At $250K, this is the lowest balance in our series, and it deserves the most direct answer. A fully self-funded retirement from 60 to 90 is not realistic at this balance for most Australians. The super is not large enough to carry that load on its own over 30 years.

But that framing misses how retirement at $250K actually works for people who make it function. It is not a 30-year self-funded plan. It is a seven-year bridge from 60 to 67, managed carefully, with the Age Pension taking over as the primary income source from there. Super then becomes the supplement. For homeowners with genuinely low spending needs, and particularly those willing to do some paid work in the early years, that plan can work.

This post lays out the realistic picture, what the risks are, and what distinguishes the retirements that hold together from those that do not.

Where $250K Sits Against the Retirement Benchmarks

The ASFA Retirement Standard estimates a single homeowner needs around $595,000 in super (plus the Age Pension) for a comfortable retirement, and a couple needs around $690,000. (Source: ASFA)

At $250K, a single retiree is around $345,000 below the comfortable benchmark. The relevant comparison is the ASFA modest retirement standard, which describes a lifestyle covering basic essentials for a homeowner relying primarily on the full Age Pension. That standard requires a relatively low super balance precisely because the Age Pension is doing most of the income work from 67.

The honest position is that $250K at 60 is most viable as a bridge to that Age Pension-supported retirement. How well the bridge holds depends on spending discipline during the 60 to 67 window and whether some supplementary income reduces the annual drawdown.

The 60 to 67 Bridge: The Critical Seven Years

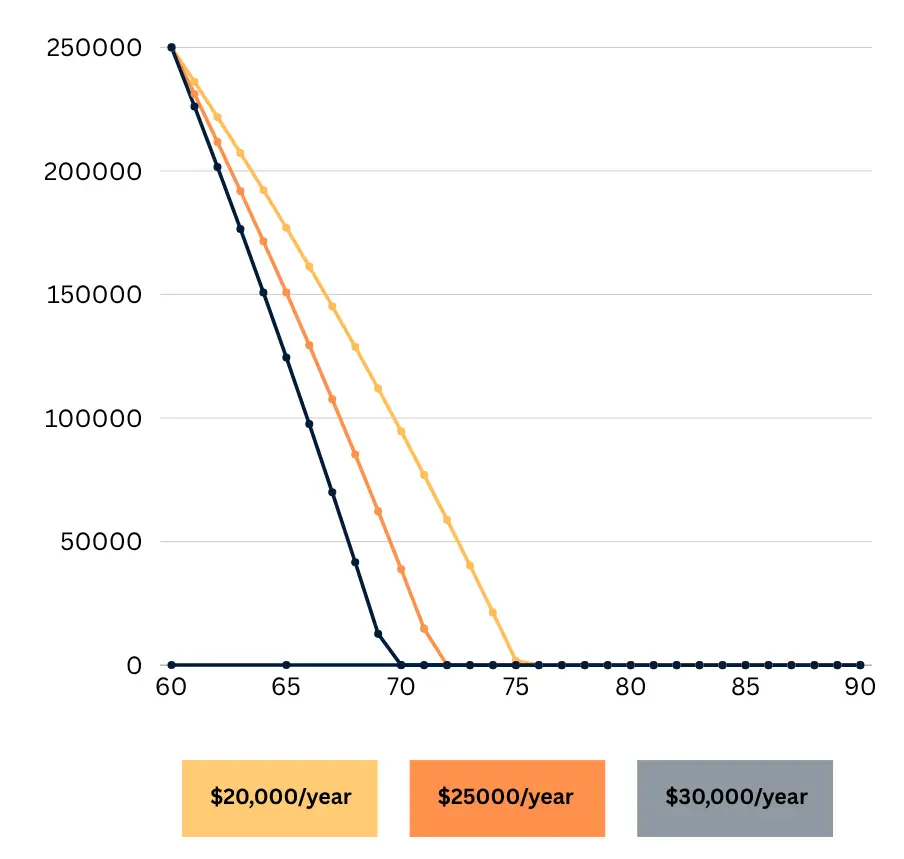

From 60 to 67, there is no Age Pension and no Centrelink support for retirees. Everything comes from your super. At $250K, that is a real constraint.Drawing $22,000 to $25,000 a year from age 60, with modest investment returns, means consuming a substantial portion of the balance before 67. On relatively conservative assumptions, a remaining super balance anywhere from $80,000 to $120,000 at age 67 is plausible depending on actual returns and spending. For a homeowner, that remaining balance places most people well within eligibility for a full Age Pension.

That is the structural logic: spend carefully from 60 to 67, arrive at 67 with super partially depleted, and let the Age Pension carry the primary income load from there. Super then supplements the pension rather than replacing it.

The maths gets significantly harder if annual spending runs at $30,000 or above during the bridge years. At that rate, $250K depletes quickly and the remaining balance at 67 may not be sufficient to supplement the pension meaningfully. That is where the plan breaks down.

Scott and Phil covered the early retirement income gap and why timing matters so much in Episode 19: Is Early Retirement a Trap? The $150K Gap Most Aussies Miss. Worth watching for anyone working through numbers at this balance level.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

The Age Pension: The Engine of This Retirement Plan

At $250K, the Age Pension is not a supplement. It is the income foundation from 67, with super providing the bridge to get there and a modest ongoing top-up thereafter.

Current maximum Age Pension rates from 20 March 2026 are:

- Single: approximately $31,223 a year

- Couple (combined): approximately $47,070 a year

(Source: Services Australia, current as at March 2026. Rates are updated each March and September.)

For a single homeowner reaching 67 with around $90,000 to $110,000 remaining in super, the full Age Pension combined with a modest super drawdown of around $5,000 to $8,000 a year gives total retirement income in the range of $36,000 to $39,000. For a homeowner with no housing costs and genuinely modest needs, that is liveable.

Maximising your Age Pension entitlement at this balance level is one of the most valuable things a financial adviser can do for you. The difference between a full pension and a reduced one, based on how assets are structured, can be $5,000 to $10,000 a year for the rest of retirement. Our Pension and Centrelink page explains how the assets test and income test work, and what structuring decisions affect the outcome.

Episode 9 of the Wealthlab podcast, When Super Fund Advice Can Cost You the Age Pension, covered a real case where generic intra-fund advice cost a client significant Age Pension entitlements they should have received. At $250K, that kind of mistake is particularly damaging.

Accessing Super at 60: The Key Point

At 60, you reach preservation age. But access to super is not automatic. You need to meet a condition of release, the most common being that you have genuinely retired and do not intend to return to work in a similar capacity.

Once you meet the conditions, converting your accumulation super to an account-based pension means the investment earnings in the fund attract zero tax, compared to 15% in accumulation phase. Over a seven-year bridge period, that difference adds up. Episode 18 of the podcast, Is 61 the New Retirement Age in Australia?, covered the conditions of release and the retirement definitions in detail.

What the Retirement Lifestyle Looks Like at $250K

Home ownership is not optional at this balance. It is the foundational assumption on which everything else rests. A homeowner with no mortgage or rent has dramatically lower essential costs than a renter, and the family home is excluded from the Age Pension assets test. Both factors are critical.

For a homeowner spending around $22,000 to $24,000 a year, retirement at 60 with $250K can cover:

- Basic groceries, household bills and essential insurance

- Public healthcare supplemented by a modest private health policy

- Transport costs for one car or public transport

- Low-cost local activities and occasional short domestic travel

Overseas travel, significant lifestyle spending or any ongoing debt repayment is generally not compatible with this income level during the bridge years. And a single large unplanned expense, a car replacement, a health issue or a home repair, can materially shorten the runway if it hits early.

For renters with $250K, a full retirement at 60 is very difficult to make work. Housing costs on top of basic living expenses push required drawdown well above what $250K can sustain over seven years.

Our retirement planning page has more on how Wealthlab approaches income planning for retirees at different balance levels.

What Makes the Difference at $250K

Looking at what tends to separate viable retirements at this balance from those that come unstuck:

Part-time or casual income in the early years. This is the single most effective lever. Earning $8,000 to $12,000 a year from 60 to 63 or 64 cuts the annual super drawdown roughly in half during the most critical years. A balance of $250K drawing $13,000 a year in net withdrawals survives the bridge to 67 in much better shape than one drawing $24,000. Many people at this balance find a gradual step-down more sustainable personally too.

Spending that is genuinely below $24,000 a year. Not aspirationally low, actually low. Some retirees achieve this naturally, particularly those who have lived below their means for decades or who move to a lower cost area in retirement. Others find spending drifts higher than planned when free time opens up new costs. Knowing which category you fall into before committing to the plan matters.

Converting to an account-based pension on retirement. Once you meet a condition of release, this step removes the 15% tax on investment earnings inside the fund. At $250K earning modest returns over seven years, the compounding tax saving is worth capturing.

Understanding the Age Pension means test properly. At this balance, you will almost certainly qualify for the full Age Pension at 67. But how assets are structured can affect the timing and the amount. Getting advice specifically on the Age Pension interaction before you retire is worth doing at $250K.

Episode 10, How the Age Pension Really Works (With Real Case Studies), walked through how the assets test and income test interact with super balances in practice and why assumptions about automatic eligibility can be costly.

Investment Strategy at This Balance

With $250K and seven years of bridge to manage, getting the investment mix broadly right matters. All-cash earns minimal returns and risks being eroded by inflation. All-growth creates sequencing risk if markets fall early.

A common approach is keeping one to two years of living expenses in a stable option as a buffer, with the remainder in a balanced or moderately growth-oriented mix. That way a short-term market fall does not force you to sell growth assets at a loss to fund daily living costs. The Wealthlab podcast covered why this matters in Episode 1: Why Playing It Safe in Retirement Can Cost You More.

Our superannuation page covers how Wealthlab approaches investment strategy in retirement for clients at different balance levels.

Want to run different scenarios for your own numbers? Try the free Wealthlab super calculator as a starting point.

A General Retirement Scenario

For a single homeowner at 60 with $250K in super, spending around $22,000 a year and doing some casual work earning around $10,000 a year until 63:

- Age 60 to 63: Net super drawdown reduced to around $12,000 a year after casual income. Balance reduces slowly during this period.

- Age 63 to 67: Full drawdown of around $22,000 a year. Balance reduces more noticeably over this four-year stretch.

- Age 67+: Full Age Pension likely accessible given remaining balance will typically be well within homeowner assets-test thresholds. Combined retirement income from pension and modest super drawdown potentially around $36,000 to $39,000 a year.

Without the casual income in the early years, the drawdown during 60 to 63 roughly doubles, the balance at 67 is lower, and the long-term income from 67 onward is tighter. That difference is meaningful at $250K.

Individual outcomes vary considerably. This is an illustrative shape only.

FAQ: Retiring at 60 with $250K in Australia

Can I retire at 60 with $250K in super? For homeowning Australians with genuinely low spending needs and ideally some supplementary income in the early years, retirement at 60 with $250K is possible as a bridge strategy to the Age Pension at 67. It is the balance in this series where a hard stop at 60 with no other income is most challenging. Individual circumstances vary considerably.

How long will $250K last in retirement? At $250K, the goal is not for super to self-fund retirement indefinitely. The goal is to bridge the seven years to the Age Pension at 67, with some balance remaining to supplement the pension from there. How long the bridge holds depends on drawdown rate, investment returns and whether supplementary income reduces withdrawals in the early years.

Will I get the full Age Pension with $250K at 67? A homeowner who starts at $250K and draws down carefully over seven years will almost certainly qualify for a full or near-full Age Pension at 67, as the remaining super balance will typically fall well within homeowner assets-test thresholds. Eligibility is assessed by Services Australia under the assets test and income test. Figures are current as at March 2026.

Does home ownership really matter that much at $250K? Yes, it is the most important single variable. Without housing costs, essential spending is dramatically lower. The family home is also excluded from the Age Pension assets test, meaning owning your home does not reduce your pension entitlement. Both factors are critical to making retirement viable at this balance.

What if I am renting with $250K at 60? The numbers are very tight. Rent on top of regular living costs would push required drawdown well above what $250K can sustain across a seven-year bridge to the pension. Renting retirees at this balance generally need supplementary income, a different retirement date or a significantly lower cost of living to make the plan workable.

Is working a few more years to 63 or 65 worth considering? For most people at this balance, yes. Three to five more years of contributions going in and nothing being drawn out makes a meaningful difference to the remaining balance and how long retirement income lasts. Whether that trade-off suits you depends on health, employment and what retirement means to you personally.

This Line Chart Showing how $250K depletes across 30 years at $20K, $25K, and $30K annual spending.

Talk It Through with Wealthlab

If you are approaching 60 with around $250K and trying to work out whether retirement is realistic, getting clarity on the specifics matters. At this balance, small decisions around drawdown timing, investment mix, account-based pension conversion and Age Pension structuring each carry more weight than at higher balances.

Wealthlab works with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how the general principles here might apply to your circumstances.

If you want to see how the numbers compare at a higher balance, our post on Can I Retire at 60 with $275K? covers the next step up in this series.