this retirement work, even if the years before 67 are lean.

Phil and Dan covered how the Age Pension assets and income tests work in practice with real case studies in Episode 10 of the Wealthlab Podcast: “How the Age Pension Really Works.”

The Psychology of This Situation

Here’s the thing a lot of financial content won’t tell you directly: retiring at 60 with $155K is genuinely stressful territory, and the anxiety that comes with it is completely understandable.

Going from a regular income to funding your own retirement on a balance that could run out in seven years is not a small thing emotionally. As Scott said in Episode 8 of the Wealthlab Podcast: “The Psychology of Money,” “The goal isn’t to die with the largest super balance possible. The goal is to convert capital into confident living.” That’s true at $155K too. But confident living at this balance requires being honest about the constraints rather than hoping the numbers will somehow stretch further than they do.

The people who navigate this position well are the ones who get clear on what they actually need to spend each year, understand exactly what the Age Pension will provide, and make a deliberate decision about whether to work a little longer rather than hoping for the best. That clarity is more valuable than any investment return.

Frequently Asked Questions

Can I retire at 60 with $155K in super in Australia?

Technically yes, you can access super at 60. But $155K provides a thin bridge to Age Pension eligibility at 67. At $20,000 per year spending, the balance is largely depleted by 67. For most people in this position, semi-retirement with part-time work, or working until 63 to 65 while building the balance, is a stronger foundation than full retirement at 60.

How long will $155,000 in super last?

At $20,000 per year spending with a 5% net return, approximately 10 to 11 years before depletion, meaning roughly to age 71 to 72 if you retire at 60. However, from age 67 the Age Pension supplements income, which means you can reduce drawdowns and extend the balance considerably beyond that estimate. At $15,000 per year, the balance lasts longer and is partially intact when the Age Pension starts.

What is the full Age Pension for a single person in Australia 2026?

Approximately $29,000 per year for a single person including all supplements, as of March 2026. For couples, approximately $43,700 per year combined. The Age Pension is available from age 67 for anyone born on or after 1 January 1957.

Will I get the full Age Pension if I retire at 60 with $155K?

Not at 60 as Age Pension eligibility starts at 67. From 67, a single homeowner with $155K or less in remaining assets would likely qualify for the full Age Pension as total assets would be well below the $321,500 full pension threshold.

What is the minimum I can draw from super at 60?

The minimum account-based pension drawdown for someone under 65 is 4% of your opening balance per year. On $155,000 that’s $6,200 per year. You can draw more than the minimum at any time, but keeping drawdowns low while supplementing with part-time income preserves the balance for longer.

Should I use my super to retire at 60 or keep working?

At $155K, continuing to work, even part-time, makes a significant financial difference. Each additional year of employer SG contributions and reduced drawdown meaningfully improves your position at 67. Working part-time from 60 to 65 or 67 while drawing a modest TTR pension income is a common and effective strategy for people in this balance range.

What is a Transition to Retirement pension?

A TTR pension allows Australians who have reached preservation age (60) to access up to 10% of their super balance per year as income while still working. It’s designed for people who want to reduce hours before fully retiring, allowing them to supplement a reduced salary with super income while employer contributions continue building the balance.

Where to from Here

If you’re 60 with $155K in super, the most useful thing you can do right now is get clear on three numbers: what you’ll spend each year, what your Age Pension will be at 67, and whether the bridge between them is manageable on your current balance or whether working a little longer changes the picture enough to matter.

The free Wealthlab super calculator can help you model the bridge years and see how different spending levels and part-time income scenarios affect your position at 67.

If you’d like to talk through what your specific retirement actually looks like, book a free chat with the Wealthlab team. No judgment, no jargon, just honest numbers and a plan,or take the free Wealthlab retirement quiz