By Scott and Phil, Financial Planners at Wealthlab

Managing your cashflow and debt effectively is a critical component of financial planning. At WealthLab, we’re always on the lookout for innovative approaches to help our clients achieve financial freedom. One such approach that we’ve found particularly effective is the Debt Waterfall Strategy. In this comprehensive guide, we’ll dive deep into the mechanics of this strategy, explore its advantages and potential drawbacks, and break down the mathematics that make it so powerful.

What is the Debt Waterfall Strategy?

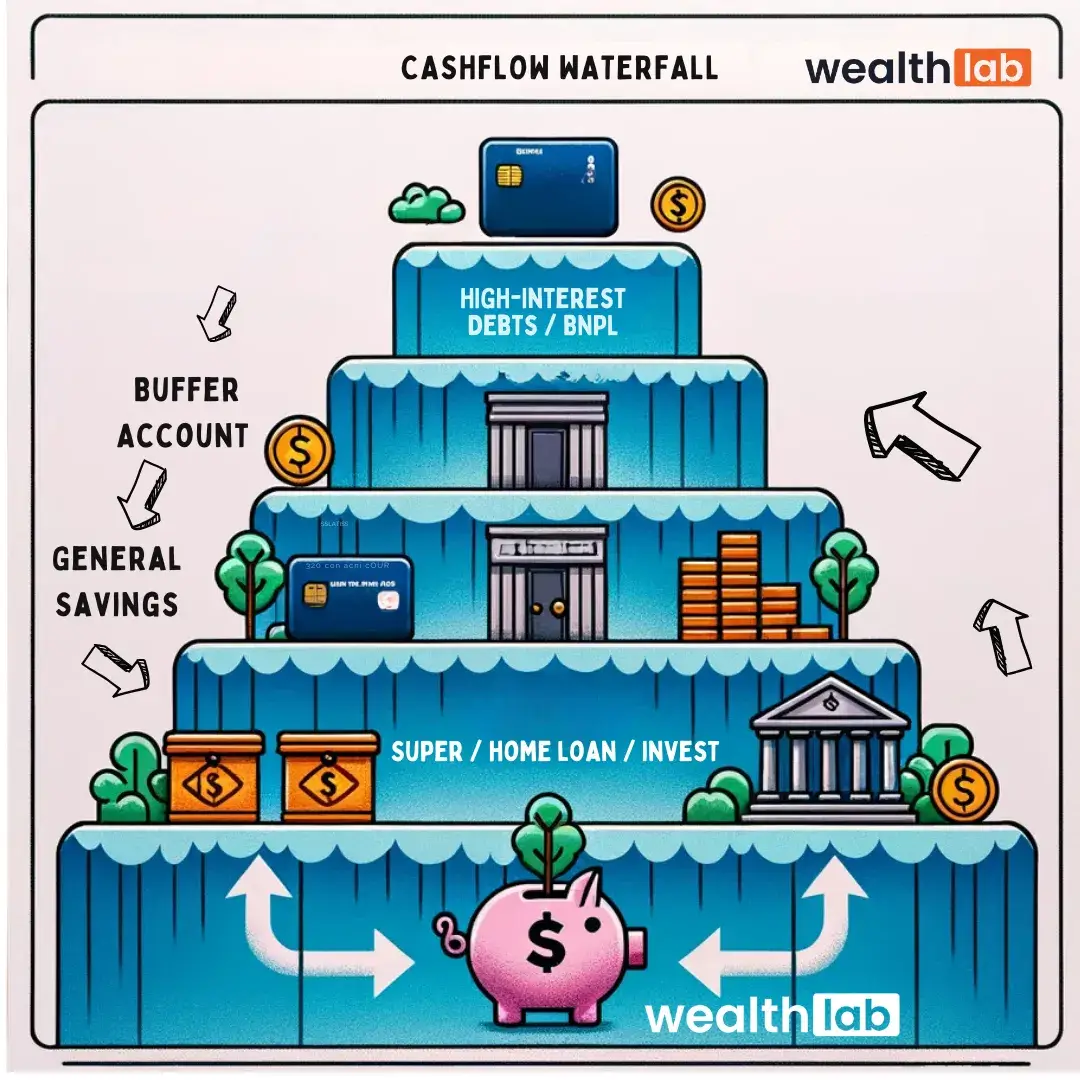

The Debt Waterfall Strategy is a methodical approach to managing and paying off debt. It involves prioritising debts based on their interest rates, starting with the highest. The strategy gets its name from the cascading effect of payments as you pay off each debt.

What is the Waterfall Strategy?

How Does it Work?

- List All Debts: Begin by listing out all your debts, from the highest interest rate to the lowest.

- Minimum Payments: Ensure minimum payments are made on all debts to avoid penalties.

- Extra Payments: Direct any extra funds towards the debt with the highest interest rate.

- Cascading Effect: Once the highest interest debt is cleared, redirect these funds to the debt with the next highest interest rate.

- Repeat: Continue this process until all debts are paid off.

Benefits of the Debt Waterfall Strategy

- Cost-Effective: By targeting high-interest debts first, you reduce the overall interest paid over time.

- Momentum Building: There’s a psychological benefit in seeing debts being cleared, which can motivate continued adherence to the plan.

- Structured Approach: It provides a clear and organised method for tackling debt.

The Marathon Analogy

Implementing the Debt Waterfall Strategy is much like running a marathon. As the saying goes, “Investing is like a marathon, not a sprint.” The same principle applies to debt repayment. It requires patience, persistence, and a long-term perspective. Just as a marathon runner paces themselves for the long haul, you need to adopt a disciplined approach to your debt repayment journey.Like training for a marathon, the Debt Waterfall Strategy requires preparation, consistent effort, and the ability to overcome obstacles along the way. There may be times when you feel like giving up, but remember that each debt you pay off is like passing another mile marker – it brings you closer to your ultimate goal of financial freedom.

Potential Challenges

- Requires Discipline: This strategy demands a strict adherence to the plan.

- Liquidity Issues: Allocating extra funds to debt reduction can reduce available cash for emergencies.

- Not One-Size-Fits-All: It might not be suitable for all financial situations, especially where lower interest debts have higher personal significance or urgency.

The Mathematics Behind the Strategy

The effectiveness of the Debt Waterfall Strategy lies in its mathematical foundation. Here’s a simplified example to illustrate:

- Debt A: $10,000 at 20% interest

- Debt B: $5,000 at 10% interest

- Monthly Payment: $500 towards Debt A, $200 towards Debt B (minimum payments)

By focusing on Debt A first, the high-interest rate is tackled head-on, reducing the amount of interest accrued over time. Once Debt A is cleared, the $500 that was being paid towards it is then directed to Debt B, on top of its $200 minimum payment. This accelerates the repayment of Debt B, further reducing the interest paid.

Adapting the Strategy for Non-Debt Holders

For those fortunate enough not to have debt, a modified version of the Debt Waterfall Strategy can be applied to enhance financial stability and growth:

- Buffer Account: Initially, direct your surplus income into a buffer account. Aim for an amount equivalent to three months’ worth of expenses.

- Fun Account: Once the buffer is established, start contributing to a ‘fun account’, equivalent to one month’s expenses.

- Investing and Wealth Creation: With the buffer and fun accounts in place, shift your focus to investing and wealth creation.

This adapted strategy not only secures your immediate financial needs but also ensures that you’re building towards a prosperous future while enjoying life along the way.

So in summary…

The Waterfall Strategy is a powerful tool for managing and eliminating debt. By understanding its mechanics and the discipline required, it can be an effective part of your financial planning arsenal. However, it’s essential to consider your unique financial circumstances and seek professional advice when needed.

Remember, you can always reach out to us at WealthLab for personalised advice. Also, don’t miss our detailed discussion on this topic in our WealthLab Podcast, which can provide you with more insights and practical tips.

Listen to Our Podcast on the Debt Waterfall Strategy

Disclaimer: This post is for educational purposes only and should not be taken as financial advice. Always consult a professional for financial planning (such as us!) about investment decisions.