This is one of the more manageable scenarios in the Wealthlab retirement series, and here is why. Retiring at 65 with $300K in super and a paid-off home is fundamentally different to retiring at 60 with the same balance. The gap before the Age Pension starts at 67 is two years, not seven. That shorter bridge changes the maths considerably, and for a homeowner with modest spending, it makes retirement at 65 genuinely workable for many Australians.

That does not mean there is nothing to plan for. Two years of self-funded retirement still draws down a meaningful portion of $300K, the investment mix still matters, and the Age Pension means test still needs to be understood. But the structural challenge is much more contained than earlier retirement at this balance.

This post explains what retirement at 65 with $300K and a paid-off home can realistically look like, what the risks are, and what tends to determine whether the plan holds together long term.

Why 65 Is Different to 60 at This Balance

The posts earlier in this series cover retirement at 60 with balances from $250K to $580K. In each case, the defining challenge is the seven-year gap from 60 to 67 before the Age Pension begins.

At 65, that gap shrinks to two years. For a homeowner with $300K drawing around $28,000 to $30,000 a year, the bridge to 67 consumes roughly $50,000 to $60,000 of super, leaving around $240,000 to $250,000 at Age Pension age. For most homeowners, that remaining balance sits comfortably within assets-test thresholds for at least a part Age Pension.

That is the core logic of this scenario: manage two careful years from 65 to 67, then the Age Pension takes over as the primary income source. Super then supplements the pension rather than replacing it. Compared to a seven-year bridge at 60, this is substantially more achievable.

Where $300K Sits Against the Retirement Benchmarks

The ASFA Retirement Standard estimates a single homeowner needs around $595,000 in super (plus the Age Pension) for a comfortable retirement, and a couple needs around $690,000. (Source: ASFA)

At $300K, a single retiree is well below the comfortable benchmark. The relevant comparison at this balance is the ASFA modest retirement standard, which describes a homeowner largely supported by the full Age Pension with a modest super balance providing a top-up.

At 65 retiring two years before the Age Pension, $300K with home ownership is enough to bridge that gap and then support a modest but stable retirement income alongside the pension for many Australians. Whether that describes a “comfortable” or “modest” retirement in ASFA terms depends on individual spending and circumstances.

The Two-Year Bridge: 65 to 67

From 65 to 67, your super funds the entire retirement income. There is no Age Pension, no Centrelink support for retirees, and no other safety net beyond what you hold.

Drawing around $28,000 to $30,000 a year over two years with modest investment returns means consuming roughly $50,000 to $55,000 of your balance before the Age Pension begins. Assuming some investment growth offsets part of this, a remaining super balance in the range of $245,000 to $255,000 at age 67 is plausible for many people at this starting point.

For a homeowner with no significant other assets, a remaining super balance in that range would typically fall within assets-test thresholds for at least a part Age Pension, and possibly a full one depending on total assets. The assets test thresholds are updated each March and September by the Department of Social Services.

The key risk during the two-year bridge is not running out of money, the balance is more than adequate for two years,it is arriving at 67 with the balance structured in a way that optimises Age Pension eligibility. That is where specific advice adds value.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

Projecting the Numbers

Here’s a rough example of how it might play out if you retire at 65 and spend ~$30,000/year:

| Age | Super Balance | Annual Drawdown | Earnings (3%) | End Balance |

|---|---|---|---|---|

| 65 | $300,000 | $30,000 | $7,500 | $277,500 |

| 66 | $277,500 | $30,000 | $6,900 | $254,400 |

| 67 | $254,400 | $12,000 (reduced drawdown with Age Pension) | $6,300 | $248,700 |

| 70 | ~$230,000 | Ongoing drawdowns ~10–15k/year | Ongoing growth | ~$200,000 |

| 80+ | ~$100,000 | Smaller top-ups | +Age Pension | Balanced income |

Even with modest returns, your super can support you well into your 80s, especially if your Age Pension kicks in after 67.

This Line Chart Shows Depletion of $300K over time under different spending levels.

The Age Pension From 67: The Primary Income Source

From 67, the Age Pension becomes available subject to the assets test and income test.

Current maximum Age Pension rates from 20 March 2026 are:

- Single: approximately $31,223 a year

- Couple (combined): approximately $47,070 a year

(Source: Services Australia, current as at March 2026. Rates are updated each March and September.)

For a single homeowner reaching 67 with around $245,000 remaining in super, the pension entitlement depends on the assets test result. With $245,000 in super as the primary asset and a home that is exempt from the assets test, a homeowner is likely to be within partial or full pension territory. The exact amount requires a proper means-test assessment.

Combined retirement income from even a part Age Pension plus a modest super drawdown of $10,000 to $12,000 a year gives total income of roughly $38,000 to $43,000 for many people in this situation. For a homeowner with no housing costs, that is a stable, workable retirement income.

Getting the Age Pension structuring right is worth doing carefully at this balance level. Our Pension and Centrelink page explains how the assets test and income test work and what decisions affect the outcome. Episode 9 of the Wealthlab podcast, When Super Fund Advice Can Cost You the Age Pension, showed a real case where poor advice cost a client meaningful pension entitlements. At $300K, that kind of mistake is genuinely costly.

Accessing Super at 65: What to Know

At 65, accessing super is more straightforward than at 60. You have reached preservation age and, under the conditions of release, being 65 or older means you can access your super regardless of your employment status. You do not need to have retired in the same way the conditions apply at 60.

Converting your accumulation super to an account-based pension at retirement removes the 15% tax on investment earnings inside the fund. Over a 20 to 25 year retirement, that matters. Episode 18 of the Wealthlab podcast, Is 61 the New Retirement Age in Australia?, covered the conditions of release and account-based pension setup in detail.

What the Retirement Lifestyle Looks Like at $300K and 65

Home ownership is the foundation. Without a mortgage or rent, essential living costs drop significantly and the retirement income picture is more stable. For a homeowner spending around $28,000 to $30,000 a year, retirement at 65 with $300K can generally cover:

- Household bills, groceries and essential insurance

- Private health cover and routine medical and dental costs

- Running a car or using public transport

- Modest hobbies, local activities and occasional short domestic travel

- A small buffer for unexpected expenses

What it is unlikely to support comfortably is regular overseas travel, significant lifestyle spending or any ongoing debt repayment. But for homeowners who have genuinely modest spending habits, this lifestyle is achievable and sustainable once the Age Pension supplements super from 67.

Our retirement planning page has more on how Wealthlab approaches retirement income planning for clients at different balance levels.

Investment Strategy for a Short Bridge

With only a two-year bridge to the Age Pension, the investment strategy question at 65 is somewhat different to earlier retirement ages. The sequencing risk, a sharp market fall wiping out a large portion of the balance before it can recover, is still present but less severe over a two-year window than a seven-year one.

That said, the balance still needs to last the rest of retirement alongside the pension, potentially another 20 to 25 years. Going all-cash at 65 means inflation erodes purchasing power throughout. Some growth exposure continues to be relevant even in retirement.

A practical approach many people consider is keeping one to two years of living expenses in a stable option as a drawdown buffer for the bridge years, with the rest in a balanced or moderately growth-oriented mix. The Wealthlab podcast covered why this matters in Episode 1: Why Playing It Safe in Retirement Can Cost You More. Our superannuation page covers how Wealthlab approaches investment strategy in retirement.

Run your own numbers through the free Wealthlab super calculator to get a sense of how different scenarios affect your balance over time.

What Helps the Plan Work at This Balance

Owning your home outright. The title of this post is not incidental, home ownership is what makes retirement at $300K and 65 viable. Without it, the required annual drawdown to cover rent would be substantially higher, and the two-year bridge becomes much more stressful.

Spending that genuinely tracks below $30,000 a year. The bridge years from 65 to 67 are the period where spending discipline matters most. Withdrawing significantly more than planned in those two years reduces the balance arriving at 67 and may affect Age Pension eligibility.

Understanding how the Age Pension means test applies to your situation. The assets test and income test interact with your super balance, any other financial assets and your home ownership status. Getting a clear picture of what you will likely receive before you retire helps you plan the drawdown strategy around it. Episode 10, How the Age Pension Really Works (With Real Case Studies), is a practical walkthrough of how the tests apply in real scenarios.

Not leaving super in the wrong investment option at 65. Moving everything to cash at retirement is a common default that carries its own risks over a 20-year retirement. Taking specific advice before making any changes to your super investment option is worth doing.

A General Retirement Scenario

For a single homeowner at 65 with $300K in super, spending around $28,000 a year:

- Age 65 to 67: Drawing from super at around $28,000 a year. Investment returns partially offset the drawdown. Rough remaining balance at 67 around $245,000 to $255,000.

- Age 67+: Age Pension available, amount depending on assets test. Combined retirement income from pension and reduced super drawdown potentially around $38,000 to $43,000 a year for many people in this situation.

- Later retirement: Healthcare spending typically rises from the mid-70s. Building a modest buffer for this into long-term plans leads to more realistic projections.

Individual outcomes vary considerably. This is an illustrative shape, not a projection for any specific person’s situation.

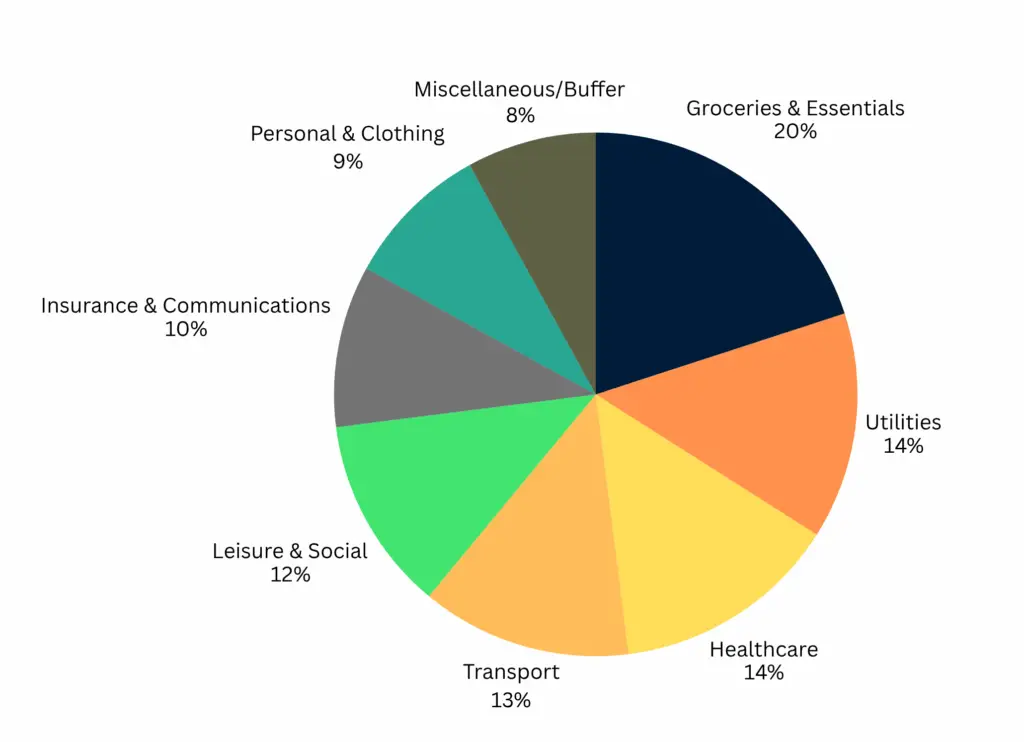

This Pie Chart Shows Budget allocation for a $25K–$30K yearly lifestyle.

FAQ: Retiring at 65 with $300K and a Paid-Off Home

Can I retire at 65 with $300K if I own my home? For many Australians with genuinely modest spending needs and no significant debt beyond the home, retirement at 65 with $300K is achievable. The two-year bridge to the Age Pension at 67 is the main challenge, and it is substantially more manageable than the seven-year bridge faced by those retiring at 60 with the same balance. Individual circumstances vary.

How does retiring at 65 compare to retiring at 60 with $300K? Very differently. At 60, the gap to the Age Pension is seven years, which is a very significant drawdown on $300K. At 65, the gap is two years. For a homeowner, two years of bridging on $300K is workable for most people. The shorter gap also means more of the balance survives to 67, which improves Age Pension eligibility and the long-term retirement income position.

Will I qualify for the Age Pension at 67 with $300K in super? A homeowner retiring at 65 with $300K who draws down carefully over two years will typically have a remaining balance around $245,000 to $255,000 at 67. For most homeowners, that places them within partial or full Age Pension territory depending on total assets and income. Eligibility is assessed by Services Australia under the assets test and income test. Figures are current as at March 2026.

Do I need to retire fully at 65 or can I work part-time? Many people at this balance find that continuing some part-time or consulting work for a year or two around 65 reduces the drawdown on super during the bridge years and improves the overall retirement picture. Whether that suits you depends on employment options, health and what retirement means personally.

What investment option should my super be in at 65? This depends on individual risk tolerance, income needs and retirement timeline. Most people benefit from maintaining some growth exposure through retirement rather than moving entirely to cash or a defensive option at 65. Taking specific advice before making any changes is worth doing.

What is the minimum super balance needed to retire at 65 in Australia? There is no single minimum figure, as it depends entirely on spending needs, other assets, home ownership and health. The ASFA modest retirement standard assumes relatively low super with a full Age Pension from 67 doing most of the income work. For homeowners, lower balances are more viable than for renters. For specific guidance, speaking with a financial adviser is more useful than any general benchmark.

Talk It Through with Wealthlab

If you are approaching 65 with around $300K and a paid-off home, and you are working out whether the numbers hold together, getting clarity on your specific situation is valuable. The Age Pension structuring, investment mix and drawdown approach in those two bridge years can all affect how the rest of retirement unfolds.

Wealthlab works with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how the general principles here might apply to your circumstances.

Not ready to book? Take the free Wealthlab retirement quiz for a general snapshot of where you stand.

If you want to see how the same balance plays out with a retirement at 60 instead of 65, our post on Can I Retire at 60 with $320K? covers the closest comparable scenario.