Reaching age 60 with $265,000 in super might not seem like a lot especially when media headlines often talk about needing a million dollars or more. But the truth is, retiring at 60 with $265K is possible in Australia. It won’t be a luxury lifestyle, but with strategic planning, government support later on, and modest living, you can make it work.

What Happens Financially When You Retire at 60 with $265K in Australia?

Turning 60 is a major retirement milestone in Australia. Here’s why:

- You’ve reached your preservation age, meaning you can now access your super tax-free, provided you’ve retired.

- However, you’re still seven years away from being eligible for the Age Pension, which begins at 67.

- That means from 60 to 67, you’re fully responsible for funding your lifestyle including housing, food, transport, and healthcare using your own resources.

Retiring at 60 with $265K requires careful budgeting and smart management of your super.

What Retirement Costs Look Like When You Retire at 60 with $265K

Let’s keep this simple. According to the ASFA Retirement Standard (March 2024), retirement costs vary depending on your lifestyle:

- Modest lifestyle (single): ~$32,000/year

- Comfortable lifestyle (single): ~$51,000/year

These figures assume you own your home, rely on public healthcare, and aren’t paying rent. With $265K, living modestly is possible, especially if you budget wisely and manage your expenses during the 60–67 gap before the Age Pension starts.

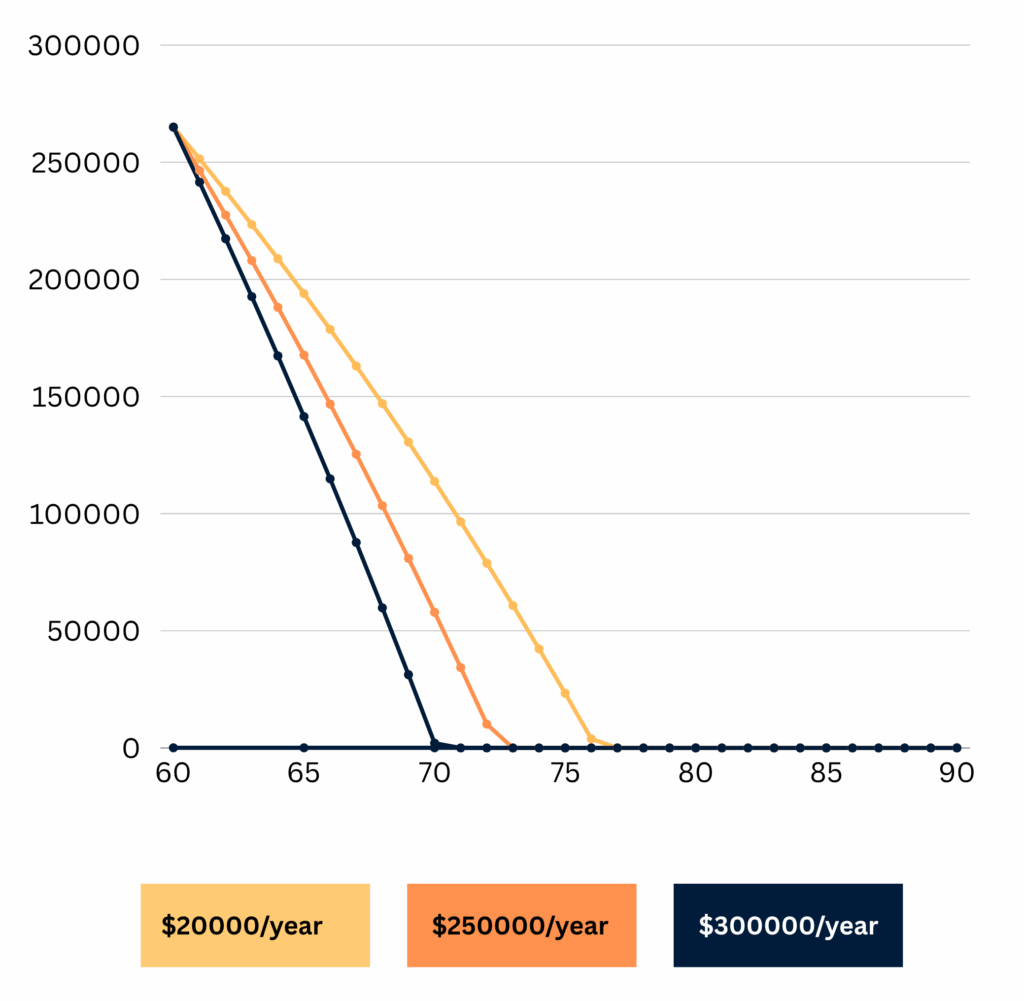

This line chart showing depletion of $265K from age 60 to 90 under three spending levels: $20K, $25K, and $30K. This will help visualise your options clearly.

How Long Will $265k Last in Retirement?

Here’s a simple forecast assuming:

- Annual drawdown: $28,000–$31,000

- Investment return: 3%

| Age | Starting Balance | Withdrawal | Growth (3%) | Ending Balance |

|---|---|---|---|---|

| 60 | $265,000 | $28,000 | $6,300 | $243,300 |

| 61 | $243,300 | $28,500 | $5,800 | $220,600 |

| 62 | $220,600 | $29,000 | $5,200 | $196,800 |

| 63 | $196,800 | $29,500 | $4,500 | $171,800 |

| 64 | $171,800 | $30,000 | $3,800 | $145,600 |

| 65 | $145,600 | $30,500 | $2,900 | $118,000 |

| 66 | $118,000 | $31,000 | $2,300 | $89,300 |

| 67 | $89,300 | $10,000 | $2,600 | $81,900 |

This shows that careful budgeting can bridge the 60–67 gap, leaving a modest buffer to complement the Age Pension once it starts.

What Happens at Age 67?

At age 67, you’re eligible for the Age Pension but it’s not automatic. You must pass both an income test and an assets test through Centrelink.

Current Full Pension Rates (as of July 2024):

- 👤 Single: ~$29,000/year

- 👥 Couple (combined): ~$43,800/year

A reduced super balance makes you more likely to qualify for the full or part pension. Once this support kicks in, you may only need to draw down small amounts from your super to cover your total annual expenses.

How to Make Retirement Work on $265,000

1. Own Your Home

Owning your home is one of the biggest advantages in early retirement. Without rent or mortgage payments, your yearly costs drop significantly. It becomes much easier to live on $28,000–$30,000 per year.

2. Set Up an Account-Based Pension

Turn your super into a retirement income stream instead of withdrawing lump sums. This keeps your income tax-free, provides regular payments, and helps manage spending in a more controlled way.

3. Live Slightly Below the Modest Lifestyle Standard

Try to live on $25,000–$28,000/year. Use government concessions (like health card discounts), stick to a budget, and avoid lifestyle inflation. Every dollar saved in the early years stretches your super further.

4. Keep a Balanced Investment Strategy

Hold part of your funds in growth assets to stay ahead of inflation, but keep enough cash for 1–2 years of living expenses. A low-risk portfolio can still grow your super modestly without excessive risk.

5. Work Part-Time Until Age 62 or 63 (If Possible)

A few hours a week can preserve thousands in super. It also gives structure, connection, and may improve your Age Pension eligibility by reducing how much you draw from your super too early.

So, Is $265K Enough?

It depends but it can be enough if you’re strategic. Your retirement might be modest, but with smart planning, Age Pension, and lifestyle adjustments, you could live comfortably.

What Kind of Lifestyle Can You Expect?

| Category | Expectation |

| Housing | Must own your home |

| Food & Utilities | Covered through modest budgeting |

| Travel | Local trips; overseas holidays may be limited |

| Healthcare | Public system, limited extras |

| Discretionary | Low to moderate spending on non-essentials |

Mistakes to Avoid on a $265k Retirement Plan

❌ Assuming you can access super and Age Pension together

❌ Overspending in the early years

❌ Not considering inflation and rising costs

❌ Withdrawing large lump sums

❌ Ignoring professional advice or modelling

Ready to Retire with $265k? Let Wealthlab Help You Plan With Confidence

You don’t need a million dollars to retire just a smart plan. At Wealthlab, we specialise in helping Australians like you retire securely, even with modest balances.

- Super withdrawal strategies

- Retirement income modelling

- Age Pension maximisation

📞 Book a consultation now to map out your ideal path from 60 to 90 and beyond.