The honest answer is: yes, it is possible, but it requires going in with a clear picture of what $260K can and cannot do. For a single homeowner spending carefully, $260K can bridge the gap to the Age Pension. For a couple or anyone expecting a comfortable lifestyle straight away, the numbers are tighter than they might look.

This article breaks down exactly what $260K means for retirement at 60, how long it can realistically last, what happens at 67, and what most people in this position should be thinking about now.

What Happens at 60 with $260K in Super?

At 60, you’ve hit your preservation age. If you stop working, you can access your super tax-free through an account-based pension. That’s the good news.

The less comfortable reality is that the Age Pension doesn’t start until 67. That’s a seven-year gap where you’re entirely self-funded, covering housing, food, healthcare and everything else from your savings alone.

At $28,000 to $30,000 a year in spending, $260K is enough to carry most homeowners through those seven years with something still left over when the pension kicks in. It requires discipline, but it is workable.

What $260K does not support on its own is a comfortable retirement as defined by ASFA. For 2026, ASFA puts a comfortable lifestyle for a single person at around $54,000 a year and for a couple at around $77,000. Those numbers require a much larger balance. But a modest retirement at $260K, for a homeowner without debt, is a different conversation.

How Long Will $260K Last at 60?

The table below shows a rough projection for a single homeowner spending $28,000 to $30,000 a year, with a 5% net return inside an account-based pension.

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 60 | $260,000 | $28,000 | $11,600 | $243,600 |

| 61 | $243,600 | $28,500 | $10,755 | $225,855 |

| 62 | $225,855 | $29,000 | $9,843 | $206,698 |

| 63 | $206,698 | $29,500 | $8,860 | $186,058 |

| 64 | $186,058 | $30,000 | $7,803 | $163,861 |

| 65 | $163,861 | $30,000 | $6,693 | $140,554 |

| 66 | $140,554 | $30,000 | $5,528 | $116,082 |

| 67 | $116,082 | Pension starts | ~$106,000 |

By 67, there’s still around $106,000 in super and the Age Pension begins supplementing income. For a single homeowner, a balance of $116,000 at 67 falls well under the full pension assets test threshold, which sits around $314,000 for a single homeowner (current as at May 2026, Services Australia). That means near-full pension entitlements.

Please note: The figures above are approximate and for illustrative purposes only. Individual outcomes will vary based on your spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

The Age Pension Changes Everything at 67

The full Age Pension for a single person is currently around $29,754 a year including supplements. For a couple combined, it’s around $44,856 (current as at May 2026, Services Australia). These figures are typically updated each March and September.

Once the pension starts, the pressure on your super drops significantly. Instead of drawing $28,000 to $30,000 entirely from your own savings, the pension covers a large part of that. Your super then needs to fund only the gap between what the pension pays and what you actually spend.

For someone with $106,000 in super at 67 spending $30,000 a year, the Age Pension covers most of that. The remaining balance can be drawn down gradually over the next 10 to 15 years, and by most projections, the combination carries through to the mid-80s.

On the podcast, Phil and Dan ran through exactly this kind of scenario in Episode 10, “How the Age Pension Really Works”. If you want a clear walkthrough of how the assets test and income test interact with a balance like this, it’s worth a listen. Watch it on YouTube or find it on Spotify.

What the ASFA Numbers Say

According to the ASFA Retirement Standard (updated February 2026):

- Single homeowner, modest lifestyle: $35,199 a year

- Single homeowner, comfortable lifestyle: $54,240 a year

- Couple homeowners, modest lifestyle: $50,866 a year

- Couple homeowners, comfortable lifestyle: $77,375 a year

At $28,000 to $30,000 a year, the scenario above sits below ASFA’s modest standard. That’s the honest reality of $260K at 60. It is not a comfortable retirement by the numbers, but for homeowners with no debt and realistic expectations, many Australians do manage a decent quality of life on less than the ASFA modest figure, particularly in the early years of retirement when spending tends to be lower. you budget to around $28,000 to $30,000 a year during the 60 to 67 gap before the Age Pension starts.

What $260K at 60 Actually Requires

Owning your home outright is probably the single biggest factor. If you’re still renting or carrying a mortgage into retirement, $260K becomes very hard to stretch. The assumption in every projection above is no housing costs. If that’s not your situation, the picture changes considerably.

Spending discipline in the first few years matters more than most people realise. The early years of retirement have a disproportionate impact on how long savings last. Drawing heavily from a modest balance in years one and two can create problems that compound for decades. The sequencing risk Scott covered in Episode 1 of the Wealthlab Podcast applies here too. A poor start to drawdowns, whether from high spending or a bad market run, can shorten funding by years. Watch Episode 1 on YouTube.

Keeping some growth in your investments matters in retirement, not just before it. Sitting entirely in cash when inflation is running at 3% means your balance is shrinking in real terms every year even before withdrawals. A mix of growth and defensive assets is worth considering. Speak with a qualified financial adviser about what mix suits your circumstances.

Part-time work in your early 60s can make a meaningful difference. Even modest income between 60 and 63 delays the point where you start drawing down super, and that delay compounds positively over time.

Want to run your own numbers and see how your balance holds up under different scenarios? The free Wealthlab super calculator takes a couple of minutes and gives you a clearer picture than any general table can.

Common Mistakes to Avoid

Taking large lump sums early is the most common issue. The temptation to knock off a renovation or take a trip in year one is understandable, but with a modest balance, large early withdrawals can be very hard to recover from.

Assuming the Age Pension is automatic. You need to apply for the Age Pension through Centrelink, and the assets and income tests can catch people off guard. A balance that seems modest may still affect your entitlement if it sits in certain structures. Getting advice on this before you hit 67, not after, is the move most people wish they’d made.

Forgetting healthcare costs. The ASFA figures include private health insurance for good reason. Healthcare costs tend to rise sharply in the 70s and 80s, and a $260K retiree who hasn’t factored this in may find their buffer thinner than expected.

Our retirement planning page covers more on the structural decisions worth getting right before you retire.

How Does $260K Compare to Average Balances?

According to APRA data, the average super balance for Australians aged 60 to 64 sits around $360,000 to $400,000 for men and considerably lower for women on average. So $260K is below the average for men in this age group, roughly in line with or above average for women, depending on career history.

Average balances are interesting as context but they’re not the number that matters for your retirement. What matters is whether your specific balance, combined with your spending, your housing situation and your pension eligibility, adds up to enough. For a more detailed look at where the numbers sit, read our post on what the average super balance at 60 in Australia looks like and what it means.

For women in particular, this is a topic worth understanding in detail. Episode 17 of the Wealthlab Podcast covers the gender super gap, life expectancy differences and what they mean for retirement planning. Watch it here.

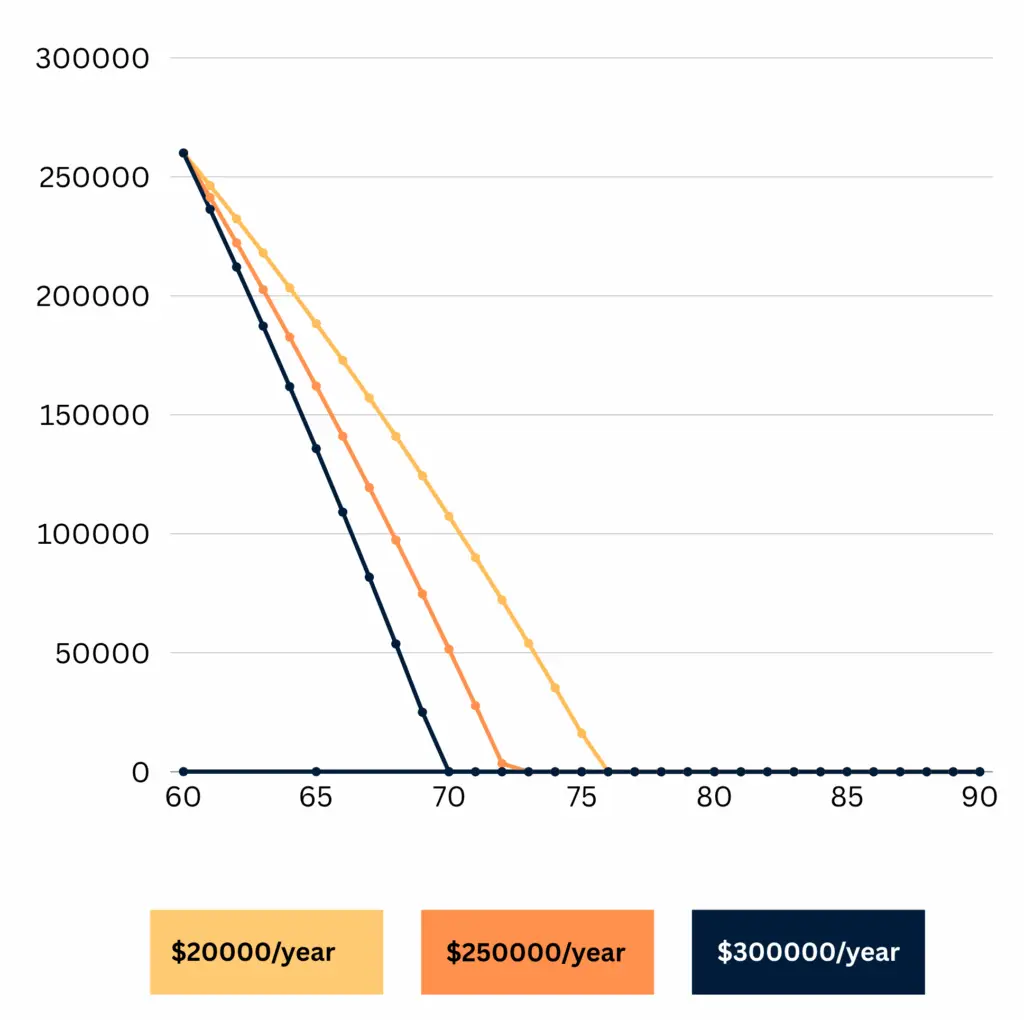

This Line Chart Shows Depletion of $260K from age 60 to 90 at $20K, $25K, $30K annual spending

FAQ: Can I Retire at 60 with $260K?

Is $260K enough to retire at 60 in Australia? For a single homeowner spending around $28,000 to $30,000 a year, it can work. It funds a modest retirement, not a comfortable one as ASFA defines it. With careful drawdowns and the Age Pension starting at 67, the money can last into the 80s and beyond for many people. Individual circumstances vary significantly.

How long does $260K last in retirement? At $28,000 to $30,000 a year spending and around 5% net annual return in an account-based pension, $260K lasts roughly seven to eight years before drawing down significantly. Once the Age Pension supplements income from 67, the remaining balance stretches considerably further.

Will I qualify for the Age Pension with $260K at 60? Almost certainly by the time you reach 67. Drawing down over seven years from $260K typically leaves a balance well under the full pension assets test threshold for a single homeowner, currently around $314,000. Your home is exempt from the assets test.

What is the Age Pension threshold for a single homeowner in 2026? The full Age Pension assets test threshold for a single homeowner is around $314,000 (current as at May 2026). The cut-off for any pension is around $695,500. These figures are updated by the government each March and September. For current rates, check Services Australia.

Can I access my super at 60? Yes, if you have retired from the workforce. Once you stop working and meet the conditions of release, you can access your super tax-free from age 60. If you’re still working, a transition to retirement (TTR) pension lets you access limited amounts. See our superannuation page for more detail.

What lifestyle does $260K support at 60? For a debt-free homeowner, a modest lifestyle covering groceries, utilities, healthcare, local activities and some domestic travel. It does not support frequent international travel, significant gifts to family or a high-discretionary lifestyle without supplementary income.

Is retiring at 60 with $260K riskier than waiting? Generally yes. Every extra year you work grows your super, reduces drawdown years and improves your Age Pension position at 67. Whether the trade-off is worth it is a personal decision. Many people in this position look at part-time work in their early 60s as a middle path, reducing hours without fully stopping.

What to Do Next

If you’re approaching 60 with around $260K in super, the most useful thing you can do is get clarity on your specific numbers before you make any decisions. The Age Pension interaction with your super, your housing situation, your spending expectations and your investment structure all affect the outcome in ways that general projections cannot capture.

Not sure where you stand?or take the free Wealthlab retirement quiz or a general read on your retirement position. Or if you’d like to talk through your situation with someone who can look at your actual numbers, book a free callee call.