Can you retire at 60 with $300K in super in Australia? The honest answer is yes, for some people, no for others, and it hinges on three things more than anything else: whether you own your home, whether you’re single or part of a couple, and how you plan to bridge the seven-year gap before the Age Pension kicks in at 67. $300K is below what ASFA suggests you need for a comfortable retirement, but it isn’t far off the median balance for Australians in their early 60s, and plenty of people do make it work. They just don’t make it work by accident.

This guide walks through what retiring at 60 with $300K actually looks like in practice. The numbers, the trade-offs, the most common traps we see in our work with clients, and where the real difference between “it works” and “it doesn’t” actually sits.

What the Benchmarks Say in 2026

The ASFA Retirement Standard (February 2026 update) raised the benchmarks for the first time in three years. A single homeowner now needs approximately $630,000 to fund a comfortable retirement at 67, and a couple needs around $730,000 combined. These figures assume you own your home and will receive a part Age Pension.

A “comfortable” retirement covers private health insurance, a reliable car you can replace when needed, annual domestic travel and an overseas trip every few years, regular dining out, and modest discretionary spending. It is not luxury. It is a solid, secure retirement that doesn’t require checking the bank balance every week.

$300K falls well short of those targets. But ASFA also publishes a “modest” retirement standard, which covers the basics with limited capacity for extras, and the lump sum for a modest retirement is much lower at around $110,000 single / $120,000 couple, because the Age Pension does most of the heavy lifting at that level.

Where does $300K leave you? Somewhere in between, and that’s the real question this post is trying to answer.

It helps to compare against actual super balances rather than benchmarks alone. ABS Household Income and Wealth data shows the average super balance for men aged 60 to 64 is around $395,000, and for women around $313,000. $300K is not unusual at all. It just requires a more deliberate strategy than a balance closer to the ASFA comfortable target.

The Core Problem: The 7-Year Gap Before the Age Pension

This is the structural challenge with retiring at 60, regardless of your balance. You can access your super tax-free from 60 (once you’ve met a condition of release), but the Age Pension doesn’t start until 67. That creates a seven-year window where your super carries everything.

If you draw $30,000 a year from $300K for seven years without any investment return, you’d have roughly $90,000 left when you turn 67. With a modest investment return of 4 to 5 per cent per year in an account-based pension, the balance erodes more slowly, but the maths is still tight.

This is also where investment choice matters most, and where we see the most expensive mistakes. Scott and Phil unpacked this on the podcast with a stark example. A couple with $500K in super spending $75K a year. In a growth portfolio expected to return 6 to 7 per cent, the money funds retirement comfortably into their late 90s. In a conservative portfolio returning 3 to 4 per cent, the same couple runs out 15 years earlier. Same starting balance, same spending, completely different outcomes from the asset allocation alone. The full breakdown is in Episode 1 of the Wealthlab Podcast.

This matters acutely at $300K because there’s no margin for a 15-year early depletion. The investment option you sit in through the gap years is one of the biggest levers you have.

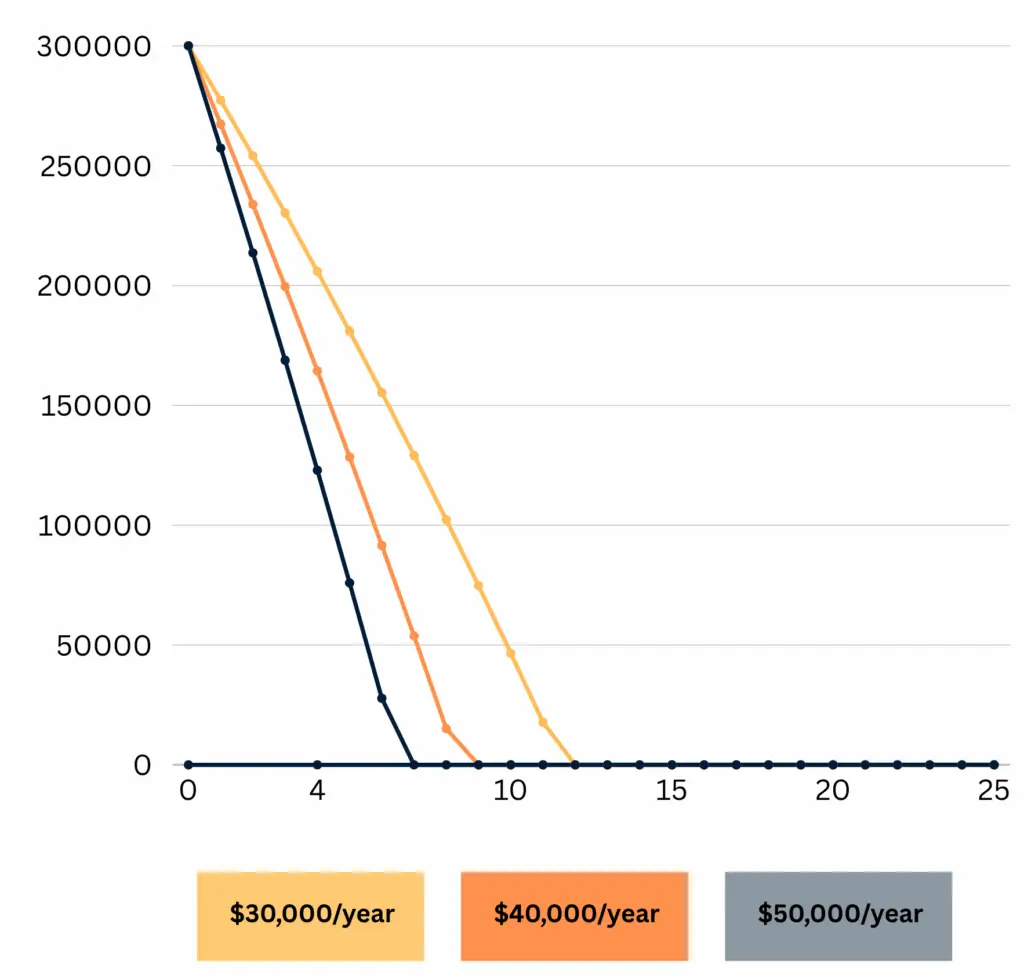

How Long Does $300K Last at Different Spending Levels?

These figures assume a 4% net annual return (a moderately conservative account-based pension) and starting drawdown at age 60. They are general illustrations, not predictions.

| Annual Spending | Super Balance at 67 | Approximate Balance at 75 |

|---|---|---|

| $25,000 per year | approximately $130,000 | approximately $60,000 |

| $35,000 per year | approximately $50,000 | depleted around age 71 |

| $45,000 per year | depleted around age 65 | gone |

The Age Pension changes the picture significantly from age 67 onwards. A single homeowner with $130,000 in super and no other significant assets would likely receive close to the full Age Pension of $1,200.90 per fortnight (approximately $31,223 per year, current as at 20 March 2026). For a couple, the combined full Age Pension is $1,810.40 per fortnight (approximately $47,070 per year).

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees, indexation, and current government policy. This is general information, not personal advice.

If you want to model your own numbers, the free Wealthlab super calculator lets you plug in your balance, age and spending target and see how the projection tracks for your situation.

Line chart showing how $300K depletes under three annual spending scenarios over 25 years.

What the Age Pension Adds to the Equation

The Age Pension is not means-tested on your home, which is one of the most important things to understand at this balance level. If you own your home outright, the home doesn’t count toward the assets test. That means a homeowner with $300K in super and modest savings is likely to receive a significant pension from 67.

For a couple retiring at 60 with $300K combined, spending carefully through the seven-year gap and arriving at 67 with $100,000 to $150,000 in super remaining, the Age Pension likely covers most of their living costs. Super becomes a top-up rather than the sole income source.

For a single person the same logic applies but with less margin for error. The single full Age Pension ($31,223 per year) covers modest living costs for a homeowner. Adding $1,000 to $2,000 per month in super drawdown on top gets you close to a liveable income.

Phil and Dan walked through real Age Pension case study numbers in Episode 10 of the Wealthlab Podcast, including how the timing of major asset sales in the years before pension age can dramatically affect both your CGT bill and your eventual pension entitlement. Worth a listen if you’re in the years leading up to a pension claim.

Single vs Couple: The Numbers Are Very Different

Retiring at 60 with $300K looks very different depending on whether you’re doing it alone or with a partner.

Single person with $300K. The seven-year gap is the hardest part. Drawing $30,000 a year depletes super significantly before pension age. You’ll likely reach 67 with a modest balance and qualify for close to the full Age Pension. Combined with careful drawdown of remaining super, a modest retirement is achievable. A comfortable retirement on $300K alone as a single person is very difficult without other assets.

Couple with $300K combined. The household dynamic helps. Costs are shared, and the couple Age Pension rate ($47,070 a year combined) is much higher relative to per-person costs than the single rate. If both partners are frugal through the gap years, a couple with $300K combined can reach 67 in reasonable shape and have the pension carry most of the load from there.

Women face this scenario more often than men. The average female super balance at 60 to 64 ($313K) is right at the $300K mark, and women typically live longer than men, meaning the same balance needs to last longer. Scott and Phil covered this gap in detail in Episode 17 of the Wealthlab Podcast, including the additional twist that women often end up in more conservative super options despite needing the balance to stretch further. A high growth portfolio dropped 45% in the GFC but recovered within two years. The investment mix at 60 matters more than most people realise.

Home Ownership Changes Everything

This keeps coming up because it genuinely matters that much. A retiree who owns their home outright has already removed their single largest living cost from the equation. No rent, no mortgage. That alone can reduce annual spending needs by $20,000 to $30,000 or more depending on location.

A renter with $300K in super at 60 is in a very different position. Rent costs consume super quickly, there’s no asset building over time, and even though the Age Pension assets test threshold for non-homeowners is higher ($980,000 single / $1,343,000 couple), rent assistance only partly offsets the housing cost gap. If you’re renting and considering retirement at 60 with $300K, the numbers are genuinely difficult, and working a few more years usually makes a significant difference.

What a Modest Retirement at 60 With $300K Could Look Like

Here’s a practical scenario for a single homeowner.

Age 60 to 67 (the gap years)

- Super balance: $300,000

- Drawdown: $28,000 per year from super (account-based pension)

- Remaining balance at 67 (assuming 4% net return): approximately $110,000

Age 67 onwards

- Full Age Pension (approximate): $31,223 per year

- Super top-up drawdown: $5,000 to $8,000 per year

- Total income: approximately $36,000 to $39,000 per year

- Super balance at this drawdown rate could run through to approximately age 80 to 82

For a homeowner with no debt, $36,000 to $39,000 a year is not luxurious. But it covers groceries, utilities, basic health cover, a modest car, local activities and simple holidays. It is a modest but workable retirement.

In our experience, the people who make this work tend to share three things. They’ve already had a frank conversation about what they’re prepared to spend and what they’re not. They’ve stress-tested the plan against a 30 to 40 per cent market drop early in retirement (because sequence of returns risk is the killer at this balance level). And they’ve taken the time to actually understand how their super investment option behaves in different conditions, rather than leaving it on whatever default the fund stapled them to ten years ago.

What You Can Still Do Before Retiring

If you’re 60 and considering retirement but your balance feels light, a few strategies can make a meaningful difference even in a short window.

Work one or two more years. It sounds obvious but the impact is real. On the podcast, Phil and Scott looked at the difference one year of delayed retirement makes. The example: retiring one year earlier than planned shifted the funding position from running comfortably to age 105 down to running out at 79. The full breakdown is in Episode 19 of the Wealthlab Podcast. Each year you keep working adds employer contributions, potential salary sacrifice contributions, and one fewer year of drawdown on a balance that’s already tight.

Salary sacrifice through your final working years. If you’re still earning income, adding concessional contributions (the cap is $30,000 per year including employer contributions in 2025-26) at the 15% super tax rate instead of your marginal rate builds the balance and reduces your tax bill. Moneysmart’s guide to super contributions has a useful breakdown of how the mechanics work.

Catch-up contributions. If your total super balance is under $500,000 and you haven’t used your full concessional cap in recent years, you may be able to carry forward unused amounts and make larger contributions before you retire. This is worth checking with an adviser, because the eligibility rules around the $500,000 threshold can catch people out.

Consider part-time work rather than full retirement. Transitioning to three days a week, or taking on casual work for a year or two, keeps income coming in without the full grind of full-time employment. It also slows the drawdown on your super, which compounds significantly over a seven-year gap.

For more on structuring your retirement income strategy, see the Wealthlab retirement planning page.

What to Watch Out For

A few things that catch people out when retiring at 60 with a modest balance.

Healthcare costs rise with age. A healthy 60-year-old doesn’t spend much on healthcare. By 75, the picture looks different. Private health insurance, specialist appointments and medications all add up. Budget for this to increase over time rather than assuming today’s costs hold.

Inflation erodes purchasing power. $30,000 a year in 2026 buys less than $30,000 did in 2016. An account-based pension invested in a balanced or growth option helps offset this. A fully conservative portfolio often doesn’t keep pace with inflation over a 25-year retirement.

Sequence of returns risk. If markets fall sharply in the first few years of retirement and you’re drawing down at the same time, the balance can be damaged in ways that are hard to recover from. This is one of the most underappreciated risks at modest balances. Scott explained it well on the podcast: a portfolio with the same 6 per cent average return can fund retirement to your late 90s or run out 10 years earlier purely based on the sequence in which those returns arrive. That’s Episode 1 of the Wealthlab Podcast if you want the full walkthrough.

Investment mix at 60. Many super funds default you into a more conservative option as you approach retirement. Conservative portfolios have historically returned 3 to 4 per cent per year, versus 6 to 7 per cent for growth options. With $300K and potentially 25 to 30 years of retirement ahead, the investment choice you sit in at 60 can be worth tens of thousands of dollars over 20 years.

Frequently Asked Questions

Can I retire at 60 with $300K in super in Australia? It is possible for a homeowner targeting a modest lifestyle, particularly for a couple where costs are shared. The main challenge is funding the seven-year gap before the Age Pension starts at 67. With controlled spending and a moderate investment return, a single homeowner can reach 67 with remaining super and then partly rely on the Age Pension. A comfortable retirement on $300K alone, as defined by ASFA, is very difficult without other assets or part-time income.

How long will $300K in super last if I retire at 60? At $30,000 per year in spending with a 4% net return, $300K lasts approximately 13 to 15 years, taking you to around age 73 to 75 on super alone. The Age Pension from age 67 supplements this significantly if you’re eligible, which extends how long your money lasts in practice. Drawing less, or earning a higher net return through a less conservative investment option, can extend the timeline considerably.

Do I qualify for the Age Pension if I retire at 60 with $300K? Not immediately. The Age Pension is only available from age 67. From 60 to 67 you’ll be living off your super. By 67, if your super and other assets are modest, you’re likely to qualify for a full or part Age Pension. A single homeowner with $300K in super at 60 would likely qualify for a significant pension by 67, depending on how much super remains by then.

Is $300K enough to retire on in Australia? ASFA’s 2026 benchmark for a comfortable retirement is $630,000 for singles and $730,000 for couples. $300K falls below this but sits roughly at the median for Australians aged 60 to 64. Whether it’s “enough” depends on whether you own your home, whether you’re single or partnered, what lifestyle you’re targeting, and how the gap years to age 67 are managed. A modest retirement on $300K plus the Age Pension is achievable for many homeowners. A comfortable retirement at the ASFA standard generally isn’t, without working longer or having other assets.

What’s the difference between a comfortable and modest retirement in Australia? The current ASFA Retirement Standard (February 2026 update) puts a comfortable retirement for a single homeowner at approximately $54,240 per year and around $76,505 per year for a couple. A modest retirement is around $35,199 per year for a single person and $50,866 for a couple. The lump sums needed are approximately $630,000 single / $730,000 couple for comfortable, and around $110,000 single / $120,000 couple for modest (because the Age Pension covers most of the modest budget).

Is $300K in super enough for a couple to retire at 60? Combined, $300K is tight for a couple at 60. The seven-year gap before pension age is the hardest stretch. If both partners can work part-time through the early 60s, or one partner continues working, the picture improves considerably. A couple who reaches 67 with even $100,000 remaining and qualifies for the couple Age Pension ($47,070 per year combined) is in a workable position for a modest retirement.

What if I’m still renting at 60 with $300K in super? This is one of the harder retirement scenarios. Ongoing rent costs, which can easily run $20,000 to $30,000 per year, consume super quickly and make it very difficult to sustain a retirement over a 25 to 30 year horizon. Commonwealth Rent Assistance helps once the Age Pension starts at 67, but it only partly closes the gap. If you’re renting and considering retirement at 60 with $300K, working a few more years or talking to a financial adviser before making the call is generally a good idea.

Can I work part-time and still draw from super at 60? Yes. Once you’ve met a condition of release (typically retiring, even partially, or turning 60 and leaving an employer), you can access your super. Working part-time while drawing from super is a common transition strategy. Be aware that combined income affects your tax position and, eventually, your Age Pension eligibility once you turn 67.

Where to Get Help Thinking Through Your Numbers

Retiring at 60 with $300K is not impossible, but it isn’t comfortable either. The honest answer depends on a few key variables: whether you own your home, how much you plan to spend each year, whether you’re single or part of a couple, how well your super is invested through the gap years, and how willing you are to adjust if markets don’t co-operate in the early years.

For many Australians in this position, working two or three more years, or transitioning to part-time work rather than full retirement, makes a substantial difference. So does shifting from a conservative default option into something better matched to a 30-year retirement horizon.

If you’d like to talk through how the principles in this article apply to your situation, book a free chat with the Wealthlab team. No pressure, no jargon. Or take the free Wealthlab retirement quiz for a quick 60-second snapshot of where you stand.

Where to Get Help Thinking Through Your Numbers

Retiring at 60 with $300K is not impossible, but it isn’t comfortable either. The honest answer depends on a few key variables: whether you own your home, how much you plan to spend each year, whether you’re single or part of a couple, how well your super is invested through the gap years, and how willing you are to adjust if markets don’t co-operate in the early years.

For many Australians in this position, working two or three more years, or transitioning to part-time work rather than full retirement, makes a substantial difference. So does shifting from a conservative default option into something better matched to a 30-year retirement horizon.

If you’d like to talk through how the principles in this article apply to your situation, book a free chat with the Wealthlab