Retire at 60 with $270K ?You’ve saved up $270,000 in super and are approaching your 60th birthday. Naturally, the question arises: Is that enough to retire? While $270k won’t afford you a luxurious retirement, the good news is with smart planning, modest lifestyle choices, and a clear understanding of government support, retiring at 60 in Australia with $270,000 is absolutely achievable. The key lies in knowing how to stretch your money, what kind of lifestyle it can support, and how to navigate the crucial seven-year gap before you become eligible for the Age Pension at 67.

What Happens Financially When You Turn 60?

Turning 60 is a major financial milestone in Australia. It’s the age at which you reach your superannuation preservation age, meaning you can start accessing your super tax-free, as long as you declare retirement. This gives you greater flexibility in how you fund your retirement, but there’s a catch — you won’t be eligible for the Age Pension until you’re 67. That means for the first seven years of retirement, you’ll need to fully fund your lifestyle from your own savings.

This isn’t necessarily a deal-breaker. If you own your home, have no major debts, and are comfortable living on a modest income, then you can make it work. The important thing is to plan your withdrawals carefully ideally through an account-based pension and stick to a sustainable budget that doesn’t burn through your super too quickly.

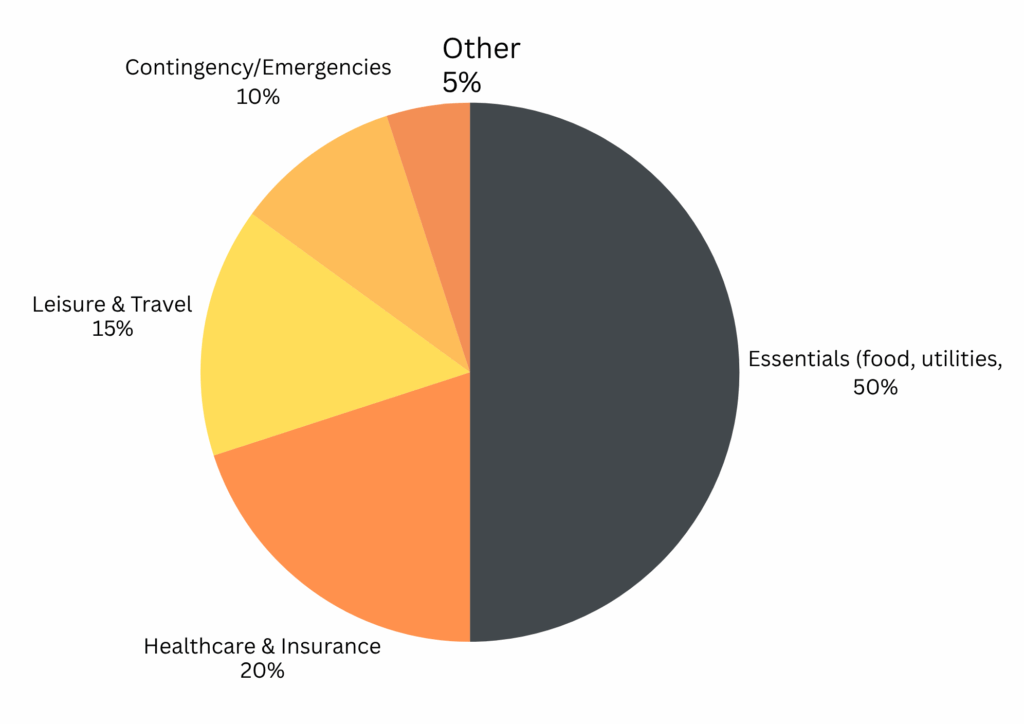

Sample $25K Budget Breakdown (if you own your home)

Here’s how a modest $25,000/year lifestyle might look:

| Category | % of Budget |

|---|---|

| Essentials (food, utilities, transport) | 50% |

| Healthcare & Insurance | 20% |

| Leisure & Travel | 15% |

| Contingency/Emergencies | 10% |

| Savings Buffer | 5% |

🏡 This assumes you own your home and maintain a modest lifestyle.

What Retirement Costs Look Like in Australia

To understand how far your $270k can go, you need a clear picture of what retirement costs actually look like. According to the ASFA Retirement Standard (March 2024), a modest lifestyle for a single retiree costs about $32,000 per year, while a comfortable lifestyle which includes things like private health cover, travel, and entertainment requires closer to $51,000 per year.

These estimates assume you:

- Own your home outright

- Use the public healthcare system (Medicare)

- Live independently without ongoing support

If you’re aiming to retire with $270,000 in super at 60, the goal should be to live slightly below the modest benchmark ideally spending between $27,000 to $30,000 per year. This approach gives you a bit of breathing room to weather inflation and unexpected expenses while still maintaining a decent quality of life.

How Long Will $270k Last in Retirement?

Let’s break it down using conservative assumptions:

- 📉 Annual drawdown: $28,000–$31,000

- 📈 Annual growth: 3%

| Age | Starting Balance | Withdrawal | Growth (3%) | Ending Balance |

|---|---|---|---|---|

| 60 | $270,000 | $28,000 | $6,400 | $248,400 |

| 61 | $248,400 | $28,500 | $5,900 | $225,800 |

| 62 | $225,800 | $29,000 | $5,200 | $202,000 |

| 63 | $202,000 | $29,500 | $4,300 | $176,800 |

| 64 | $176,800 | $30,000 | $3,600 | $150,400 |

| 65 | $150,400 | $30,500 | $2,800 | $122,700 |

| 66 | $122,700 | $31,000 | $2,200 | $93,900 |

| 67 | $93,900 | $10,000 | $2,800 | $86,700 |

This projection shows you can bridge the 60–67 period and still have savings left when the Age Pension starts.

What Happens at Age 67?

Current Full Pension Rates (July 2024):

- 👤 Single: ~$29,000/year

- 👥 Couple (combined): ~$43,800/year

Since you’ve already drawn down your super to a modest balance, there’s a good chance you’ll qualify for full or part pension giving your savings more longevity into your 70s, 80s, and beyond.

How to Make Retirement Work on $270,000

1. Own Your Home Before Retiring

Eliminating rent or mortgage payments lowers your annual expenses dramatically. Housing is typically the biggest cost in retirement and owning your home makes a $270k budget much more sustainable.

2. Set Up a Super Income Stream

Use your super to create an account-based pension. It allows regular income withdrawals, is tax-free from age 60, and helps control spending preserving your super for longer.

3. Spend Below the Modest Lifestyle Benchmark

Aim to live on $26,000–$30,000 per year. Use public healthcare, government concessions, energy discounts, and simple lifestyle adjustments to reduce costs without sacrificing quality of life.

4. Invest Conservatively But Strategically

Keep some of your super in income-generating assets like balanced or conservative growth funds. At the same time, hold 1–2 years of expenses in cash or liquid funds for stability.

5. Work Part-Time Until Age 63 (If You Can)

Even light or casual work for a few hours a week can delay your need to withdraw from super, build Age Pension eligibility, and offer emotional and social benefits in early retirement.

Mistakes to Avoid on a $270k Retirement Budget

❌ Assuming you’ll qualify for Age Pension early

❌ Spending too much in the first 2–3 years

❌ Taking out large lump sums from super

❌ Ignoring rising inflation and healthcare costs

❌ Not seeking professional retirement planning advice

Ready to Retire at 60? Let Wealthlab Help You Maximise Your $270k

You don’t need to delay retirement just because you’re not a millionaire. At Wealthlab, we specialise in helping everyday Australians turn modest super balances into secure retirements.

- Super income modelling

- Retirement drawdown strategies

- Pension eligibility planning

📞 Book your personalised retirement session today and retire smarter, not later.