If you are 60 years old with $500,000 in super and wondering whether it is enough to retire, you are in the same position as a significant number of Australians. $500K is close to the average combined super balance for couples retiring today, and for many homeowners it can genuinely support retirement when paired with the Age Pension from 67.

The short answer is that $500K can work for many people, but it requires understanding what the money can carry, where the gaps are, and how the Age Pension changes the picture once you reach 67. This post answers the questions we see most often from Australians at this balance.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

How Long Will $500,000 Last in Retirement in Australia?

This is the most searched question on this page, so it deserves a direct answer upfront.

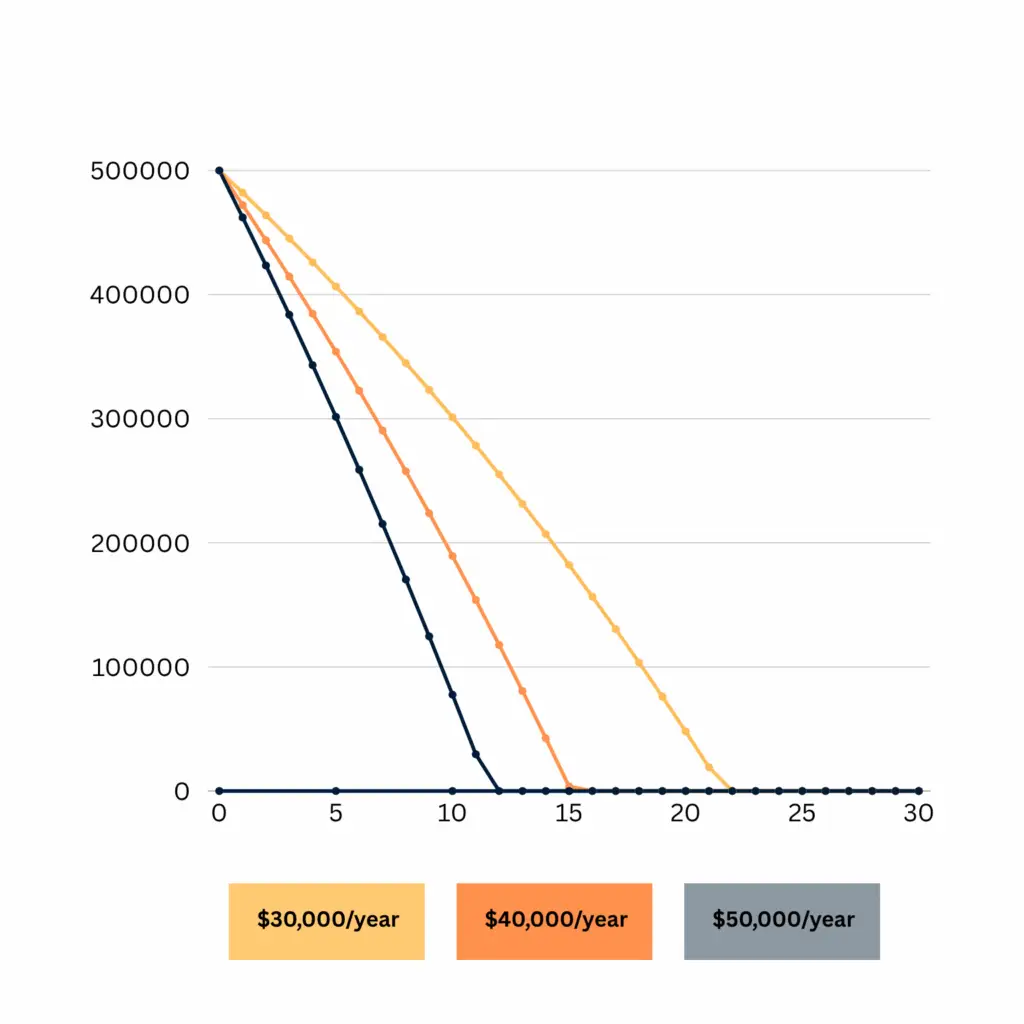

How long $500K lasts depends primarily on how much you spend each year and the investment return your balance earns. Here is an illustrative guide:

| Annual Spending | How Long $500K May Last |

|---|---|

| $30,000 per year | approximately 19 to 21 years |

| $40,000 per year | approximately 15 to 17 years |

| $50,000 per year | approximately 12 to 14 years |

These are illustrative estimates only. They assume a 2.4% inflation-adjusted real return with consistent annual withdrawals. Actual outcomes will vary significantly based on investment returns, fees and individual circumstances.

At $30,000 a year, $500K could carry you into your early 80s before the balance is substantially reduced. That is the point where the Age Pension is carrying most of the income load. At $40,000 a year, you reach a similar position in your mid to late 70s.

The investment return assumption matters more than most people realise. A balanced portfolio with some growth exposure typically outperforms a cash or conservative option over a 20 to 25 year retirement, even after accounting for market volatility. Scott and Phil covered this directly in Episode 1: Why Playing It Safe in Retirement Can Cost You More, which walked through how a conservative portfolio can actually run out of money faster than a growth one over a long retirement.

What Does a $30,000 Annual Retirement Budget Cover?

For a homeowner with no mortgage, $30,000 a year covers a genuine lifestyle. Here is how that budget typically distributes across common costs:

| Category | Percentage of Budget |

|---|---|

| Housing and Utilities | 22% |

| Food and Groceries | 18% |

| Healthcare and Insurance | 15% |

| Transport | 13% |

| Leisure and Travel | 10% |

| Clothing and Personal Care | 8% |

| Bills and Communication | 7% |

| Buffer and Miscellaneous | 7% |

This is a modest lifestyle but a stable and dignified one. Private health cover, a car, basic leisure and some short domestic travel are all within reach at this spending level for a homeowner paying no rent or mortgage.

Is $500,000 Enough to Retire On in Australia?

For many homeowning Australians with spending around $30,000 to $35,000 a year, $500K is enough to support retirement at 60, particularly when the Age Pension supplements income from 67. Whether it is enough for your situation depends on several factors:

Home ownership matters most. A homeowner with no rent or mortgage has fundamentally lower essential costs than a renter. The family home is also excluded from the Age Pension assets test. Both of these factors are critical to making $500K work in retirement.

The seven years from 60 to 67 are the most demanding. The Age Pension does not start until 67. From the day you retire at 60, your super funds everything for seven years with no government support. At $500K drawing $33,000 a year with modest returns, the balance reduces over this period before the pension provides relief.

Spending discipline in the early years is the key variable. Overspending in the first five years of retirement compounds over the following two decades and is the most common reason retirement plans come unstuck at this balance level.

Our retirement planning page has more on how Wealthlab approaches income planning for clients at different balance levels.

This Line Chart Showing how $500K depletes over 25–30 years under three spending levels: $30K, $40K, and $50K/year.

What the Age Pension Adds From 67

From age 67, the Age Pension becomes available subject to the assets test and income test. Current maximum rates as at March 2026 are:

- Single: approximately $31,223 per year

- Couple combined: approximately $47,070 per year

(Source: Services Australia. Rates are updated each March and September.)

A homeowner who retires at 60 with $500K and draws around $33,000 a year will arrive at 67 with a remaining super balance that, for most homeowners with no other significant financial assets, sits within assets test thresholds for at least a part Age Pension.

Even a part pension of $15,000 to $20,000 a year on top of a reduced super drawdown gives total retirement income of $40,000 to $45,000 a year. That is a very different picture to the $33,000 a year the super alone was carrying during the bridge years.

Understanding how the means test interacts with your specific balance and assets is where specific advice adds real value. Our Pension and Centrelink page explains how the tests work. Episode 9 of the Wealthlab podcast, When Super Fund Advice Can Cost You the Age Pension, covered a real case where poor advice cost a retiree significant Age Pension entitlements. At $500K, that kind of mistake is genuinely costly.

What the Average Retirement Age in Australia Tells Us

The average retirement age in Australia is currently around 63 to 64 for men and slightly lower for women. Most Australians retire with less super than they planned and earlier than they expected, often due to health issues, redundancy or carer responsibilities.

At $500K, retiring at 60 is slightly ahead of the average age but at a balance that is broadly in line with what many Australians actually retire with. Episode 19 of the Wealthlab podcast, Is Early Retirement a Trap? The $150K Gap Most Aussies Miss, found that the average couple retiring today has around $540K combined, around $150K below the ASFA comfortable standard. $500K for a single person is a meaningful balance given that context.

Common Retirement Mistakes That Reduce How Long $500K Lasts

Overestimating investment returns or spending beyond the plan. A common assumption is that super will earn 7 to 8% a year in retirement. After fees and in a conservative option, real returns are significantly lower. Building a plan on realistic return assumptions is more important than an optimistic one.

Forgetting to account for inflation. $30,000 in 2026 buys meaningfully more than $30,000 will buy in 2041. A retirement plan that does not build in inflation protection gradually loses purchasing power year by year.

Missing Age Pension eligibility. Many retirees at this balance assume they will not qualify and never investigate. The means test thresholds are updated twice a year and the structuring of assets around retirement can make a real difference to eligibility. Getting advice specifically on this before retiring is worthwhile.

Not reviewing the plan every few years. Spending, health, returns and government policy all change over a 25 to 30 year retirement. A retirement plan set at 60 and never revisited is unlikely to still be optimal at 75.

Use the free Wealthlab super calculator to run your own scenarios across different spending levels and return assumptions.

A General Retirement Scenario

For a single homeowner at 60 with $500K in super, spending around $32,000 a year:

Age 60 to 67: Drawing from super at around $32,000 a year. Investment returns partially offset the drawdown. Balance reduces over this period.

Age 67 onwards: Part Age Pension likely accessible for many homeowners at the remaining balance. Combined income from pension and reduced super drawdown potentially around $41,000 to $46,000 a year depending on the means test outcome.

Later retirement: Healthcare costs typically rise from the mid-70s. Building a buffer for this into the long-term plan is more realistic than assuming flat spending throughout retirement.

Individual outcomes vary considerably. This is an illustrative shape only.

FAQ: Retiring at 60 with $500K in Australia

How long will $500,000 last in retirement in Australia? At $30,000 a year with a 2.4% real return, $500K may last approximately 19 to 21 years for many people. At $40,000 a year, approximately 15 to 17 years. These are illustrative estimates. The Age Pension from 67 extends how far the remaining balance needs to stretch, since the super does not need to fund the full retirement income from that point. Actual outcomes depend on investment returns, fees and spending.

Is $500,000 enough to retire on in Australia? For many homeowning Australians with spending of around $30,000 to $35,000 a year, $500K can support retirement, particularly when combined with Age Pension income from 67. Whether it is enough for your situation depends on your actual living costs, home ownership, investment returns and total assets. Individual circumstances vary. This is general information, not personal advice.

Is $500,000 in super enough to retire at 60? At 60, the challenge is the seven-year gap to the Age Pension at 67. During that period, $500K funds everything. For a homeowner spending around $32,000 a year, that bridge is manageable for many people. Once the Age Pension supplements super from 67, the combined income position is more comfortable. Whether your specific situation works depends on factors beyond just the super balance.

How much money do I need to retire at 60 in Australia? The ASFA Retirement Standard estimates a single homeowner needs around $595,000 in super plus the Age Pension for a comfortable retirement. For a couple, around $690,000. These are benchmarks, not fixed minimums. Many Australians retire with less and live well, particularly homeowners with realistic spending expectations and Age Pension eligibility from 67. (Source: ASFA)

How long will $500K in super last in Australia? This depends on your annual drawdown and investment returns. At a 2.4% real return and $30,000 a year spending, approximately 19 to 21 years for many people. At $40,000 a year, approximately 15 to 17 years. These are illustrative estimates only. The Age Pension from 67 typically reduces the annual drawdown from super, extending how long the balance lasts.

What is the average retirement age in Australia? The average retirement age in Australia is currently around 63 to 64. Many Australians retire earlier than planned due to health issues, redundancy or carer responsibilities. Retiring at 60 is slightly earlier than average but common. The key consideration at 60 is the seven-year gap before the Age Pension begins at 67.

Will I get the Age Pension if I retire at 60 with $500K in super? Not at 60. The Age Pension begins at 67. By the time a retiree who started with $500K reaches 67 after seven years of drawdown, the remaining balance will often fall within homeowner assets-test thresholds for at least a part pension. Eligibility is assessed by Services Australia under the assets test and income test at age 67. Figures are current as at March 2026.

What if I retire at 60 but still have a mortgage? A mortgage on top of regular living costs pushes required annual drawdown significantly higher. At $500K, carrying ongoing debt into retirement is one of the factors that most commonly causes the numbers to not work. Our post on paying off your mortgage versus putting money into super covers the trade-offs in detail.

Talk It Through with Wealthlab

If you are approaching 60 with around $500K and working through whether retirement is realistic, getting clarity on your specific situation is worthwhile. The investment mix, drawdown rate, account-based pension setup and Age Pension structuring all interact, and decisions made early in retirement are harder to reverse later.

Wealthlab works with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how the general principles here might apply to your circumstances.

To compare how the numbers shift at nearby balances, our posts on Can I Retire at 60 with $480K? and Can I Retire at 60 with $520K? cover similar ground.