Retirement at 60 the dream of leaving the alarm clock behind, travelling when you want, and spending time on things that actually matter. But the big question remains:“Can I retire at 60 with $670K in Australia and still live comfortably?”The honest answer is yes, you can if you play your cards right.

With the right mix of investment strategy, lifestyle planning, and a few smart financial moves, $670K can take you far well into your 80s or even 90s without the constant worry of running out of money.

This guide walks you through what life with $670K in super can look like, how to make it last, and the strategies Australians are using to turn savings into freedom.

The Real Meaning of Retiring at 60 in Australia

For many Australians, hitting 60 means reaching a major milestone: you can finally access your super tax-free. But it’s also when financial reality hits.With rising living costs and longer lifespans, $670K isn’t “set for life” money but it’s strong foundation money if you plan carefully.

On average, Aussies now live about 85 years for men and 88 for women. That’s roughly 25–30 years of retirement to fund a whole new chapter that requires strategy, not just savings.

What Lifestyle Can $670K Support at 60?

If you’re retiring at 60 with $670K, you’re in a better position than most. According to ASFA, the average super balance for Australians in their early 60s is around $420K (men) and $360K (women) so you’re already ahead.

Here’s what a $670K balance can support if managed wisely:

- Comfortable living: All household bills, utilities, and groceries are easily covered.

- Healthcare security: Private health insurance, routine check-ups, and a buffer for emergencies.

- Freedom to move: Keep your car or use public transport without stressing about petrol or fares.

- Lifestyle perks: Enjoy dinners out, hobbies, and short domestic trips without guilt.

- Travel goals: Budget-friendly international travel every few years.

If you own your home and carry no major debts, your $670K can stretch far funding a comfortable lifestyle rather than just a basic one.

How Long Will $670K Last?

Let’s look at the numbers.

If you follow a 4–5% annual drawdown, your $670K could provide:

| Household Type | Estimated Annual Income | Tax Status | Longevity |

|---|---|---|---|

| Single retiree | $35,000–$40,000 | Tax-free after 60 | 25–30 years |

| Couple | $50,000–$55,000 | Tax-free after 60 | 25–30 years |

When you reach 67, you can combine your super with the Age Pension, giving you extra breathing room:

| Type | Age Pension (approx.) | Combined Income Potential |

|---|---|---|

| Single | ~$28,500 | $63,000–$68,000 |

| Couple | ~$43,000 | $93,000–$98,000 |

By combining these income sources, you gain flexibility to enjoy your retirement instead of merely enduring it.

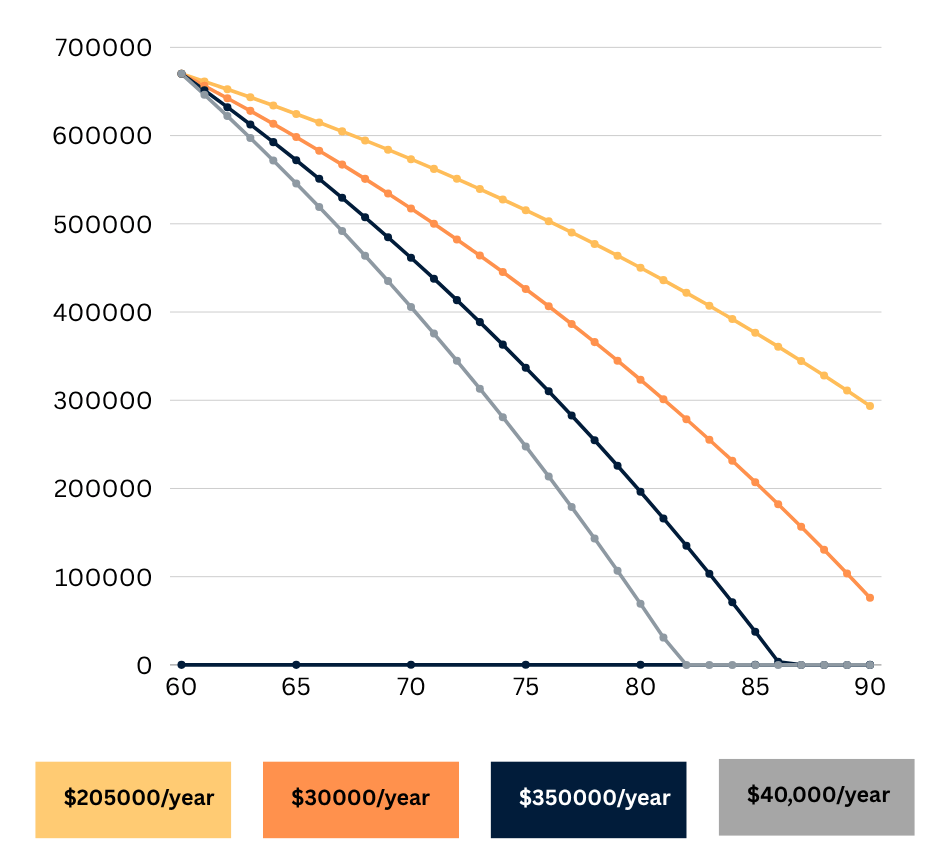

This Line Chart Shows Depletion of $670K over 30 years across spending levels: $25K, $30K, $35K, and $40K/year.

Sample Budget for a $30K–$35K Annual Lifestyle

To picture this lifestyle, here’s a realistic budget for a debt-free single or couple living modestly yet comfortably:

| Category | % of Budget | Annual Spend (approx.) |

|---|---|---|

| Food & Groceries | 22% | $7,000 |

| Utilities & Housing | 13% | $4,000 |

| Health & Medical | 15% | $4,500 |

| Transport | 12% | $3,600 |

| Leisure & Recreation | 10% | $3,000 |

| Insurance & Internet | 10% | $3,000 |

| Clothing & Essentials | 8% | $2,400 |

| Emergency / Savings | 10% | $3,000 |

That’s roughly $30K–$35K per year a sustainable and comfortable lifestyle without sacrificing your happiness or health.

5 Smart Strategies to Make $670K Work for You

Even a healthy super balance can disappear quickly without the right plan. Here’s how to make $670K work for you, not against you.

1. Invest for Growth, Not Guesswork

At 60, your strategy should shift from aggressive growth to stable, inflation-beating returns.

That means a mix of growth assets like shares, ETFs, or property exposure, plus defensive options like bonds and cash.

The goal? Protect your capital while letting it grow steadily.

Example: A 60/40 portfolio (60% growth, 40% defensive) often provides around 4–5% annual returns, enough to sustain comfortable withdrawals.

2. Budget Like a Pro (and Review Often)

The first few years of retirement are often the most expensive travel, home upgrades, lifestyle changes.

Track every dollar to ensure your spending aligns with your income. Small oversights early on can shave years off your savings.

Tip: Use apps like MoneyBrilliant or Frollo to keep your spending visible and accountable.

3. Create a Supplementary Income Stream

Many retirees find part-time work or side projects empowering, not limiting.

A few hours a week consulting, freelancing, or renting out a room can bring in $5K–$10K annually, easing the strain on your super and extending its life span.

4. Consider Downsizing or Relocating

Selling a larger home or relocating to a regional area can unlock extra capital and lower living costs.

You could even contribute up to $300K per person to your super under the government’s Downsizer Contribution Scheme.

Lower expenses mean more money for leisure and long-term comfort.

5. Ease into It with Phased Retirement

Who says you have to retire overnight?

Gradually reducing your hours or shifting to part-time before 60 lets you keep earning while adjusting to new rhythms.

This approach helps both emotionally and financially giving your super time to keep compounding.

Real-Life Example: Peter & Sandra’s Journey

Peter (60) and Sandra (59) have a combined $670K in super and own their home.They decide to retire graduallySandra drops to three days a week, while Peter consults part-time.

Their first 5 years look like this:

- Combined part-time income: $20,000/year

- Super drawdown: $45,000/year (tax-free)

- Age Pension from 67: $43,000/year

By combining these streams, they maintain an annual income of $65K–$85K, take one domestic holiday each year, and keep savings growing in the background.

Their secret? They planned early, kept spending realistic, and didn’t panic about market ups and downs.

FAQs: Can I Retire at 60 with $670K in Australia?

Q1: Is $670K enough to retire comfortably at 60?

Yes if you own your home, manage spending, and invest strategically. $670K can fund a comfortable lifestyle for 25–30 years when combined with the Age Pension later on.

Q2: How much income does $670K provide?

Roughly $35K–$40K per year for singles or $50K–$55K for couples, tax-free once you reach 60.

Q3: What’s the best investment strategy at 60?

A balanced approach part growth (shares, ETFs) for returns and part defensive (cash, bonds) for stability. Avoid taking unnecessary risks late in life.

Q4: Can I still travel or enjoy leisure activities?

Absolutely. With smart budgeting, you can travel domestically every year and even take an international trip every few years without jeopardising your nest egg.

Q5: Should I see a financial adviser?

Definitely. A certified adviser can help you structure withdrawals, reduce tax, and plan your investment mix based on your goals and comfort level. Retiring at 60 with $670K isn’t about giving up income it’s about gaining freedom.Freedom to choose how you spend your days, where you live, and what matters most.With the right mix of planning, investing, and budgeting, $670K can fund decades of financial peace and personal fulfilment.

The earlier you start preparing, the more flexibility and confidence you’ll have when the time comes to step away from full-time work.

Plan Your Future with Wealthlab

At Wealthlab, we help Australians build retirement strategies that work in the real world not just on paper.

Our advisors can show you exactly how to:

✅ Stretch your $670K further

✅ Balance risk and reward in your super

✅ Combine income streams for lasting comfort

👉 Book your free retirement planning session today and take the first confident step toward a stress-free retirement.