Yes, retiring at 60 with $425,000 in super is achievable for many Australians, particularly homeowners with modest to moderate spending expectations. It is not a large balance by ASFA’s comfortable benchmark, but it is enough to bridge the seven year gap to the Age Pension and, combined with pension income from 67, support a stable retirement for the rest of your life.

The catch is that $425K leaves less margin for error than higher balances. A poor investment mix, unplanned major expenses, or overspending in the early years can shift this from a workable retirement to a stressful one. This guide breaks down what $425K genuinely supports at 60, how long it lasts at different spending levels, and the strategies we generally see work at this balance.

Where $425K sits against the benchmarks

The ASFA Retirement Standard (lump sums updated February 2026) sets the recommended super balances at 67 at $630,000 for a comfortable single retirement and $730,000 for a couple. For a modest retirement, the recommended lump sums are much lower, around $110,000 single and $120,000 couple, because the Age Pension covers most of the spending at that level.

$425,000 sits well above the modest benchmark and $205,000 below the comfortable single target. As a couple with $425K combined, you are around $305,000 below the comfortable couple benchmark, which is a more significant gap.

For context, the average super balance for Australians aged 60 to 64 is approximately $381,000 for men and $301,000 for women, based on ASFA’s analysis of ATO data. With $425K, you are above the average for both singles and single women, and about $44,000 above the average for men. That puts you in a stronger position than most Australians approaching retirement.

The important point: those ASFA benchmarks assume you retire at 67, not 60. Retiring seven years earlier means your super has to fund those extra years before the Age Pension starts, so a balance that would comfortably support retirement at 67 needs more careful management at 60.

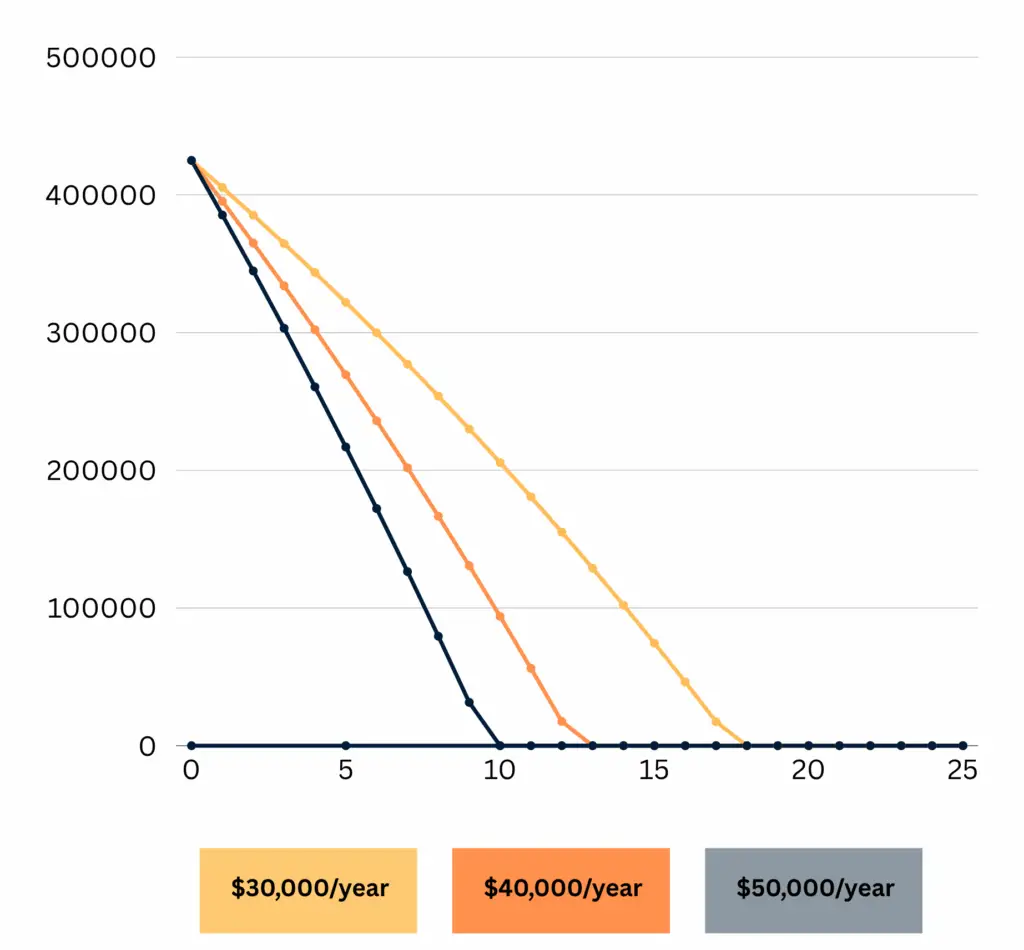

How long will $425K super last in retirement?

The answer depends almost entirely on how much you spend each year.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. They assume a balanced investment return of approximately 5% per annum after fees. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

| Annual spending | How long $425K lasts on its own | Age super runs out |

|---|---|---|

| $28,000/year | 20 to 24 years | Early to mid 80s |

| $35,000/year | 14 to 17 years | Mid to late 70s |

| $42,000/year | 11 to 13 years | Early 70s |

These figures assume you draw from super only, with no Age Pension until 67. Once the pension starts at 67, your required drawdown from super drops significantly, and the remaining balance stretches much further.

The pattern we generally see with $425K balances: spending in the $28,000 to $35,000 range through the gap years bridges you comfortably to 67 with a useful balance still invested. Spending above $40,000 in that period puts real pressure on the plan..

This Line Graph Shows How Long Will $425K Super Last?” across 3 spending levels ($30K, $40K, $50K).

The 60 to 67 gap: seven years your super has to cover

This is the stretch where a $425K retirement either works or falls short. From 60 you can access super tax-free, but the Age Pension does not start until 67. That is seven years where your super has to cover everything.

At $32,000 a year in spending, you would draw down roughly $220,000 over those seven years, allowing for some investment growth on the remaining balance. That leaves you with around $205,000 to $230,000 at 67. From that point, the Age Pension takes over as your primary income and your super becomes the top-up.

Scott and Phil walked through the real cost of the gap years in Episode 19 of the podcast. Their observation was that retiring even one year earlier can dramatically shift the numbers, with the average couple retiring today on around $540K combined and healthcare consuming approximately 34% of lifetime retirement spending. For a $425K balance, that framing is directly relevant.

How much Age Pension will you get with $425K at 67?

From 20 March 2026, the full Age Pension pays $1,200.90 per fortnight for singles ($31,223 a year) and $1,810.40 per fortnight for couples combined ($47,070 a year). A single homeowner with assessable assets under $321,500 qualifies for the full pension. For homeowner couples, the full pension threshold is $481,500 combined.

Source: Services Australia. These figures are set by the Australian Government and are updated each March and September.

Here is what that means at $425K specifically. If you arrive at 67 with around $220,000 remaining in super, a single homeowner would sit under the $321,500 full pension threshold and qualify for the full Age Pension of $31,223 a year. Combined with a modest drawdown from super, that produces a total retirement income of $37,000 to $40,000 a year, indexed with pension movements.

For a homeowner couple with $425K combined arriving at 67 with around $220,000 left, the couple assets test threshold of $481,500 also means the full couple Age Pension of $47,070 is likely, subject to the income test.

One of the structural advantages of retiring with a balance in this range is that the assets test tends to work in your favour by the time you reach 67. Phil and Dan covered how the assets test and income test interact in Episode 10 of the podcast, and Scott and Phil walked through commonly missed Age Pension opportunities in Episode 20.

Retiring single vs as a couple with $425K

$425K plays out very differently depending on whether it is a single balance or a couple’s combined balance.

For a single homeowner at 60, $425K is well above the individual average of $381,000 for men and $301,000 for women. It comfortably bridges the gap years at modest spending, and the single Age Pension of $31,223 becomes the primary income from 67. Many single retirees at this balance find that gap year spending of $30,000 to $32,000 works well.

For a couple with $425K combined, the picture is tighter. The couple ASFA comfortable benchmark is $730,000, so $425K sits $305,000 below that target. Combined spending of $40,000 to $45,000 in the gap years is generally more sustainable than higher figures at this balance. The offset is that the couple Age Pension of $47,070 a year is substantially higher than the single rate, so once both partners reach 67, the pension carries a bigger share of the load.

Scott and Phil discussed the specific challenges women face with super balances and retirement timing in Episode 17 of the podcast, covering the super gap, longer female life expectancy (average 85 vs 81 for men), and the investment mix mismatch many women face heading into retirement.

What’s the best way to invest $425K for retirement income?

The best way to invest $425K in retirement generally comes down to three principles: keep some growth in the portfolio, manage risk carefully through the gap years, and avoid decisions driven by short term fear.

Setting up an account-based pension is a common structure for retirees at 60. Rolling super into an account-based pension provides regular, tax-free income from 60, keeps the money invested, and helps control the drawdown rate. It is also generally more favourable under the Age Pension means test than lump sums held elsewhere. Our pension and Centrelink page covers this in more detail.

Keeping some growth assets in the mix matters more than most people expect at this balance. Scott and Phil showed in Episode 1 of the podcast how a growth portfolio expecting 6 to 7% per annum can fund a couple with $500K in super into their late 90s, while the same couple with a conservative portfolio at 3 to 4% runs out 15 years earlier. On $425K, that difference between growth and conservative is what determines whether the money makes it through a 25 to 30 year retirement.

Phil also pointed out in Episode 22 that what most super funds label “balanced” is often a growth portfolio with 70% or more in growth assets. It is worth checking what your fund calls balanced actually holds.

Holding one to two years of expenses in cash is a common way to manage sequencing risk. If markets drop 20% in the first year of retirement, drawing from cash rather than selling investments at a loss protects the long term balance. The cash buffer gets topped up when markets recover.

Diversified index funds or a well-managed balanced option inside super give broad market exposure without relying on individual stock picks. At $425K, the room for a concentrated bet that goes wrong is very small.

Want to run your own numbers? Try the free Wealthlab super calculator to see how your balance, spending and Age Pension interact.

How $425K plays out year by year

Here is an illustrative projection for a single homeowner spending $32,000 a year, with a balanced investment return of 5% per annum:

| Age | Super balance (approx.) | Drawdown from super | Age Pension | Total income |

|---|---|---|---|---|

| 60 | $425,000 | $32,000 | $0 | $32,000 |

| 63 | $335,000 | $32,000 | $0 | $32,000 |

| 67 | $220,000 | $6,000 | $31,000 | $37,000 |

| 72 | $195,000 | $6,000 | $31,000 | $37,000 |

| 80 | $145,000 | $6,000 | $31,000 | $37,000 |

| 85 | $115,000 | $6,000 | $31,000 | $37,000 |

These numbers are approximate and assume steady investment returns (real markets are lumpier). Actual drawdowns tend to rise with inflation over time, so the pattern here is illustrative. The key point is that from 67, the Age Pension takes over as the main income source and the pressure on your super drops significantly.

Six strategies that generally make $425K stretch further

Part-time work in the early years. Even $10,000 to $15,000 a year from casual or consulting work through the gap years takes real pressure off the super drawdown. Two to three years of light work at this balance often adds meaningful years to the plan.

Controlled spending through the gap years. The 60 to 67 window is where balances at this level are under the most pressure. Spending in the $30,000 to $35,000 range for singles, or $40,000 to $45,000 for couples, is where we generally see the plan hold together.

Planning for the Age Pension from day one. At $425K, the pension is not a small supplement, it is a core part of the plan. Structuring drawdowns and asset allocation with pension eligibility in mind tends to produce a better result than treating super and the pension as separate systems.

Healthcare cost planning. A healthy 60-year-old spends very little on healthcare. By 75, specialists, medications and procedures add up. Episode 19 noted that healthcare can consume around 34% of lifetime retirement spending, with the final 24 months of life alone accounting for 50 to 80% of total lifetime healthcare costs.

Age Pension application timing. Services Australia accepts applications up to 13 weeks before you turn 67. Getting the paperwork in early avoids missing weeks of payments while waiting for processing.

Rethinking downsizing carefully. For homeowners with $425K in super, downsizing is a common consideration, but the assets test treats the family home differently to cash. Scott and Phil covered the downsizer contribution rules in Episode 2 of the podcast, including the 90-day deadline and the Age Pension impact of turning an exempt asset (the home) into an assessable one (cash).

Retiring at 60 vs 65 with $425K

The five year difference between retiring at 60 and retiring at 65 is more significant than it looks on $425K.

Retiring at 60 means seven years of full self-funding before the Age Pension starts. Retiring at 65 cuts that to two years. That difference alone typically leaves $180,000 to $210,000 more in the account at 67, before accounting for five additional years of employer super guarantee contributions and compounding growth.

For someone at $425K at 60, working to 63 or 65 often shifts the retirement from workable to comfortable. This is not a recommendation to keep working, but a realistic option worth understanding. Our post on the average super balance at 60 explores this in more detail.

Retirement age in Australia: what actually matters

There is no compulsory retirement age in Australia. Three ages matter:

Preservation age (60): When you can access your super tax-free, provided you meet a condition of release. For anyone born after 1 July 1964, preservation age is 60.

Age Pension age (67): When you become eligible for the Age Pension, subject to means testing. Applies equally to men and women.

Your retirement age: Whenever the maths and lifestyle line up. On $425K, that is somewhere between 60 and 67 for most homeowners, depending on spending and other assets.

Scott and Phil covered the common myths around preservation age and retirement definitions in Episode 18 of the podcast, including the difference between preservation age and actual retirement, and how the “10 hours per week” test applies to conditions of release.

Frequently asked questions

Can I retire at 60 with $425K in Australia?

Yes, if you own your home and are prepared for a modest to moderate lifestyle. $425K can bridge the seven year gap to the Age Pension at 67 and, combined with the pension, support you into your mid to late 80s.

Is $425,000 in super enough to retire on?

For homeowners who budget carefully, yes. $425K is above the average super balance for Australians aged 60 to 64 and well above the ASFA modest benchmark. It falls short of the comfortable target ($630K for singles at February 2026), so lifestyle sits between modest and comfortable.

How long will $425K super last at 60?

At $32,000 a year with balanced investment returns, $425K on its own lasts 14 to 18 years. With the Age Pension from 67, total retirement funding extends into the mid to late 80s or beyond.

How much Age Pension will I get with $425K at 67?

If you draw around $30,000 a year from super between 60 and 67, you would likely arrive at 67 with around $200,000 to $230,000 remaining. For a single homeowner, that sits below the $321,500 full pension assets threshold at March 2026, which usually means the full Age Pension of $31,223 a year applies. Couples with $425K combined would be similarly placed under the $481,500 couple threshold.

What’s the best way to invest $425K in Australia for retirement?

For most retirees at this balance, an account-based pension with a balanced investment mix (around 60% growth, 40% defensive) is a common structure. It keeps the money invested, provides tax-free income from 60, and allows control over the drawdown rate. Holding one to two years of expenses in cash helps manage sequencing risk. Sitting fully in cash is generally avoided because it tends to lose real purchasing power across a 25 to 30 year retirement.

Can a couple retire at 60 with $425K combined?

It is tighter than at higher balances, but possible for homeowner couples with modest spending. Combined spending of $40,000 to $45,000 through the gap years, plus the full couple Age Pension of $47,070 from 67, generally supports a modest retirement lifestyle indefinitely.

How does renting affect retirement with $425K?

Renting adds $18,000 to $25,000 or more per year to retirement costs, which significantly compresses how far $425K stretches. The non-homeowner assets test threshold is higher ($579,500 for singles at March 2026), so renters may qualify for a larger part pension, but the ongoing rent cost typically outweighs that advantage. For renters at 60 with $425K, working a few more years or finding a way to reduce housing costs before retirement usually makes a material difference.

How much super should I have at 60 in Australia?

The ASFA target for a comfortable retirement at 67 is $630,000 for singles and $730,000 for couples (February 2026 figures). At 60, working backwards, that suggests $500,000 to $600,000 for a single person targeting a comfortable retirement. Most Australians retire with less than these targets, which is why the Age Pension is designed to supplement retirement income.

Your next step

$425,000 at 60 is a genuinely workable retirement position for homeowners, provided the gap years are managed carefully and the Age Pension is factored into the plan from day one. The margin for error is smaller than at $500K or $600K, but the fundamentals are the same: control the drawdown, keep some growth in the portfolio, and understand how everything shifts at 67.

If any of this has raised questions about your own situation, book a free chat with the Wealthlab team. No pressure, no jargon.

Not sure where you stand? Take the free Wealthlab retirement quiz for a general snapshot.