$750,000 in super at 60 is a strong position. It puts you above the ASFA Retirement Standard comfortable benchmark for singles ($630,000) and near it for couples ($730,000). The average super balance for Australians aged 60 to 64 is approximately $381,000 for men and $301,000 for women, so at $750K you’re roughly double the average.

The short answer is yes, you can retire comfortably at 60 with $750K if you own your home. You have enough to fund the seven-year gap to the Age Pension at 67, maintain a comfortable lifestyle, and still have a substantial balance remaining when pension support begins. The question at this level is not “can I retire?” but “how do I make the most of what I have?”

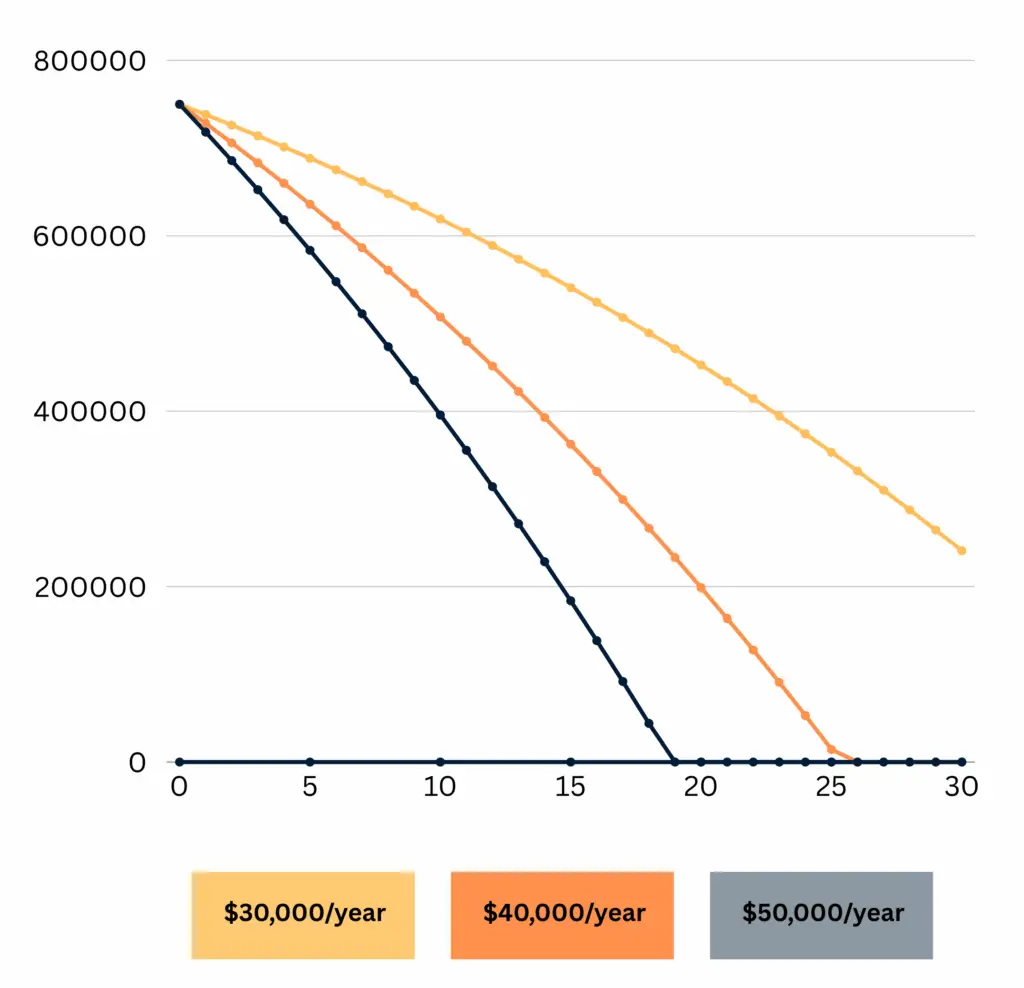

How long will $750K last in retirement?

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. They assume a balanced investment return of approximately 5% per annum after fees. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

| Annual spending | Balance at 67 | Balance at 75 | Balance at 85 |

|---|---|---|---|

| $40,000/year | ~$530,000 | ~$420,000 | ~$230,000 |

| $50,000/year | ~$440,000 | ~$270,000 | ~$30,000 |

| $60,000/year | ~$350,000 | ~$120,000 | Depleted ~82 |

| $70,000/year | ~$260,000 | Depleted ~76 | Gone |

At $45,000 to $50,000 a year, a single homeowner with $750K can comfortably fund the gap years, arrive at 67 with a substantial balance, and still have super lasting well into the mid-80s before the Age Pension takes over as the primary income source. For a couple spending $60,000 to $65,000, the picture is tighter but still workable, particularly once the couple Age Pension adds $47,070 a year from 67.

What $750K means against the benchmarks

The ASFA Retirement Standard (lump sums updated February 2026, spending figures updated quarterly) sets the comfortable retirement targets at $630,000 for singles and $730,000 for couples at age 67.

$750K at age 60 is above both singles targets and close to the couple target, seven years before the benchmark age. That’s a genuinely strong position. It means you can target the comfortable spending level of $54,840 a year for singles or $77,375 for couples from the start, rather than needing to live modestly in the gap years and ease up later.

The ASFA comfortable standard covers private health insurance, a reliable car, regular domestic travel and occasional overseas trips, dining out, and household costs. It is not luxury. It is a solid, secure retirement with genuine freedom of choice. At $750K, this lifestyle is within reach from day one.

Scott and Phil covered the real cost of the gap years in Episode 19 of the podcast. At $750K, the gap years are manageable. The risk shifts from “running out” to “not getting the structure right.”

This Line Chart Depletion of $750K across 30 years under $30K, $40K, and $50K spending levels.

The 60 to 67 gap on $750K

At $50,000 a year in spending with balanced returns, you arrive at 67 with approximately $440,000 in super. That’s above the full Age Pension threshold for a single homeowner ($321,500) but below the part pension cut-off ($722,000 at March 2026). You would receive a meaningful part pension.

For a couple with $750K combined, spending $60,000 a year brings you to 67 with roughly $350,000. That’s below the full couple pension threshold of $481,500, meaning you’d qualify for the full or near-full couple Age Pension of $47,070 a year (as of 20 March 2026).

Source: Services Australia. Updated each March and September.

From 67, the Age Pension supplements your super drawdown. Your remaining balance drops more slowly, and many retirees who start with $750K find their money lasting into the early to mid-90s on moderate spending.

Phil and Dan walked through real Age Pension case studies in Episode 10 of the podcast and covered commonly missed pension opportunities in Episode 20.

What lifestyle does $750K actually support?

At $50,000 to $55,000 a year for a single homeowner or $65,000 to $70,000 for a couple, $750K supports all household bills, groceries, utilities and insurance comfortably. Private health insurance is easily covered. A reliable car and regular maintenance are manageable. One or two domestic holidays a year, plus an occasional international trip every two to three years. Regular dining out, entertainment and social activities. Modest home maintenance and occasional upgrades.

This is the ASFA comfortable retirement in practice. It’s not extravagant, but it’s genuinely comfortable and secure. At $750K, you’re not counting every dollar. You’re making choices about how to spend, not whether you can afford to.

The best way to invest $750K in retirement

At $750K, the investment strategy matters more than at lower balances because you have more to protect and more time for compounding to work.

Account-based pension. Roll your super into an account-based pension. Tax on earnings drops to zero in pension phase (from 15% in accumulation). Your money keeps growing while you draw regular income. For more on how this works with the pension system, see our pension and Centrelink page.

Balanced to growth investment mix. With $750K and a 25 to 30 year retirement ahead, keeping 60 to 70% in growth assets (shares and property) and 30 to 40% in defensive (bonds and cash) gives you the best chance of outpacing inflation and making the money last. A conservative portfolio at 3 to 4% per year on $750K generates $22,500 to $30,000. A balanced portfolio at 5 to 6% generates $37,500 to $45,000. Over 25 years, that difference is hundreds of thousands of dollars. Scott and Phil showed in Episode 1 of the podcast how a conservative portfolio can run out 15 years earlier than a growth one. Phil also noted in Episode 22 that what most funds call “balanced” is really a growth portfolio, so check what you’re actually invested in.

Cash buffer of two years’ expenses. At $750K and $50,000 spending, that’s $100,000 in cash or near-cash. This protects against sequencing risk: if markets drop in year one, you draw from cash instead of selling investments at a loss. Top up the buffer when markets recover.

Don’t over-concentrate. $750K gives you the temptation to make larger bets, like putting a significant portion into a single property or concentrated share portfolio. Diversification is still the best protection. A well-managed balanced option inside your super fund or a diversified ETF portfolio keeps risk appropriate.

For more on superannuation investment options, see our service page.

What you can still do to strengthen the position

Even at $750K, a few moves can meaningfully improve the outcome.

Maximise contributions in the final working years. The concessional cap is $30,000 for 2025-26, rising to $32,500 from 1 July 2026. If your balance is under $500K (it’s not, at $750K), carry-forward rules apply. But you can still salary sacrifice up to the annual cap on top of employer contributions.

Consider the downsizer contribution. If you’re 55 or over and sell a home you’ve owned for 10+ years, you can contribute up to $300,000 each ($600,000 as a couple) into super from the proceeds, outside the normal caps. This is relevant if you’re thinking about downsizing. Scott and Phil covered the traps in Episode 2 of the podcast.

Get your estate planning right. At $750K, there’s meaningful wealth to protect and pass on. Super death benefits are treated differently depending on who receives them. Binding nominations and estate planning matter at this balance level. Scott and Phil covered the key traps in Episode 12.

For more on structuring your retirement planning, see our service page.

Want to run your own numbers? Try the free Wealthlab super calculator. For a broader readiness check, take the retirement quiz.

Frequently asked questions

Can I retire at 60 with $750K in Australia?

Yes, comfortably. $750K is above the ASFA comfortable benchmark for singles ($630,000) and near it for couples ($730,000). A homeowner at 60 can fund the seven-year gap to the Age Pension, maintain a comfortable lifestyle, and still have a substantial balance at 67.

How long will $750K last in retirement?

At $50,000 a year with balanced returns, $750K lasts well into the late 80s before the Age Pension takes over as the primary income source. At $40,000 a year, it can last into the 90s. At $70,000 a year, it runs out in the mid-70s, though the Age Pension extends the overall timeline.

Is $750K enough to retire comfortably?

Yes, for homeowners. ASFA defines a comfortable retirement as $54,840 a year for singles and $77,375 for couples. $750K can sustain spending at or near these levels, particularly once the Age Pension supplements your income from 67.

How much Age Pension will I get with $750K at 67?

Depends on how much you’ve drawn down by 67. If you arrive at 67 with $440,000 (after 7 years at $50K/year), you’re above the full pension threshold but below the cut-off. You’d receive a part pension. If your spending is higher and you arrive with $300,000 to $350,000, the pension entitlement is larger. A couple arriving at 67 with assets under $481,500 qualifies for the full couple pension of $47,070 a year (March 2026).

What’s the best investment strategy for $750K in retirement?

A balanced to growth mix (60-70% growth, 30-40% defensive) in an account-based pension, with a two-year cash buffer for sequencing risk protection. Avoid concentrating in a single asset class. The difference between 5% and 3% returns over 25 years on $750K is hundreds of thousands of dollars.

Should I retire at 60 or keep working with $750K?

At $750K, the financial case for retirement at 60 is strong. The decision becomes more personal than financial: do you have a clear vision for what you’ll do with your time? Are your relationships and identity ready for the transition? For more on the personal side, see our guide on when is the best time to retire.

How does $750K compare to what most Australians retire with?

The average super for Australians aged 60-64 is approximately $381,000 for men and $301,000 for women. At $750K, you’re roughly double the average. You’re in a stronger position than the majority of Australians approaching retirement.

Is $750K enough for a couple to retire at 60?

Yes. $750K combined is near the ASFA comfortable couple benchmark of $730,000. A homeowning couple spending $60,000 to $65,000 a year can fund the gap years and arrive at 67 eligible for a meaningful Age Pension. Combined income from 67 (super drawdown plus pension) can reach $60,000 to $70,000, which is within the ASFA comfortable range.

Making the most of $750K

$750,000 at 60 is one of the stronger starting positions for retirement in Australia. The question isn’t whether you can retire. It’s how to structure things so the money works as hard as possible across a 25 to 30 year horizon. Investment mix, drawdown timing, Age Pension structuring and estate planning all matter more at this balance than at lower amounts, because there’s more to optimise and more to protect.

If any of this has raised questions about your own situation, book a free chat with the Wealthlab team. No pressure, no jargon.