If you have saved $520,000 in super and are wondering whether you can retire at 60 in Australia, you are asking the right question at the right time. $520K is a meaningful balance. It is not enough to self-fund a 30-year retirement without any government support, but for many homeowning Australians with realistic spending habits, it can absolutely support retirement at 60 when the Age Pension is factored in from age 67.

The key is understanding what $520K can actually carry across three phases: the years before you can access super (if applicable), the seven-year bridge from 60 to 67, and the longer stretch where the Age Pension supplements your drawdown. This post walks through all three.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

How Much Money Do You Need to Retire at 60 in Australia?

The ASFA Retirement Standard is the most widely used benchmark for retirement adequacy in Australia. It estimates a single homeowner needs around $595,000 in super (plus the Age Pension) for a comfortable retirement, and a couple needs around $690,000. (Source: ASFA)

At $520K, a single retiree sits around $75,000 below the comfortable benchmark. That gap sounds significant but it is not insurmountable, especially for a homeowner who reaches 67 with Age Pension eligibility. The ASFA figures are benchmarks, not hard minimums. Many Australians retire with less and live well.

The more important question is not whether $520K meets a benchmark but whether it meets your actual needs across a retirement that could last 25 to 30 years.

How Long Will $520K Last in Retirement?

How long your super lasts depends primarily on how much you spend each year and how your balance is invested. Here is an illustrative guide based on consistent annual withdrawals:

| Annual Spending | How Long $520K May Last |

|---|---|

| $30,000 per year | approximately 20 to 22 years |

| $40,000 per year | approximately 16 to 18 years |

| $50,000 per year | approximately 13 to 15 years |

These are illustrative estimates only. They assume a 2.4% inflation-adjusted return with consistent withdrawals from age 60. Actual outcomes will vary based on investment returns, fees and personal circumstances.

At $30,000 a year, $520K could carry you into your early 80s before the balance is substantially depleted. That is the point where the Age Pension is doing most of the income work. At $40,000 a year, the balance runs further into your mid to late 70s before the pension takes over as the primary income source.

The investment return assumption matters significantly here. A balanced or moderately growth-oriented portfolio typically produces better long-term outcomes than a conservative or cash option, even in retirement. Scott and Phil covered the maths behind this in Episode 1: Why Playing It Safe in Retirement Can Cost You More, which is directly relevant if you are deciding where to keep your super at 60.

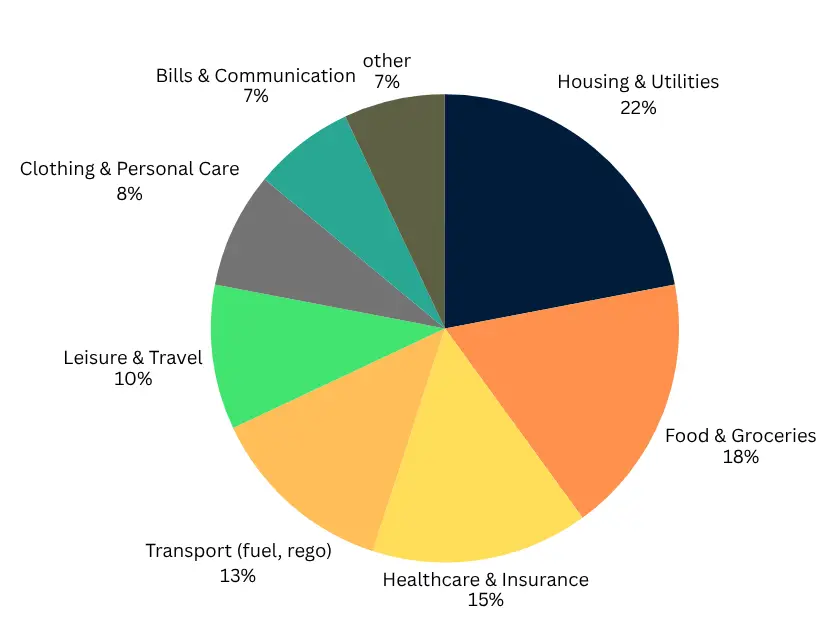

What Does $30K/Year Cover?

If you can manage your lifestyle around $30,000 per year, here’s how that budget may be distributed:

| Category | % of Budget |

|---|---|

| Housing & Utilities | 22% |

| Food & Groceries | 18% |

| Healthcare & Insurance | 15% |

| Transport (fuel, rego) | 13% |

| Leisure & Travel | 10% |

| Clothing & Personal Care | 8% |

| Bills & Communication | 7% |

| Other Essentials & Buffer | 7% |

What Does a $30K to $40K Annual Retirement Budget Cover?

For a homeowner with no mortgage, $30,000 to $40,000 a year can cover a genuine lifestyle in retirement. Here is how a $30,000 budget might be distributed across common expenses:

| Category | Percentage of Budget |

|---|---|

| Housing and Utilities | 22% |

| Food and Groceries | 18% |

| Healthcare and Insurance | 15% |

| Transport | 13% |

| Leisure and Travel | 10% |

| Clothing and Personal Care | 8% |

| Bills and Communication | 7% |

| Buffer and Miscellaneous | 7% |

This is not an extravagant lifestyle but it is a stable and genuinely comfortable one for a homeowner. Regular domestic travel, hobbies, dining out occasionally, private health cover and a reasonable car are all within reach at this spending level.

The Seven-Year Gap From 60 to 67

This is the part that catches most people out. The Age Pension does not begin at 60. It begins at 67, which means from the day you retire at 60, your super funds everything for seven years with no government support.

Drawing $35,000 a year from $520K over that seven-year window, with modest investment returns, means a meaningful portion of your balance is consumed before the Age Pension becomes available. The amount remaining at 67 then determines both your Age Pension eligibility and how long the rest of retirement is funded.

For a homeowner who manages spending carefully during the bridge years, the remaining balance at 67 will often sit within the assets test thresholds for at least a part pension. That changes the retirement income picture considerably.

Scott and Phil discussed the real cost of the pre-pension gap in Episode 19: Is Early Retirement a Trap? The $150K Gap Most Aussies Miss. The episode is worth watching if you are thinking through the 60 to 67 window carefully.

What the Age Pension Adds From 67

Once you reach 67 and meet the residency and means test requirements, the Age Pension becomes available. Current maximum rates as at March 2026 are:

- Single: approximately $31,223 per year

- Couple combined: approximately $47,070 per year

(Source: Services Australia. Rates are updated each March and September.)

Even a partial Age Pension of $15,000 to $20,000 a year on top of a modest super drawdown gives total retirement income of $40,000 to $45,000 a year for many homeowners at this balance level. That is a meaningfully different number to what the super alone can provide from age 60, and it is why planning for the Age Pension from the start, rather than treating it as an afterthought, is important at $520K.

Our Pension and Centrelink page explains how the assets test and income test work in practice and what structuring decisions affect the outcome. Episode 9 of the podcast, When Super Fund Advice Can Cost You the Age Pension, covered a real case where poor advice cost a client significant pension entitlements. At $520K, getting this right matters.

Who Can Make $520K Work at 60?

For most Australians, $520K is most workable at 60 when:

- You own your home outright with no mortgage

- Your genuine living costs sit at or below $35,000 a year

- You are comfortable drawing from super steadily rather than taking large lump sums early

- You understand the seven-year gap to the Age Pension and have a plan for it

- You have an investment mix that gives your balance a reasonable chance of growth across a long retirement

If you are still renting or carrying a mortgage at 60, $520K needs to work harder and the planning becomes more important, not less.

Use the free Wealthlab super calculator to run your own numbers across different spending and return assumptions.

Common Mistakes That Reduce How Long $520K Lasts

Overspending in the first five years. The early years of retirement often involve new spending on travel, home improvements or lifestyle changes. A sustained annual drawdown well above your planned amount early on compounds over the following 20 years.

Moving to an all-cash or fully conservative investment option at 60. Over a 25 to 30 year retirement, inflation erodes the purchasing power of a portfolio that barely grows. This is one of the more consequential decisions made at retirement and one of the least understood.

Assuming you will not qualify for the Age Pension. Many retirees at this balance level do not investigate their entitlement properly and miss out on pension income they were eligible for. Getting specific advice on the means test before you retire can add thousands of dollars a year in pension income.

Not reviewing the plan every few years. Spending, health, investment returns and government policy all change over a 25 to 30 year retirement. A plan built at 60 needs revisiting, not filing away.

A General Retirement Scenario

For a single homeowner at 60 with $520K in super, spending around $32,000 a year with a balanced investment mix:

Age 60 to 67: Drawing from super at around $32,000 a year. Investment returns partially offset the drawdown. Balance reduces over this period.

Age 67 onwards: Part Age Pension likely accessible for many homeowners at the remaining balance. Combined retirement income from pension and reduced super drawdown potentially around $42,000 to $48,000 a year depending on the means test outcome at that point.

Later retirement: Healthcare costs typically increase from the mid-70s. Building a modest buffer into spending projections for this period leads to more realistic planning.

Individual outcomes vary considerably. This is an illustrative shape only.

FAQ: Retiring at 60 with $520K in Australia

Can I retire at 60 with $520K in super? For many homeowning Australians with spending of around $30,000 to $35,000 a year, retirement at 60 with $520K is achievable, particularly when combined with Age Pension income from 67. Whether it works for your situation depends on your actual spending, home ownership, investment returns and total assets. Individual circumstances vary considerably. This is general information, not personal advice.

Is $520,000 enough to retire on in Australia? For a single homeowner with modest spending, $520K can support retirement in Australia when the Age Pension supplements income from 67. It sits below the ASFA comfortable benchmark of $595,000 for a single person but above the ASFA modest standard. Whether it is enough depends on your specific situation. Speaking with a financial adviser gives a more reliable picture than any general estimate.

How long will $520K last in retirement? At $30,000 a year with a 2.4% real return, $520K may last approximately 20 to 22 years for many people. At $40,000 a year, approximately 16 to 18 years. These are illustrative estimates. The Age Pension from 67 extends how far the remaining balance needs to stretch.

How much do I need to retire at 60 comfortably in Australia? The ASFA comfortable retirement standard for a single homeowner is approximately $595,000 in super plus the Age Pension. For a couple, it is approximately $690,000. These are general benchmarks, not fixed requirements. Many Australians retire with less and live comfortably, particularly homeowners with low debt and realistic spending expectations.

What is the Age Pension rate for singles in Australia in 2026? The current maximum Age Pension for a single person is approximately $31,223 per year as at March 2026. For couples the combined maximum is approximately $47,070 per year. Rates are updated each March and September. Eligibility is assessed by Services Australia under the assets test and income test at age 67.

What happens to my retirement income from 60 to 67 before the Age Pension starts? The seven years from 60 to 67 are funded entirely from your own super. There is no Age Pension or Centrelink support for retirees during this period. How well your super holds up across this bridge determines what remains at 67 and how much the Age Pension can then contribute. Managing spending and investment strategy during the bridge years is the most important planning task for anyone retiring at 60.

Should I retire at 60 or wait until 65 with $520K? Retiring at 65 means a two-year gap to the Age Pension instead of seven. For a balance of $520K, that shorter bridge changes the maths considerably. More of the balance survives to 67, which typically improves Age Pension eligibility and gives a higher combined income from 67 onward. Whether waiting five years is worth it depends on personal circumstances, health and employment options.

Talk It Through with Wealthlab

If you are approaching 60 with around $520K and working out whether the numbers can hold together, the most useful step is getting a clear view of your specific situation. The investment mix, drawdown rate, account-based pension setup and Age Pension positioning all affect how the next 25 to 30 years unfold.

Wealthlab works with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how the general principles here might apply to your circumstances.

To compare how the numbers shift at nearby balances, our posts on Can I Retire at 60 with $480K? and Can I Retire at 60 with $550K? cover similar ground.