Retiring at 55 with $300K is one of the most challenging scenarios in this series, and it is worth being direct about why before getting into the numbers. The challenge is not just the 12-year gap before the Age Pension starts at 67. It is the fact that for most Australians in 2026, you cannot access your super at 55 at all.

Preservation age in Australia is 60 for anyone born after 30 June 1964. If you are 55 in 2026, your super is locked for another five years. So retiring at 55 with $300K in super does not mean drawing from $300K from day one. It means drawing from whatever you hold outside super for the first five years, while leaving the $300K untouched until 60.

For most people at 55, the question is therefore not just whether $300K in super is enough. It is whether they have enough outside super to fund five years first.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

The Three Phases of Retirement at 55 with $300K

Retirement at 55 has three distinct phases, each with its own funding challenge.

Phase 1: Age 55 to 60, Outside Assets Fund Everything

Super is inaccessible during this period for most Australians. All living costs must come from savings, investments and income held outside super, rental income, a partner’s income or part-time work.

At $25,000 a year in spending, five years of outside-super funding requires around $125,000 in accessible assets. At $30,000 a year, around $150,000. For most people, that means the question “can I retire at 55 with $300K?” needs a companion question: “and how much do I have outside super?”

A genuine full stop at 55 with $300K in super and minimal outside assets is very difficult. The five-year period to age 60 needs to be funded from somewhere.

Phase 2: Age 60 to 67, Super Becomes Accessible

At 60, you reach preservation age and can access your super after meeting a condition of release, such as genuinely retiring. If the $300K has been sitting invested from 55 to 60 without being touched, five years of growth at modest returns could mean the balance has grown by the time you access it.

From 60 to 67 is a seven-year window where super funds the retirement income with no Age Pension support. At $25,000 a year with modest returns, a meaningful portion of the $300K is consumed during this period. How much remains at 67 determines the Age Pension eligibility and long-term income position.

Episode 18 of the Wealthlab podcast, Is 61 the New Retirement Age in Australia?, covered preservation age and the conditions of release that apply when you stop work at or around 60. Worth listening to if you are planning around the 55 to 60 window.

Phase 3: Age 67 Onwards, The Age Pension as Primary Income

From 67, the Age Pension becomes available subject to the assets test and income test. Current maximum rates as at March 2026 are:

- Single: approximately $31,223 per year

- Couple combined: approximately $47,070 per year

(Source: Services Australia. Rates are updated each March and September.)

For a homeowner who has drawn carefully from outside assets then super across 12 years, the remaining super balance at 67 will often sit within assets test thresholds for a full or near-full Age Pension. At $300K starting balance, that outcome is likely for most homeowners given how much of the balance is consumed over 12 years. At that point the Age Pension becomes the primary income foundation, with remaining super providing a supplement.

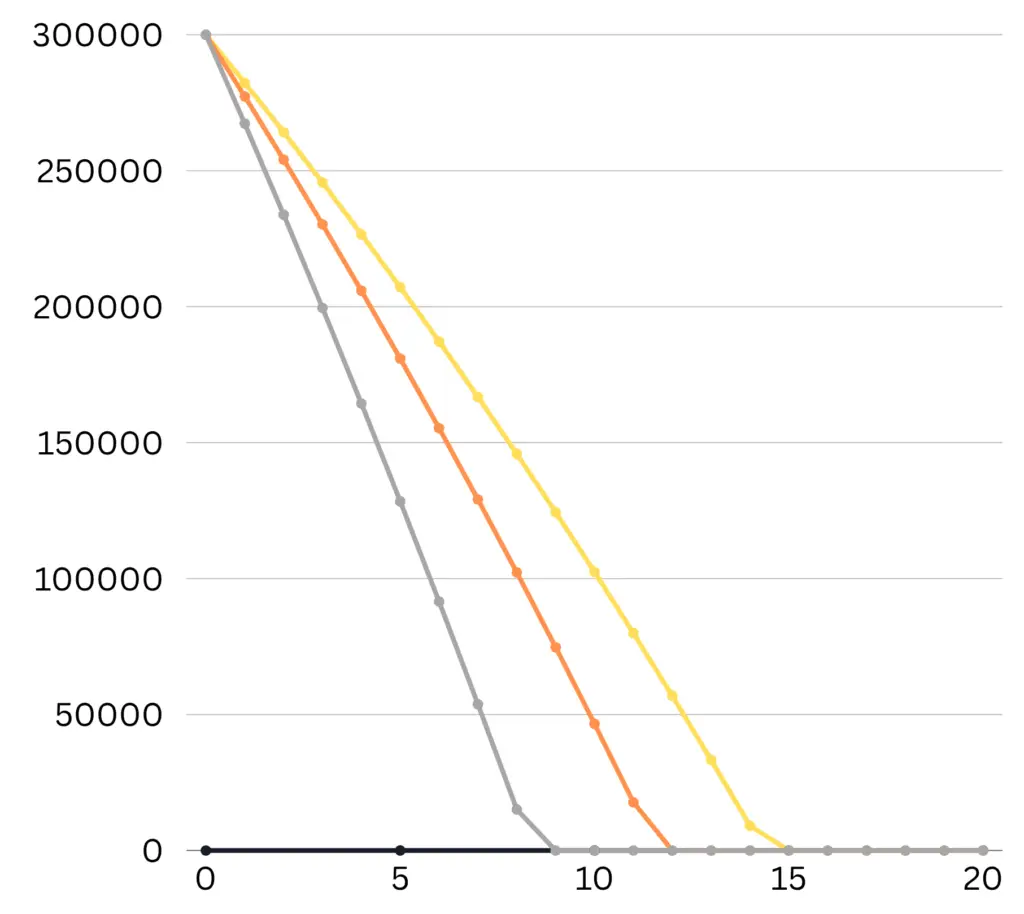

How Long Will $300K Last From Age 60?

If you reach 60 with $300K still intact after five years of living from outside assets, here is an illustrative guide to how long it might last from age 60 onward:

| Annual Spending from 60 | How Long $300K May Last |

|---|---|

| $25,000 per year | approximately 11 to 13 years |

| $30,000 per year | approximately 9 to 11 years |

| $40,000 per year | approximately 6 to 8 years |

These are illustrative estimates only. They assume a modest investment return after inflation with consistent annual withdrawals. Actual outcomes will vary based on investment returns, fees and personal circumstances.

At $25,000 a year from 60, $300K could carry many people to age 71 to 73 before the balance is substantially depleted. That is after the Age Pension has been supplementing income for four to six years already. At that remaining balance at 67, most homeowners will qualify for at least a part Age Pension and often a full one.

The investment return during the 55 to 60 period, when super is untouched and growing, is also meaningful. Five years of compound growth at even a modest 4 to 5% per year inside super can add $60,000 to $80,000 to the balance before you access it at 60. That is one of the structural arguments for leaving super untouched for as long as possible. Scott and Phil covered why investment mix matters so much across a long retirement in Episode 1: Why Playing It Safe in Retirement Can Cost You More.

What Lifestyle Can $300K Support at 55?

The ASFA Retirement Standard estimates a single homeowner needs around $595,000 in super plus the Age Pension for a comfortable retirement, and a couple needs around $690,000. (Source: ASFA)

At $300K, a comfortable retirement by ASFA standards is not achievable without significant outside assets or income. The realistic framing is that $300K, managed carefully across the three phases, can support a modest lifestyle:

- Basic household essentials, groceries and utilities

- Private health cover and routine medical costs

- Low-cost local activities and limited discretionary spending

- No significant ongoing debt

It is not a lifestyle that includes regular overseas travel, expensive hobbies or large one-off purchases. For a homeowner with no mortgage and genuinely modest needs, it is liveable, particularly once the Age Pension provides the primary income from 67.

For renters, $300K at 55 is very tight. The combination of rent, living costs and a 12-year gap before the Age Pension requires either meaningful outside assets or some ongoing income to work.

Graphic showing depletion of $300K over 25 years at three spending levels.

What Makes Retirement at 55 with $300K More Viable

Meaningful outside assets to fund 55 to 60. This is the first and most important requirement. If there is no accessible money outside super, retirement at 55 is not practically achievable. Shares, savings, property income or a partner’s income are what fund the first five years.

Leaving super untouched from 55 to 60. Five years of compound growth inside super, while living from outside assets, can lift the balance meaningfully before access at 60. Resisting the temptation to access super as soon as eligible tends to produce a better long-term outcome.

Part-time or casual income between 55 and 62 or 63. Earning $10,000 to $15,000 a year in the early years of retirement reduces drawdown on both outside assets and eventual super. It also helps maintain routine, social connection and a sense of purpose during what can be a significant personal transition.

Owning the home outright. Without rent or mortgage payments, essential costs are dramatically lower and the Age Pension assets test excludes the family home.

Understanding the Age Pension means test before retiring. At $300K, the chances of qualifying for a full Age Pension at 67 are relatively high for homeowners, but how assets are structured in the years before 67 can still affect the amount. Getting advice on this before drawing down is worthwhile. Our Pension and Centrelink page explains how the means test works.

Episode 9 of the podcast, When Super Fund Advice Can Cost You the Age Pension, covered a real case where poor structuring decisions cost a retiree significant pension entitlements. At $300K, that kind of mistake is genuinely costly.

Key Risks to Plan For

The outside asset gap is the biggest risk. If the plan relies on drawing from super at 55 when the super is legally inaccessible, the plan does not work. Many people are unaware of preservation age rules until they try to access their super.

Outliving savings. Retiring at 55 means potentially 35 to 40 years of retirement. A plan that only projects to 80 significantly underestimates the total funding required. Australian life expectancy is around 81 for men and 85 for women.

Healthcare costs in later retirement. Episode 19 of the podcast, Is Early Retirement a Trap? The $150K Gap Most Aussies Miss, noted that healthcare consumes around 34% of lifetime retirement savings on average, with spending spiking significantly in the final years of life.

Investment returns being lower than assumed. A portfolio that earns 2 to 3% after fees in a conservative option can lose real purchasing power year by year across a 35-year retirement. Getting the investment mix right during the 55 to 60 growth period inside super and through the drawdown years from 60 matters considerably.

A General Scenario

For a single homeowner at 55 with $300K in super, $130,000 in outside savings and spending around $25,000 a year:

Age 55 to 60: Living from outside savings of $130,000. Super sits invested and grows. At 5% per year, $300K could grow to around $380,000 by age 60, though actual returns will vary.

Age 60 to 67: Converting super to an account-based pension and drawing around $25,000 a year. Balance reduces over this period partially offset by investment returns. Remaining balance at 67 potentially around $200,000 to $240,000.

Age 67 onwards: Full or near-full Age Pension likely for a homeowner at this remaining balance. Combined income from pension and modest super drawdown potentially around $37,000 to $40,000 a year.

Individual outcomes vary considerably. This is an illustrative shape, not a projection for any specific situation, and assumes meaningful outside assets to fund the 55 to 60 period.

Use the free Wealthlab super calculator to run different scenarios for your own numbers.

FAQ: Retiring at 55 with $300K in Australia

Can I retire at 55 with $300K in super in Australia? For most Australians in 2026, super cannot be accessed until age 60. Retirement at 55 requires funding the five years from 55 to 60 entirely from outside assets. Whether $300K in super is enough depends on what else you hold outside super, whether you own your home and what your actual spending needs are. Individual circumstances vary considerably. This is general information, not personal advice.

Can I access my super at 55 in Australia? For most Australians in 2026, no. Preservation age is 60 for anyone born after 30 June 1964. If you are 55 today, your super is inaccessible until you turn 60 and meet a condition of release. The old transitional rules that set preservation age at 55 applied to people born before 1 July 1960, who are now 65 or older.

How long will $300K last in retirement from age 60? At $25,000 a year with modest investment returns, $300K may last approximately 11 to 13 years from age 60 for many people. At $30,000 a year, approximately 9 to 11 years. These are illustrative estimates only. The Age Pension from 67 reduces the annual super drawdown, extending how long the balance lasts. Actual outcomes depend on investment returns, fees and spending.

What is the gap between retirement at 55 and the Age Pension? The Age Pension starts at 67 for most Australians. Retiring at 55 means a 12-year gap before any government income support is available. Of those 12 years, the first five (ages 55 to 60) must be funded entirely from outside super, since super is inaccessible during this period for most people. The next seven years (60 to 67) can draw from super after meeting a condition of release at 60.

How much do I need outside super to retire at 55? At $25,000 a year in spending, funding the five years from 55 to 60 from outside assets requires approximately $125,000 in accessible funds. At $30,000 a year, approximately $150,000. This is before accounting for any investment growth or supplementary income. A genuine full stop at 55 with minimal outside assets is very difficult at any super balance.

Will I get the Age Pension at 67 if I retire at 55 with $300K? A homeowner who retires at 55 with $300K and draws carefully across 12 years will often find the remaining balance at 67 falls well within homeowner assets test thresholds for a full or near-full Age Pension. Eligibility is assessed by Services Australia under the assets test and income test at age 67. Figures are current as at March 2026.

Is working part-time from 55 to 62 a realistic approach? For many people at this balance and age, some form of part-time or consulting income in the early years is not optional, it is part of the plan. Earning $10,000 to $15,000 a year reduces drawdown on outside assets, lets super grow undisturbed until 60, and typically improves the overall position at both 60 and 67. Many people also find a gradual step-down is personally more sustainable than a hard stop.

Talk It Through with Wealthlab

Retiring at 55 with $300K has more moving parts than almost any other scenario in this series. The super access gap, the outside asset requirement, the long investment horizon and the Age Pension structuring all need to fit together over what could be a 35 to 40 year retirement. Getting advice specific to your situation is more valuable here than at almost any other retirement age or balance.

Wealthlab works with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how the general principles here might apply to your circumstances.

If you want to see how the same age plays out with a higher super balance, our post on Can I Retire at 55 with $400K in Australia? covers similar ground. For a $300K balance at a later retirement age, our post on Can I Retire at 60 with $320K in Australia? is the closest comparable.