Retiring at 60 with $275K in super is one of the more challenging scenarios in this series, and it deserves an honest answer rather than an optimistic one. At this balance, a fully self-funded retirement from 60 to 90 is not realistic for most people. The super simply is not large enough to carry that load on its own.

But that is not the whole picture. Many Australians do retire with balances in this range, particularly those with interrupted careers, time out of the workforce or lower-income working lives. And for homeowners who are willing to manage spending carefully and accept some part-time work in the early years, a workable path to retirement at 60 exists. The Age Pension at 67 is not a safety net at this balance level. It is the plan.

This post is direct about what $275K can and cannot do, what makes the difference between a retirement that works and one that does not, and what to think about before making the call.

What $275K Means Against the Retirement Benchmarks

The ASFA Retirement Standard estimates a single homeowner needs around $595,000 in super (plus the Age Pension) for a comfortable retirement, and a couple needs around $690,000. (Source: ASFA)

At $275K, a single retiree is around $320,000 below that comfortable benchmark. The relevant comparison at this balance is the ASFA modest retirement standard, which assumes a homeowner relying primarily on the full Age Pension with a relatively small super balance supplementing it. That standard is achievable, but it requires the Age Pension to be doing the heavy lifting. And the Age Pension does not start until 67.

The seven years from 60 to 67 are the core challenge. During that window, $275K has to fund everything with no government support. How you manage that stretch largely determines whether the retirement holds together long term.

The 60 to 67 Bridge: Where the Numbers Get Tight

Drawing $24,000 to $26,000 a year from age 60, with modest investment returns of around 4 to 5% per annum, means a significant portion of the $275K balance is consumed before the Age Pension starts. On conservative assumptions, the remaining super balance at 67 could be anywhere from $100,000 to $150,000, depending on returns and actual spending.

That remaining balance, for a homeowner with no other significant assets, would place most people well within eligibility for a full Age Pension at 67. And that is actually the structural logic of retirement at this balance: spend carefully from 60 to 67, arrive at 67 with the Age Pension eligibility largely intact, and let the pension carry most of the income load from there.

The maths only works if spending during the bridge years is genuinely modest. If living costs run at $32,000 to $35,000 a year, the balance depletes faster and the remaining super at 67 may not be enough to meaningfully supplement the pension. That is where the plan can come apart.

Scott and Phil discussed retirement timing and the pre-pension gap in Episode 19: Is Early Retirement a Trap? The $150K Gap Most Aussies Miss. The episode is directly relevant for anyone working through numbers at this balance level.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

The Age Pension: The Foundation of This Retirement Plan

At $275K, the Age Pension is not supplementary income. It is the primary income source once you reach 67, with super providing the bridge and a modest ongoing top-up.

Current maximum Age Pension rates from 20 March 2026 are:

- Single: approximately $31,223 a year

- Couple (combined): approximately $47,070 a year

(Source: Services Australia, current as at March 2026. Rates are updated each March and September.)

For a single homeowner who reaches 67 with around $120,000 to $140,000 remaining in super, a full Age Pension combined with a modest super drawdown of around $7,000 to $9,000 a year gives total income of roughly $38,000 to $40,000 a year. For a homeowner with no housing costs and genuinely modest spending needs, that is workable.

Understanding how the assets test and income test interact with your specific situation is critical at this balance level. Small structuring decisions, around whether assets are held inside or outside super, whether an account-based pension has been set up, and how Centrelink assesses your financial position, can make a real difference to the pension amount you receive. Our Pension and Centrelink page explains how the tests work and what Wealthlab looks at with clients in this situation.

Episode 9 of the Wealthlab podcast, When Super Fund Advice Can Cost You the Age Pension, looked at a real case study where generic advice led to a client losing Age Pension entitlements they should have received. At $275K, that kind of mistake is particularly costly.ard.

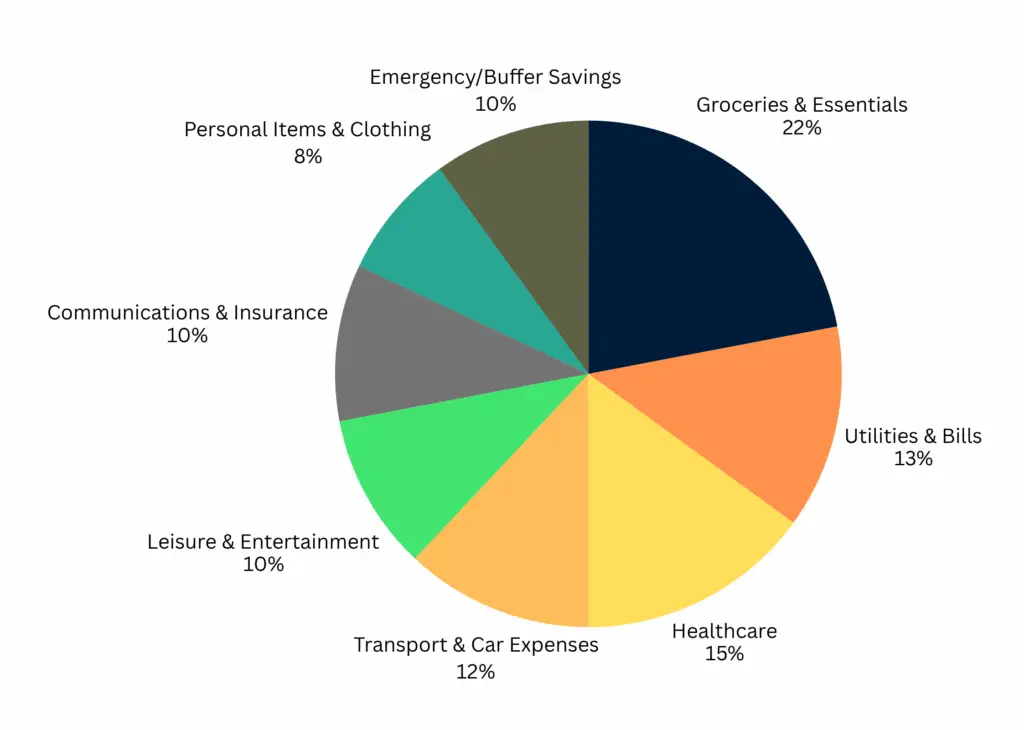

Budgeting for a $25K–$30K Lifestyle

Here’s how retirees typically allocate a $25K–$30K annual budget:

| Spending Category | % of Budget |

|---|---|

| Groceries & Essentials | 22% |

| Utilities & Bills | 13% |

| Healthcare | 15% |

| Transport & Car Expenses | 12% |

| Leisure & Entertainment | 10% |

| Communications & Insurance | 10% |

| Personal Items & Clothing | 8% |

| Emergency/Buffer Savings | 10% |

With careful management, this can support a modest but comfortable lifestyle especially for single retirees or couples who own their home.

What Makes Retirement at This Balance Actually Work

Looking across the people for whom retirement at 60 with a modest super balance holds together, a few factors consistently appear:

Home ownership with no mortgage. This is the single most important variable. A homeowner with no housing cost has fundamentally lower essential expenses than a renter, and the Age Pension assets test excludes the family home. That combination is what makes a modest super balance viable. Without home ownership, $275K is genuinely very tight.

Spending that genuinely sits below $26,000 a year. Not aspirationally modest, actually modest. Some retirees achieve this comfortably, particularly those who have always lived below their means or who move to a lower cost-of-living area. Others find that spending naturally drifts higher than planned in the early years of retirement when time and freedom are new. Knowing which category you are in is important before committing to a retirement at this balance.

Some supplementary income in the early years. Even $8,000 to $12,000 a year from casual work, a small rental income, or consulting cuts the annual super drawdown substantially and allows more of the balance to survive to 67. Many people at this balance find that a gradual step-down out of work rather than a hard stop at 60 serves them better both financially and personally. Episode 19 covered why the retirement date itself matters more than most people realise.

Converting super to an account-based pension on retirement. Once you meet a condition of release and retire, converting your accumulation balance to an account-based pension means investment earnings in the fund attract zero tax rather than 15%. For $275K drawn over seven years, that tax saving adds up. Episode 18, Is 61 the New Retirement Age in Australia?, covered the conditions of release and when this conversion makes sense.

Investment Strategy: Keeping Risk Appropriate

With $275K and a seven-year bridge to the Age Pension, investment strategy needs to balance two competing concerns: not going so conservative that inflation erodes the balance year by year, and not taking on so much growth risk that a market fall early in retirement significantly damages the balance before it recovers.

A common approach for people in this situation is to hold one to two years of living expenses in a stable, low-volatility option as a drawdown buffer, with the rest in a balanced or moderately growth-oriented mix. That way, short-term market falls do not force you to sell growth assets at a loss to fund living costs.

The Wealthlab podcast covered the core logic of retirement investment strategy in Episode 1: Why Playing It Safe in Retirement Can Cost You More. The episode is worth understanding at any balance, but particularly at $275K where there is less room to absorb the consequences of getting the mix wrong.

Our superannuation page covers how Wealthlab approaches investment strategy for clients in or near retirement.

A General Retirement Scenario

For a single homeowner at 60 with $275K in super, spending around $24,000 a year and doing some casual work earning around $10,000 a year until 64:

- Age 60 to 64: Net super drawdown reduced to around $14,000 a year after casual income. Balance reduces slowly during this period.

- Age 64 to 67: Full drawdown of around $24,000 a year. Balance reduces more noticeably during this final stretch before the pension.

- Age 67+: Full Age Pension very likely accessible given remaining balance will typically be well within homeowner assets-test thresholds. Combined retirement income from pension and modest super drawdown potentially around $38,000 to $40,000 a year.

Without the casual income from 60 to 64, the bridge-year drawdown roughly doubles, the balance at 67 is lower, and the overall retirement income position is tighter. The difference between the two paths at this balance level is meaningful.

Individual outcomes vary considerably. This is an illustrative shape only, not a projection for any specific person’s situation.

FAQ: Retiring at 60 with $275K in Australia

Can I retire at 60 with $275K in super? For homeowning Australians with genuinely low spending needs and ideally some supplementary income in the early years, retirement at 60 with $275K is possible as a bridge strategy to the Age Pension at 67. It is the balance in this series where full retirement with no other income from age 60 is the most challenging scenario. Individual circumstances vary considerably.

How long will $275K last? This depends on your drawdown rate, investment returns and whether any supplementary income reduces withdrawals in the early years. The goal at this balance is not for $275K to self-fund retirement indefinitely, but to bridge the gap to 67 with enough remaining for the Age Pension to carry the primary load thereafter. Running specific scenarios with an adviser gives a more reliable picture than any general estimate.

Will I qualify for the full Age Pension with $275K? A homeowner who starts retirement at 60 with $275K and draws down carefully over seven years will very likely qualify for a full or near-full Age Pension at 67, since the remaining balance will typically fall well within homeowner assets-test thresholds. Eligibility is assessed by Services Australia under the assets test and income test. Figures are current as at March 2026.

Does home ownership really make that much difference? At this balance, yes, substantially. A homeowner with no housing costs needs to draw significantly less from super each year than a renter. The family home is also excluded from the Age Pension assets test, meaning owning your home does not reduce your pension entitlement. Those two factors combined make home ownership the biggest single variable in whether retirement at $275K is viable.

What if I am still renting at 60 with $275K? The numbers are very tight. Rent costs on top of regular living expenses would push annual spending well above what $275K can comfortably sustain through a seven-year bridge to the pension. Retiring at 60 with $275K and no home ownership generally requires either supplementary income, a lower cost-of-living situation, or a later retirement date to make the plan workable.

Should I consider working until 63 or 65 instead? For many people at this balance, working a few more years makes a meaningful difference. More contributions go in, less is drawn out, and the remaining balance at 67 is higher, which means more flexibility in how much pension you draw on from there. Whether that trade-off is right depends on health, employment options and what retirement actually means for you personally.

Talk It Through with Wealthlab

If you are approaching 60 with around $275K and trying to work out whether the numbers can hold together, getting clarity on the specifics of your situation is worth the time. At this balance, decisions around drawdown timing, investment mix, account-based pension conversion and Age Pension structuring each carry more weight than at higher balances, because the margin for error is smaller.

Wealthlab works with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how the general principles here might apply to your circumstances.

If you want to see how the numbers compare at a higher balance, our post on Can I Retire at 60 with $320K? covers similar ground for the next step up.