C O M P O U N D I N G · E X P L A I N E D P R O P E R L Y

Time beats a bigger wallet. Every single time.

Ella’s parents tipped $30,000 into her super and stopped after ten years. Liam putin $81,000 and never stopped. Guess who retired richer.

Same 7% return. Same finish line at 65. Ella invested 37% of Liam’s money and still won by $39,052.

There is a particular kind of gift that your kids and grandkids will not unwrap, will not photograph, and will not thank you for at the time. They might not even notice it for thirty years. And then one quiet Tuesday in their sixties, they will look at a balance on a screen and realise you handed them a small fortune while they were busy getting on with their lives.

That gift is a contribution to their superannuation, and the engine that makes it ridiculous is compounding.

Most people nod along when you say, “compound interest is powerful.” They have heard it. They believe it the way they believe flossing is good for them. What they have almost never done is sit with the actual numbers long enough to feel the vertigo. So let us do that.

By the end of this article you will understand exactly why the person who invests less can finish with more, you will have a back-of-the-envelope trick that makes you look clever at dinner parties, and you will know the one thing about super that most Australians completely miss.

Fair warning: you cannot un-know this stuff.

0 1 / T H E P A R A D O X

Meet Ella, who quit early, and Liam, who tried harder

Ella is 28, a few years into her working life, with a super account she rarely thinks about. Her parents decide that rather than another present she does not really need, they will tip $3,000 a year into her super. They do this for ten years, from 28 to 37, then they stop entirely. Total gifted: $30,000. After that, Ella never adds another cent of her own to this particular pile. She just leaves it alone.

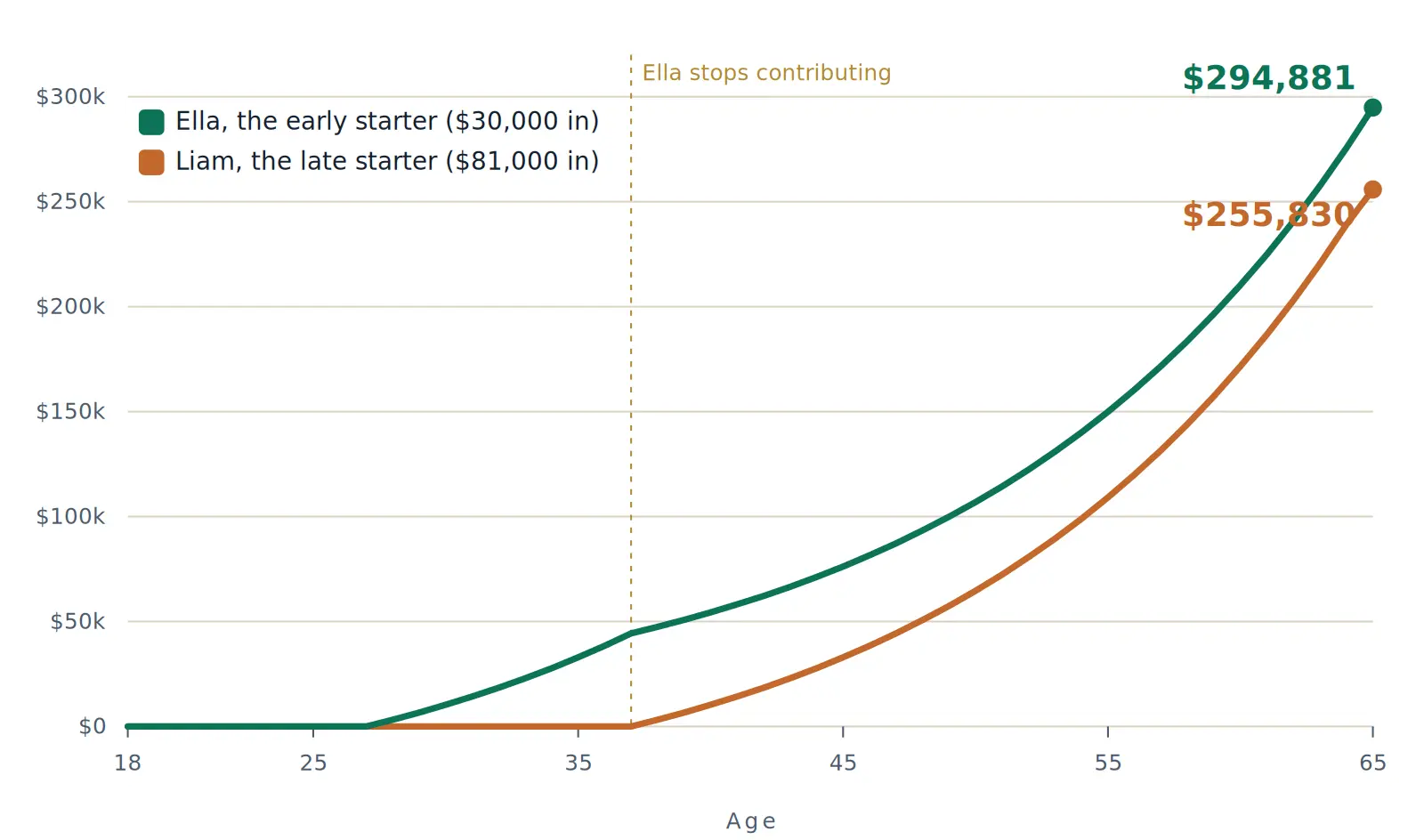

Liam hears about this at 38 and thinks, smart idea, I will do the same, except I will keep going. So Liam contributes $3,000 every year from 38 all the way to 64. That is 27 years of discipline. Total contributed: $81,000, almost three times what Ella ever put in. Both earn the same steady 7% a year. Both stop the clock at 65. Here is what their balances do over the journey.

Ella (green) front-loads ten years of contributions then coasts. Liam (clay) out-contributes her almost three to one across 27 years and still does not catch the line. Assumes a flat 7%return for illustration only.

Read that chart again, because it is doing something your intuition swears is impossible. The green line stops being fed at age 37. From there it is pure coasting, no new money, just growth on growth. The clay line keeps getting fresh fuel year after year after year, and it spends the entire chart trying to claw back the head start. It never does. Ella finishes on $294,881. Liam finishes on $255,830. She is ahead by $39,052, having parted with 37 cents for every dollar Liam invested.

The lesson is not “Liam is a chump.” Liam did well, he turned $81,000 into $255,830. The lesson is that Ella’s first ten years had something Liam could never buy back: time at the front. Every dollar Ella put in at 28 had 37 years to multiply. Liam’s dollars started a decade later and never clawed the gap back. Money invested early is not worth a little more than money invested late. It is worth wildly, almost offensively more.

0 2 / T H E B L I N D S P O T

Why your brain flatly refuses to believe this

Here is the uncomfortable truth: humans are linear thinkers trapped in an exponential world. Our brains evolved to estimate things that add up, not things that multiply. A pile of grain that grows by ten bushels a year is easy to picture. A pile that grows by 7% of itself every year, forever, is not. We badly underestimate it, every time.

The classic demonstration is the old legend of the inventor who showed a king a new game played on a board of 64 squares. Delighted, the king offered any reward. The inventor asked only for rice: one grain on the first square, two on the second, four on the third, doubling all the way to the 64th. The king laughed at such a modest request, right up until his treasurer worked out it came to more rice than had ever existed on Earth, roughly 18 quintillion grains. Same trick, every time. Doubling feels gentle for ages, then it goes vertical and leaves your imagination behind.

MYTH-BUSTER, SO YOU SOUND SMART

Einstein never called compounding the eighth wonder of the world

You will see that line on a thousand finance posts, usually with a sepia photo of Albert. There is no evidence he ever said it. The quote was being attributed to various people decades before it was ever pinned on Einstein, and historians have never found it in anything he wrote or spoke. Drop that at the next barbecue and watch a financial adviser flinch.

The maths, happily, does not need a celebrity endorsement. It works whether or not a genius signed off on it.

0 3 / T H E S H A P E

The hockey stick, and where the money actually shows up

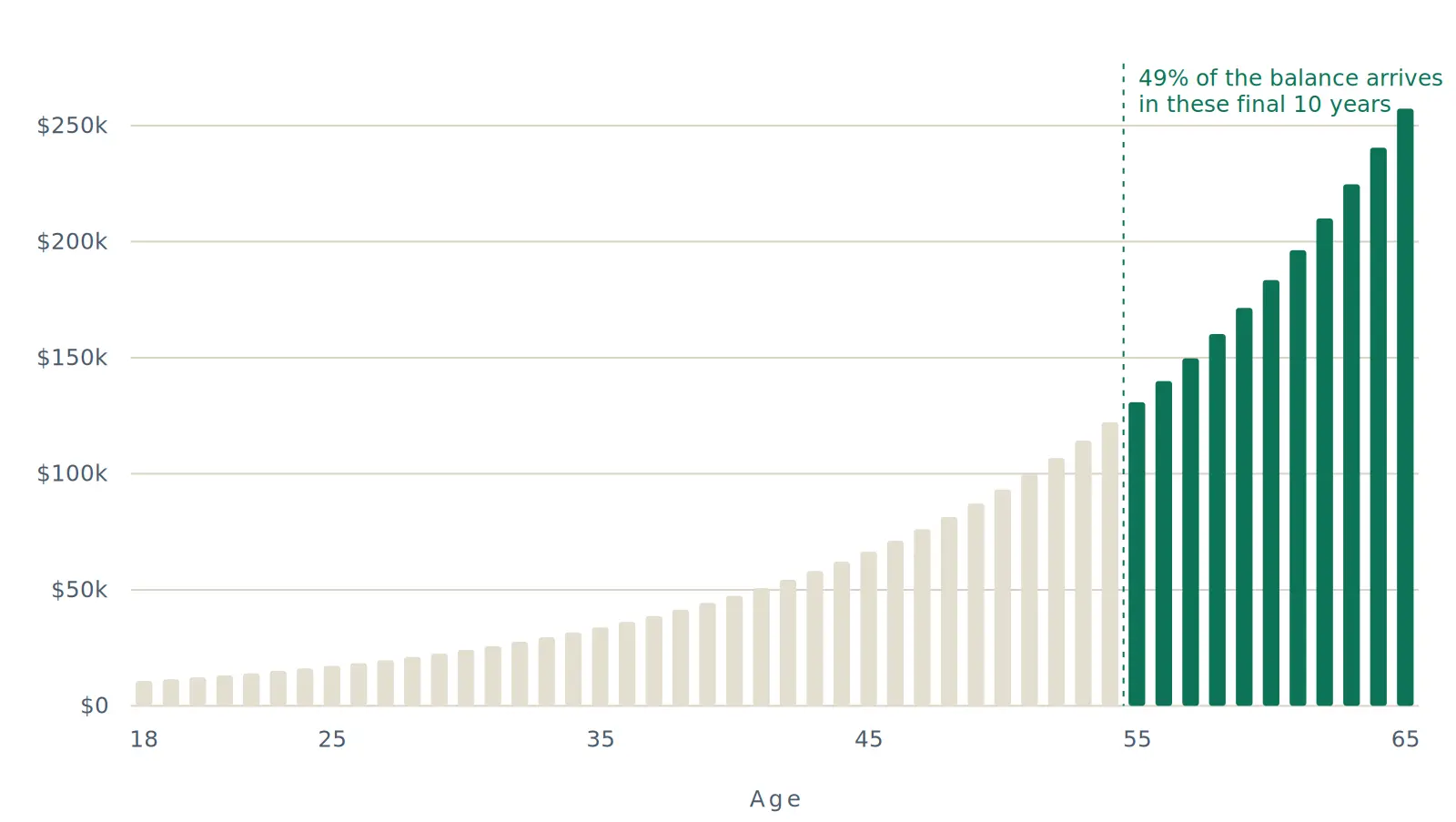

If you take a single $10,000 gift, drop it into a 7% investment at age 18, and never touch it again, it becomes $257,289 by 65. From ten grand. But the more interesting story is not the final number, it is when the growth turns up. Watch the bars.

Each bar is the balance at that age, growing from a single $10,000 gift. For decades it looks almost flat, then it detonates. Roughly 49% of the final balance is created in the last ten years alone.

This is the part that breaks people. For the first thirty-odd years it barely looks like anything is happening. The bars creep up so gently you would be forgiven for thinking the strategy is broken. Then somewhere in the fifties it goes berserk. About 49% of the entire final balance is manufactured in just the last decade, on money that was contributed back when the kid was a teenager. The work was done early. The fireworks happen late. That gap between effort and reward is exactly why so few people start: the payoff is so far away that the early years feel pointless. They are the opposite of pointless. They are the only part that matters.

A GENUINE GIFT THAT KEPT ON GIVING

Benjamin Franklin’s 200-year experiment

In a codicil to his will in 1789, Franklin left 1,000 pounds each to the cities of Boston and Philadelphia, worth around four thousand dollars at the time. The catch: the money had to be lent out at interest and left largely untouched for 200 years. He was, in effect, betting on compounding outliving everyone who would ever read the will.

By 1990, when the two centuries were up, Boston’s fund had grown to roughly $4,500,000 and Philadelphia’s to about $2,000,000. A few thousand dollars, left alone and allowed to multiply, funded technical schools and scholarships for generations. Franklin understood the assignment two hundred years before the rest of us.

THE WARREN BUFFETT TWIST

The richest investor alive is really a story about patience

Writer Morgan Housel ran the numbers in The Psychology of Money and found something startling. Of Warren Buffett’s roughly $84,500,000,000 net worth at the time, about $81,500,000,000 of it arrived after his 65th birthday. Over 99% came after he turned 50.

Buffett is a phenomenal investor, no argument. But the secret weapon was never just stock picking. It was that he started investing as a child and simply never stopped, giving compounding three-quarters of a century to do its thing.

As Housel puts it, his skill is investing, but his real edge is time. Had he started in his thirties and retired at 65 like a normal person, you would never have heard of him.

0 4 / Y O U R P A R T Y T R I C K

The Rule of 72, the only mental maths you need

Want to estimate how long it takes money to double, without a spreadsheet? Divide 72 by your return. At 7% a year, 72 divided by 7 is about 10.3, so your money doubles roughly every ten years. This little shortcut is not new. It shows up in Luca Pacioli’s Summa de Arithmetica, published in Venice in 1494, the same book that first laid out double-entry bookkeeping. Renaissance merchants were doing this in their heads five centuries ago.

Now apply it to Ella. From 28 to 65 is 37 years. At one doubling every ten years, that is about three and a half doublings. Start with a dollar, double it three and a half times, and you land around 12 times your money. Which is why a single dollar invested at 28 becomes about 12 dollars by 65, and why her ten years of $3,000 contributions snowballed into $294,881. Once you can double in your head, you can feel the power of an extra decade instantly. Each decade you wait does not shave a slice off the result. It roughly halves it.

0 5 / T H E P R I C E O F ” L A T E R “

What waiting actually costs

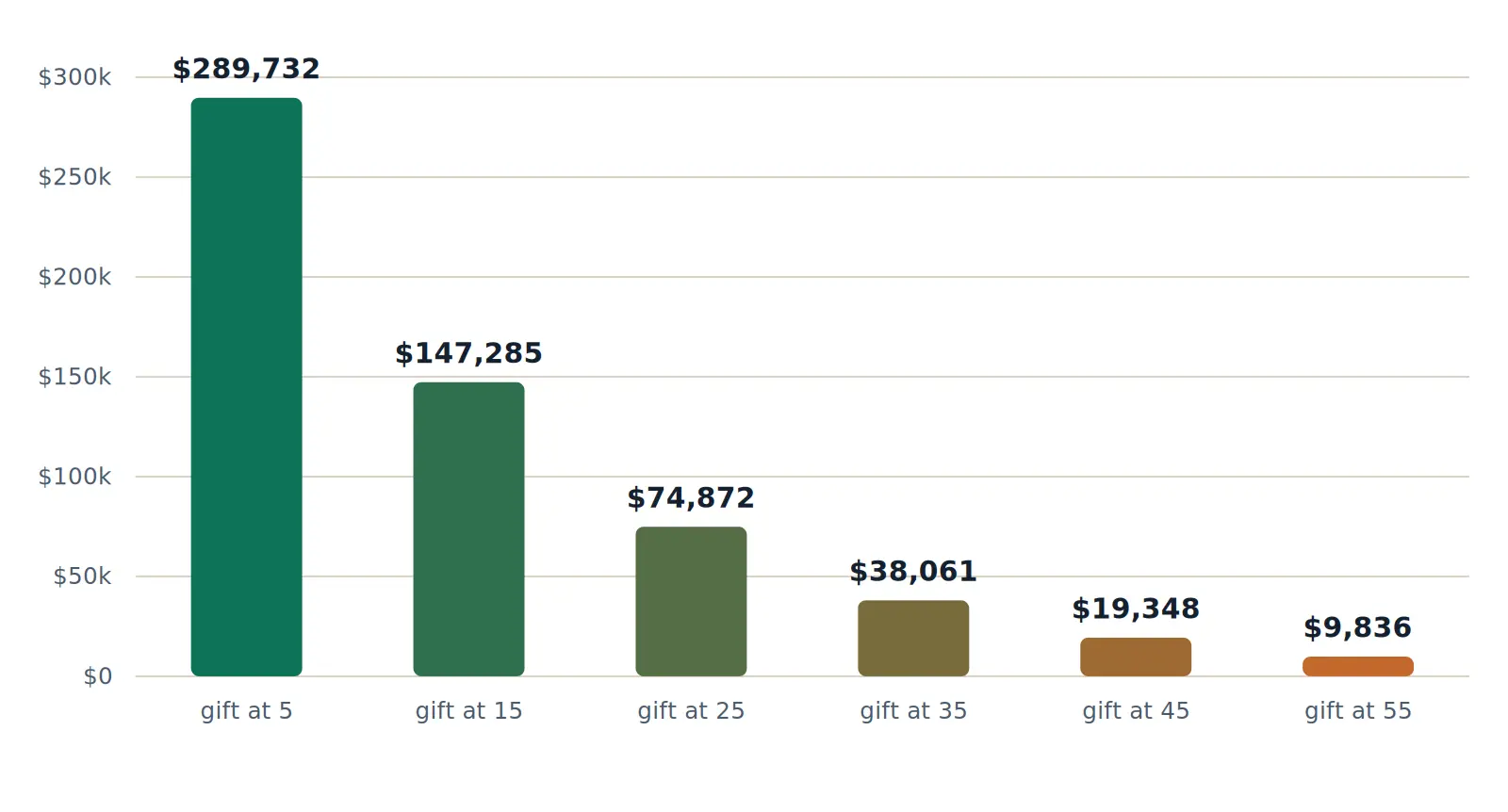

“We will start when they are older and we have more spare cash” is the most expensive sentence in personal finance. Here is the same $5,000 gift, made once, at different ages, all left to grow at 7% until 65.

Identical gift, identical return, only the start date changes. Notice the result roughly halves for every decade of delay, the Rule of 72 showing up in real life.

Gift $5,000 to a five-year-old and it is worth $289,732 at 65. Wait until they are 25 and the same $5,000 manages only $74,872. Hold off until 45 and you are down to $19,348. Same money. Same fund. The only variable is how many doublings you gave it. Procrastination, in compounding terms, is not neutral. It is a tax you pay for the privilege of waiting.

The best time to plant a tree was twenty years ago. The second best time is today, and your grandkids will be sitting in its shade long after you have forgotten you planted it.

An old proverb, lightly borrowed for super

0 6 / T H E A U S T R A L I A N A N G L E

Why super, specifically, and not just any investment

You might be thinking, fine, but why bury it in super where they cannot reach it for decades? That lock is not a bug. It is the whole point, and it comes with two quiet advantages that an ordinary savings account or share portfolio cannot match.

First, the tax environment. Inside super, investment earnings are taxed at a maximum of 15%, and in the retirement pension phase the rate can fall to zero. Outside super, earnings are taxed at the individual’s marginal rate, which for a working adult can be far higher. Over 40-plus years of compounding, that difference in the tax drag is not a rounding error. It is the difference between a snowball rolling downhill and one rolling through mud.

Second, it cannot be raided. A gift of cash to a 19-year-old has a way of becoming a car, a festival ticket, or a very memorable weekend. A contribution to super is preserved, meaning it stays locked until they reach preservation age and meet a condition of release. That enforced patience is precisely what lets compounding run uninterrupted, which, as the late Charlie Munger liked to point out, is the firstrule ofthe whole game: never interruptit unnecessarily

07 / THE PRACTICAL BIT

How to actually do this, and the catches worth knowing

You can generally contribute to another person’s super fund as a third party. For a child or grandchild this is treated as a non-concessional contribution, meaning it is made from after-tax money and the person giving it does not claim a tax deduction. It is genuinely that simple to set up. But a few catches are worth flagging before you start writing cheques.

Watch the contribution caps

Non-concessional contributions are capped each year, and anything you tip in counts toward the receiver’s cap, not yours. The caps are indexed and change over time, so check the current limits before making a large contribution,especially if the young person is already receiving employer super or contributing themselves.

Mind the fees eating a small balance

A teenager’s super account is often tiny, and a small balance is unusually vulnerable to flat-dollar admin fees and, in some cases, default insurance premiums that quietly chew through returns. On a $50 balance, a $100 annual insurance premium is not a fee, it is a demolition. It is worth checking what is being deducted and whether any insurance cover is actually needed at that age.

Remember they cannot touch it

This is a feature, but it is also a commitment. The money is genuinely locked away for decades. If there is any chance the young person will need help with a house deposit or education in the nearer term, super is the wrong vehicle for that particular pot. Compounding rewards money you can afford to forget about.

08 / THE SENSITIVITY

$1,000 today, and why the return assumption matters

One last thing to make you dangerous at dinner. A single $1,000 gift to a 20-year-old, left in super until 65, lands very differently depending on the return it earns. This is not a forecast, returns are never smooth and never guaranteed, but it shows why the rate you earn over decades matters enormously.

| IF IT EARNS | $1,000 AT 20 BECOMES, BY 65 |

|---|---|

| 5% a year | $8,985 |

| 6% a year | $13,765 |

| 7% a year | $21,002 |

| 8% a year | $31,920 |

| 9% a year | $48,327 |

Same $1,000, same 45 years. The only difference is the annual return.

Two extra percentage points of return, from 7% to 9%, more than doubles the final result. That is compounding compounding on itself. It is also a reminder that the boring decisions, low fees, a sensible investment option, staying invested through the scary years, are the ones that quietly decide the outcome.

What you now know that most people do not

- Time outranks money. Ella investd 37% of what Liam did and still finished ahead. <brThe early years are the expensive ones to skip.

- The payoff lands late. Around 49% of a balance can appear in the final decade, on money contributed when the person was a teenager.

- Use the Rule of 72. Divide 72 by your return to find the doubling time. At 7%, money doubles roughly every ten years.

- Waiting halves it. Each decade of delay roughly halves the end result. "Later"is the most expensive word in investing

- Super is the cheat code. A 15% maximum earnings tax and a lock that stops the money being spentlet compounding run clean for decades.

- Einstein never said it, Franklin actually did it, and Buffett is living proof that the secret was patience all along.

Thinking about a gift that outlives the wrapping paper?

Whether it is for your own retirement or a head start for the next generation, the right structure and the right timing are worth getting clear on. Have a chat with the Wealthlab team about how this could fit your situation.