Retiring at 60 with $320K in super is possible for some Australians, but it is the balance in this series where honesty matters most. At $320K, a full retirement at 60 with no other income is a significant stretch for most people. The super needs to last seven years before the Age Pension starts, living costs are real, and the margin for error is narrow.

That said, $320K is not the end of the road. For homeowners with genuinely modest spending, and particularly for those willing to do some part-time work in the early years, a workable path to retirement at 60 does exist. The Age Pension, once it arrives at 67, becomes the primary income source at this balance level and it is a substantial one.

This post lays out what is realistic, what the risks are, and what tends to separate the retirement plans that work at $320K from those that do not.

Where $320K Sits Against the Retirement Benchmarks

The ASFA Retirement Standard estimates a single homeowner needs around $595,000 in super (plus the Age Pension) for a comfortable retirement, and a couple needs around $690,000. (Source: ASFA)

At $320K, a single retiree is around $275,000 below the comfortable benchmark. Even the ASFA modest retirement standard, which assumes a homeowner largely relying on the full Age Pension, is premised on a lower super balance than $320K only because the Age Pension is doing most of the income work from 67 onward.

The honest framing for $320K is this: the retirement plan is really a bridge strategy. You manage the seven years from 60 to 67 as carefully as possible, and then the Age Pension takes over as the foundation of your income. Super becomes a supplement to the pension rather than the primary funding source. That is a very different plan to the one people with $580K or $520K are running, and it is worth being clear about that from the start.

Accessing Super at 60: What It Actually Means

At 60, you reach preservation age, which means you can access your super if you meet a condition of release. The most common condition is retiring, meaning you have genuinely left an employment arrangement with no intention of returning to work in a similar capacity.

Accessing super is not automatic at 60. You need to meet a condition of release, and the rules around what counts as retirement have some nuance, particularly if you are considering part-time work. Episode 18 of the Wealthlab podcast, Is 61 the New Retirement Age in Australia?, covered the conditions of release in detail including the distinction between preservation age and actual retirement.

Once you do meet the conditions, super in retirement phase attracts zero tax on earnings, which is one of the key benefits of converting to an account-based pension at retirement.

The 60 to 67 Gap: The Make-or-Break Years

Seven years with no Age Pension and $320K in super is a real constraint. The maths is not comfortable if you try to run a full retirement income off this balance alone.

Drawing $26,000 to $28,000 a year with modest investment returns of around 4 to 5% per annum means the balance reduces over this period, though returns offset some of the drawdown. On conservative assumptions, a significant portion of the $320K is consumed before the Age Pension arrives. On more optimistic assumptions with stronger returns and lower spending, the balance survives more intact.

The people who make $320K work at 60 tend to share a few common factors: they own their home outright, their genuine living costs are below $26,000 a year, and most are doing at least some paid work in the early years rather than a complete stop. Even $10,000 to $15,000 a year from casual or part-time work dramatically changes the drawdown trajectory.

Scott and Phil discussed early retirement at modest balances in Episode 19: Is Early Retirement a Trap? The $150K Gap Most Aussies Miss. The episode is directly relevant for anyone running these numbers.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

Why the Age Pension Is the Foundation at This Balance

At $320K, the Age Pension is not a supplement to your retirement income. It is the retirement income, with super providing the bridge and a top-up.

Current maximum Age Pension rates from 20 March 2026 are:

- Single: approximately $31,223 a year

- Couple (combined): approximately $47,070 a year

(Source: Services Australia, current as at March 2026. Rates are updated each March and September.)

A homeowner who reaches 67 with $120,000 to $160,000 remaining in super after seven years of careful drawdown will very likely qualify for a full Age Pension. At that point, combined retirement income from the pension plus a modest super drawdown of around $8,000 to $10,000 a year gives total income in the range of $39,000 to $41,000 for a single person. That is liveable, particularly for a homeowner with no housing costs.

The assets test thresholds are updated each March and September by the Department of Social Services. A financial adviser can help you understand exactly where your assets sit relative to the current thresholds and whether any structuring choices can improve your entitlement. Our Pension and Centrelink page explains how the tests work in practice.

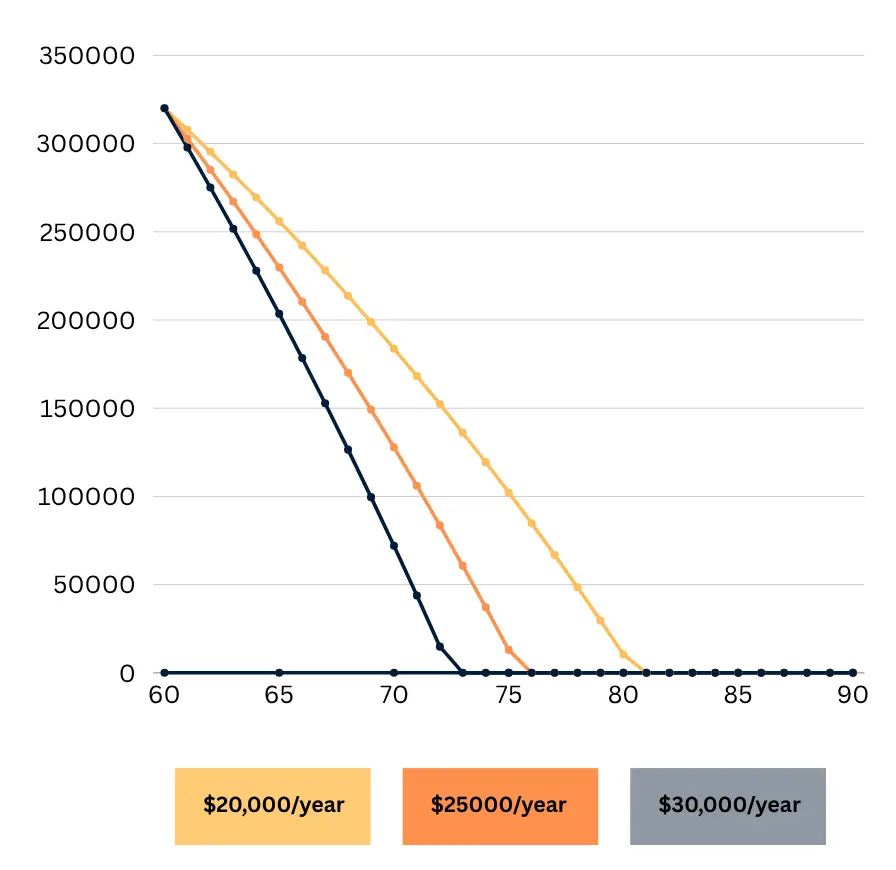

This Line Chart Showing how $320K depletes from ages 60 to 90 under $20K, $25K, and $30K/year spending levels.

Investment Strategy at $320K: Sequencing Risk Is the Key Concern

With $320K, investment risk is amplified compared to higher balances. A sharp market fall in the first two or three years of retirement is harder to recover from when the balance is smaller and you are drawing from it each year.

At the same time, parking everything in cash or a defensive option at 60 with potentially 25 to 30 years of retirement ahead risks inflation gradually eroding purchasing power year by year. A cash return of 2 to 3% per annum on $320K after fees provides very limited growth buffer.

The Wealthlab podcast covered the core mechanics of this in Episode 1: Why Playing It Safe in Retirement Can Cost You More. The episode showed that a conservative portfolio can actually run out of money faster than a growth one over a long retirement, because the lower returns compound negatively against ongoing drawdowns. For a $320K balance, that dynamic matters.

A practical approach many people at this balance consider is keeping one to two years of living expenses in a low-volatility option as a buffer, with the remainder in a diversified growth-oriented mix. That way, a short-term market fall does not force you to sell growth assets at a loss to fund living costs. Whether that structure suits your situation depends on personal factors. Our superannuation page has more on how Wealthlab approaches investment strategy in retirement.

Strategies That Make $320K More Workable

Part-time or casual work in the early years. This is probably the single most effective lever at this balance. Earning $12,000 to $18,000 a year from ages 60 to 64 or 65 cuts the annual super drawdown roughly in half during the most critical years, allows the balance to preserve more growth momentum, and tends to improve Age Pension eligibility at 67 by leaving more of the balance intact. Many people also find the transition easier personally when it is gradual rather than a hard stop.

Converting super to an account-based pension. Once you meet a condition of release, converting your super accumulation balance to an account-based pension means investment earnings in the fund are tax-free rather than taxed at 15%. For a balance of $320K drawing down over seven years, that tax saving is not enormous but it is real and worth doing.

Downsizing if the home has equity. If you own a property with meaningful equity, selling and downsizing to something smaller or cheaper frees up capital. The Downsizer Contribution Scheme allows you to contribute up to $300,000 per person from the proceeds back into super, which would fundamentally transform the retirement picture from a $320K starting point. Scott and Phil covered the rules and traps in Episode 2: Downsizer Contributions: The Hidden Traps You Must Know, including the 90-day rule and the effect on the Age Pension assets test.

Boosting super before retiring. If you are still working and have unused concessional contribution caps from prior years with a balance under $500,000, catch-up contributions can lift the balance before you stop work. Episode 10, How the Age Pension Really Works (With Real Case Studies), showed how well-timed contributions can save significant tax while boosting the balance heading into retirement.

See how different scenarios might shift your numbers with the free Wealthlab super calculator.

A General Retirement Scenario

For a single homeowner at 60 with $320K in super, spending around $26,000 a year and doing some part-time work earning $12,000 a year until 64:

- Age 60 to 64: Super drawdown is reduced to around $14,000 a year after part-time income. Balance reduces more slowly during this period.

- Age 64 to 67: Full drawdown of around $26,000 a year. Balance reduces more significantly during this stretch.

- Age 67+: Full Age Pension likely accessible given remaining balance will typically sit well within homeowner assets-test thresholds. Combined retirement income from pension and modest super drawdown potentially around $38,000 to $42,000 a year.

Without the part-time income, the 60 to 64 drawdown roughly doubles, the balance at 67 is lower and the long-term income picture is tighter. The difference between those two paths is meaningful.

Individual outcomes vary considerably. This is an illustrative shape only.

FAQ: Retiring at 60 with $320K in Australia

Can I retire at 60 with $320K in super? For homeowning Australians with genuinely modest spending and no significant debt, retirement at 60 with $320K is possible, though it is the balance in this series where the plan needs to be tightest. Most people who make it work at this balance are doing some part-time or casual work in the early years rather than a complete retirement at 60. Individual circumstances vary considerably.

How long will $320K last in retirement? This depends heavily on drawdown rate, investment returns, fees and whether any supplementary income offsets withdrawals in the early years. At a spending rate of $26,000 a year with modest growth, $320K can bridge the gap to 67 for many people, after which the Age Pension takes over as the primary income source. Running specific scenarios through a calculator or with an adviser gives a more reliable picture than any general estimate.

Will I qualify for the full Age Pension at 67 with $320K? A homeowner who starts with $320K at 60 and draws down carefully is very likely to qualify for a full or near-full Age Pension at 67, since the remaining balance will typically fall well within homeowner assets-test thresholds by that point. Eligibility is assessed by Services Australia under both the assets test and income test. Figures are current as at March 2026.

Does it make more sense to delay retirement to 63 or 65? For many people at this balance, working three to five more years makes a significant difference. It means more contributions going in, less drawn out during the bridge years, and potentially a higher balance at 67 that supports more comfortable retirement income thereafter. Whether that trade-off is right depends on health, employment options and personal circumstances.

What if I need to access super before 60? Superannuation generally cannot be accessed before preservation age (60 for most people born after 1964) unless you meet a specific condition of release such as permanent incapacity, terminal illness or severe financial hardship. Early access options are limited and often have tax consequences. Speaking with an adviser before pursuing any early access is worthwhile.

What are the biggest risks for a retirement at this balance? Overspending in the early years before the Age Pension arrives is the most common issue. Sequencing risk, a sharp market fall early in retirement when the balance is at its highest, is also more damaging at lower balances. And underestimating healthcare costs in later retirement is a consistent blind spot. The combination of all three can unravel an otherwise workable plan.

Talk It Through with Wealthlab

If you are approaching 60 with around $320K and working through whether retirement is realistic, getting clear on the specifics of your situation is genuinely valuable. At this balance, the structure of how you draw down, when you convert to an account-based pension, and how you approach the Age Pension means test can each make a meaningful difference to how the next 25 to 30 years unfold.

Wealthlab works with everyday Australians working through exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how the general principles here might apply to your circumstances.

If you want to see how the numbers compare at a slightly higher balance, our post on Can I Retire at 60 with $380K? covers similar ground for the next step up.