$375,000 in super at 60 is a position that genuinely works for a homeowner, and understanding exactly how is more useful than a vague reassurance that “it depends.” It depends on specific things: your spending during the seven-year bridge to the Age Pension, whether you own your home, and how your super is invested and structured from day one of retirement.

Here is the full picture.

Accessing Super at 60: What You Need to Know

Preservation age in Australia is 60 for anyone born after 1 July 1964. Once you retire or cease an employment arrangement, your full $375,000 is accessible completely tax-free. There is no income tax on withdrawals from a taxed super fund after age 60, whether you take a lump sum or draw an income stream.

One action that makes an immediate financial difference: the day you retire, your super should switch from accumulation phase to pension phase. In accumulation, investment earnings are taxed at up to 15%. In pension phase, all investment earnings are completely tax-free. This does not happen automatically. You need to contact your fund and initiate an account-based pension. Setting it up before your last day of work ensures it activates on day one of retirement.

Source: ATO: Super withdrawal options (Current as at May 2026)

Please note: All figures, projections and scenarios in this article are for general illustration only. Individual outcomes depend on personal circumstances, spending levels, investment returns, fees and government policy. This is general information, not personal advice.

How Long Will $375,000 Last? The Full Picture

Using a net annual return of 5% after fees and investment tax in a balanced account-based pension:

| Annual spending | Balance at age 67 | Age Pension status at 67 | Estimated combined income from 67 |

|---|---|---|---|

| $20,000/yr | ~$309,000 | Part pension (~$20,000/yr) | ~$40,000 to $42,000/yr |

| $25,000/yr | ~$260,000 | Full pension (~$29,000/yr) | ~$40,000 to $43,000/yr |

| $30,000/yr | ~$212,000 | Full pension (~$29,000/yr) | ~$40,000 to $42,000/yr |

| $35,000/yr | ~$164,000 | Full pension (~$29,000/yr) | ~$38,000 to $40,000/yr |

| $40,000/yr | ~$118,000 | Full pension (~$29,000/yr) | ~$36,000 to $38,000/yr |

A striking insight from the table: Combined income from 67 is remarkably similar across spending levels from $25,000 to $40,000 per year during the bridge. The Age Pension compensates for a depleted balance. The difference between disciplined and undisciplined bridge spending is not the income you’ll receive from 67. It’s the buffer you’ll have when unexpected costs arise in your 70s and 80s.

At $20,000 per year, you arrive at 67 with $309,000, above the full pension threshold of $321,500 for a single homeowner. You’d receive a part pension of approximately $20,000 rather than the full $29,000. Paradoxically, spending more during the bridge (reducing the balance to below $321,500) can actually result in a higher total income from 67.

Source: Services Australia: Age Pension (Current as at May 2026)

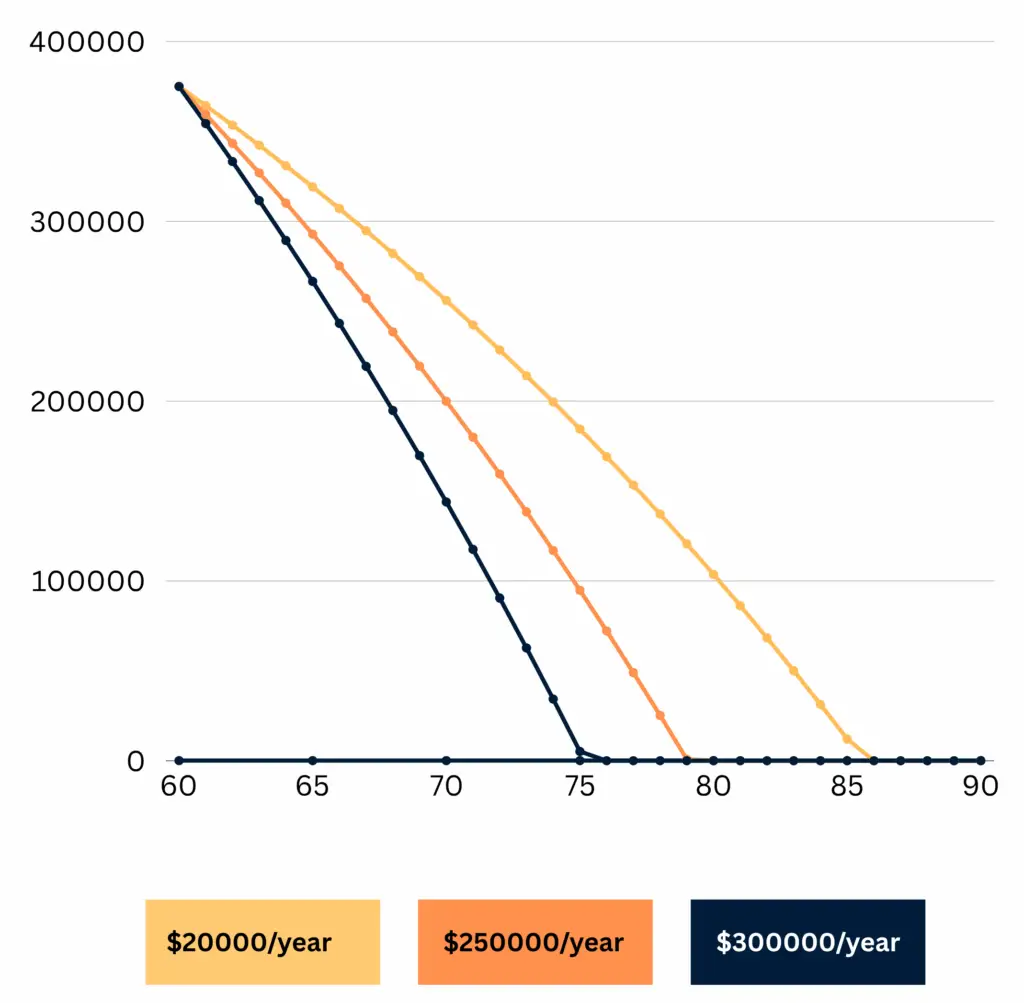

This Line Chart Showing $375K Super Depletion from Age 60 to 9. Visualising your super balance over time at various spending levels helps you clearly compare trade-offs. Spending less each year stretches your funds considerably.

Where $375K Sits Against National Benchmarks

Average super balance for Australians aged 60 to 64 (APRA data):

- Men: approximately $396,000

- Women: approximately $313,000

At $375,000 you’re within reach of the male average and comfortably above the female average. You’re broadly in the national midpoint for your age group.

ASFA Retirement Standard (February 2026):

- Comfortable single homeowner at 67: $630,000

- Modest single homeowner at 67: $110,000

$375K sits between these benchmarks. The $255,000 gap to the comfortable standard is real but it’s significantly bridged by the Age Pension. The ASFA comfortable standard is modelled at retirement age 67 with partial pension support from that point. Someone retiring at 60 with $375K draws down over seven years, arrives at 67 within full pension territory, and from that point receives $29,000 per year in pension plus whatever super drawdown they choose. That combined income often approaches or reaches ASFA comfortable territory for a homeowner with no debt.

Source: ASFA Retirement Standard, February 2026

The Seven-Year Bridge: Planning 60 to 67

Retiring at 60 means seven full years before the Age Pension starts at 67. During that window, your $375K funds everything.

At $28,000 per year, you draw approximately $196,000 over seven years. On $375K starting balance growing at 5%, that leaves approximately $234,000 at 67. A single homeowner with $234,000 in total assets is well below the $321,500 full pension threshold. The full Age Pension of $29,000 per year begins immediately.

The three most impactful bridge decisions:

Stay invested, not in cash. At 60 your money needs to last potentially 30 years. Moving to cash at 2% versus staying in a balanced option at 5% costs approximately $68,000 in lost growth on $375K over the seven-year bridge alone. As Scott covered in Episode 1 of the Wealthlab Podcast: “Why Playing It Safe in Retirement Can Cost You More,” being too conservative in the early years of retirement is one of the most common and costly decisions Australians make.

Switch to pension phase immediately. Do not leave $375K in accumulation phase after retiring. Earnings taxed at up to 15% in accumulation versus zero in pension phase. Over seven bridge years the difference on $375K is meaningful.

Keep drawdowns close to what you actually need, not what you want. The bridge years are where the balance either holds or depletes significantly. Every $5,000 per year less in drawdown over seven years adds approximately $35,000 to $40,000 to your balance at 67.

What $375K Supports in Practice: Three Retirement Scenarios

Scenario 1: Single homeowner, no debt, $28,000 per year spending

Drawing $28,000 per year through the bridge, you arrive at 67 with approximately $221,000. Well within full Age Pension territory. Combined income from 67: $29,000 pension plus $10,000 to $12,000 super drawdown equals approximately $39,000 to $41,000 per year.

For a homeowner with no mortgage, that covers grocery and household costs, utilities and rates, basic private health insurance, a reliable car, regular social activities and annual domestic travel. It sits above the ASFA modest standard of $36,700 and approaches a genuinely comfortable lifestyle for someone with fixed costs under control.

From a pure longevity standpoint, the balance at 67 of $221,000 plus a continuing $29,000 Age Pension floor means income continues indefinitely regardless of what happens to the super balance. The pension is permanent once you qualify. Your super supplements it and extends the total income, not the other way around.

Scenario 2: Couple with combined super of $375K to $500K

For a couple, $375K combined (or with one partner at $375K and the other contributing from a smaller balance) is a different picture. Two Age Pension entitlements apply from 67. The couple full pension of $43,700 per year combined is a more substantial income floor. Two people sharing housing costs, utilities and a car spend far less per person than the ASFA single figures suggest. A couple with combined super of $375K to $500K, a paid-off home and no debt can live genuinely well from 67.

Scenario 3: Planning around a Transition to Retirement pension

If you’re 58 or 59 and planning to retire at 60, a Transition to Retirement pension from 58 allows you to draw up to 10% of your balance per year as income while still working, allowing you to reduce to part-time hours. On $375K that’s up to $37,500 per year supplementing a reduced salary, while your employer continues paying SG on your work income. Your balance continues to receive contributions and investment returns. This can be an effective two-year strategy for someone who wants to ease into retirement rather than stopping abruptly. See our retirement planning page for a full breakdown of TTR strategy.

The Age Pension Assets Test: What $375K Means at 67

Current homeowner assets test thresholds (March 2026):

| Full pension | Part pension cut-off | |

|---|---|---|

| Single | Assets below $321,500 | Up to ~$695,500 |

| Couple combined | Assets below $481,500 | Up to ~$1,045,500 |

Source: Services Australia: Assets test (Current as at May 2026)

At $375K with $25,000 to $30,000 per year spending during the bridge, you arrive at 67 with approximately $212,000 to $260,000. Both figures are below the $321,500 full pension threshold. Full Age Pension.

At $20,000 per year spending, you arrive at 67 with approximately $309,000, just below the full pension threshold but very close to it. The risk of ending up slightly above the threshold due to good investment returns or timing is worth noting. A planner can help you model this precisely.

Phil and Dan covered how the assets test and income test interact with super drawdown in Episode 10 of the Wealthlab Podcast: “How the Age Pension Really Works.”

Before You Retire at 60: Six Actions to Take

1. Use catch-up contributions before 30 June 2026. If your total super balance is under $500,000 and you have unused concessional cap space from previous years, unused amounts from 2020/21 expire permanently on 30 June 2026. With $375K you’re under the $500K threshold. Log into myGov now and check your carry-forward balance. A final salary sacrifice contribution using this space before the deadline could add $10,000 to $25,000 to your balance. Scott and Phil covered this in Episode 7 of the Wealthlab Podcast.

2. Switch to an account-based pension on day one. Contact your fund before your last day and set up the pension to activate immediately. Don’t leave money in accumulation after retiring.

3. Review your investment option. Confirm you’re in a balanced or moderate growth option appropriate for a 25 to 30 year retirement horizon. Not cash, not a conservative bond-heavy option.

4. Check insurance inside super. Life and TPD cover in accumulation does not automatically transfer to pension phase. Confirm what you hold before switching, particularly if you have financial dependants.

5. Update your binding beneficiary nomination. Most binding nominations expire every three years. A lapsed nomination means your super may not go where you intend. Check and renew it before your last day of work.

6. Apply for the Commonwealth Seniors Health Card. Provides cheaper PBS medications, bulk-billed GP visits at many practices, and state government concessions on rates and utilities. Worth $2,000 to $3,500 per year. Apply through Services Australia before retiring so it activates immediately.

Should You Retire at 60 or Work a Little Longer?

Every additional year of work at $375K improves the retirement position meaningfully. One year at $80,000:

- Employer SG adds approximately $9,600

- Avoids approximately $25,000 to $30,000 in drawdown

- Allows $375K to grow rather than shrink (approximately $18,750 at 5%)

- Combined improvement: approximately $53,000 to $58,000

That’s roughly a 14% improvement in your starting retirement position from a single year. At $375K the proportional gain from each extra year is larger than at $500K or $600K.

But the financial case is not the complete picture. As Scott discussed in Episode 19 of the Wealthlab Podcast: “Is Early Retirement a Trap? The $150K Gap Most Aussies Miss,” the spending wave in retirement peaks in the early active years when you’re healthy and able. Deferring retirement to build a larger balance can mean a higher number at 63 but fewer active years to spend it. The numbers inform the decision. They don’t make it.

Frequently Asked Questions

Can I retire at 60 with $375,000 in super in Australia?

Yes, particularly as a homeowner with no significant debt. Drawing $25,000 to $28,000 per year in a balanced investment option, $375K bridges seven years to Age Pension eligibility at 67, arriving with approximately $220,000 to $260,000. As a single homeowner, that qualifies for the full Age Pension of approximately $29,000 per year. Combined income from 67 of approximately $39,000 to $42,000 is workable and stable for a homeowner with manageable fixed costs.

How long will $375,000 in super last at 60?

At $28,000 per year spending with 5% net returns, the balance tracks to approximately $221,000 at 67. From that point the Age Pension of $29,000 per year reduces the required super drawdown to $10,000 to $12,000 per year, meaning the remaining balance lasts well into the mid to late 80s. At $35,000 per year spending, the balance is largely depleted by the mid 70s but the full Age Pension continues as a permanent income floor.

Will I get the full Age Pension at 67 if I retire at 60 with $375K?

At $25,000 per year or more in spending during the bridge, yes. You arrive at 67 with approximately $260,000 or less, well below the $321,500 full pension threshold for a single homeowner. At $20,000 per year you arrive with approximately $309,000, just below the threshold but worth monitoring as investment returns could push the balance over.

What is the Age Pension age in Australia?

67 for anyone born on or after 1 January 1957. Retiring at 60 means seven years of fully self-funded retirement before any government income support begins.

What is the minimum super drawdown at 60?

The minimum annual drawdown from an account-based pension for someone under 65 is 4% of the opening balance. On $375,000 that is $15,000 per year. You can draw more at any time. Drawing the minimum and supplementing with modest part-time income during the bridge years is one effective way to preserve more capital for when the Age Pension starts at 67.

Is $375K above or below average super for a 60-year-old in Australia?

Above average for women (approximately $313,000 average at 60 to 64) and just below average for men (approximately $396,000). You’re broadly in the national midpoint for Australians approaching retirement.

What is a Transition to Retirement pension and should I use one?

A TTR pension lets you access up to 10% of your super balance per year as income while still working from age 60. It’s useful for people who want to reduce to part-time hours in the two to three years before fully retiring, allowing reduced salary to be topped up with super income while employer contributions continue building the balance.

What happens if I have a mortgage at 60 with $375K in super?

A remaining mortgage reduces your annual living costs net of mortgage repayments, which may force you to draw more from super during the bridge years and arrive at 67 with a smaller balance. Depending on the loan size, using a partial lump sum from super at 60 to clear the mortgage may be worth considering. Whether this makes sense depends on your mortgage rate, remaining balance and drawdown timeline. See our guide on should I pay off my mortgage or put money in super.

See What Your Numbers Actually Look Like

The scenarios above use standard assumptions. Your actual retirement income depends on your specific spending, home ownership, partner’s position, health and investment returns.

The free Wealthlab super calculator shows how your balance tracks at different spending levels and what the Age Pension adds from 67, in about two minutes.

If you want a proper retirement income plan for your specific situation, book a free chat with the Wealthlab team. No pressure, no jargon.