Retiring at 55 with $600,000 in super is one of the more ambitious retirement goals Australians set, and it’s more achievable than most people think, but only if you understand the rules and plan the full 12-year runway to Age Pension age at 67.

The challenge isn’t the balance. $600K is a solid starting point. The challenge is the timing. Super can’t be touched until age 60. The Age Pension doesn’t start until 67. If you retire at 55, you’re looking at five years without super access and 12 years before Centrelink helps. That’s what the plan needs to solve.

Can I Retire at 55 With $600K in Super?

Yes, but the structure matters enormously.

From a legal standpoint, you can retire from work at any age in Australia. There’s no minimum retirement age. What you can’t do is access your super until you meet a condition of release, and for most Australians born after 1964, that’s age 60. So retiring at 55 means funding five years of living expenses entirely from sources outside your super.

After 60, your $600K becomes accessible tax-free and can be converted to an account-based pension. From 67, the Age Pension begins supplementing your income. The full plan looks like this:

- Age 55 to 60: Live on savings, investments, property income, or part-time work. Super stays invested and growing.

- Age 60 to 67: Access super tax-free. Draw an income stream. Seven years before the Age Pension.

- Age 67 onwards: Age Pension supplements super. Combined income improves significantly.

The people who make this work comfortably at 55 typically have savings or investments outside super of at least $150,000 to $200,000, a paid-off home, and a realistic spending plan of $35,000 to $45,000 per year.

Best Retirement Portfolio for a 55 Year Old: How to Invest $600K

This is one of the most searched questions by people in this age group, and it’s worth a detailed answer because most generic advice either undershoots or overcorrects.

The common mistake at 55 is shifting everything to cash or conservative investments because retirement feels imminent. The problem is you’re planning for a retirement that could last 35 years. At 55, you may have another three decades ahead. A portfolio that generates 2 to 3% in cash returns loses real value to inflation every year over that timeframe.

The best retirement portfolio for a 55 year old in Australia typically looks something like this:

Growth component (50% to 60%): Australian and international shares, listed property trusts, infrastructure. This drives long-term returns and inflation protection. Over 20 to 30 years, this component is what keeps your retirement income growing rather than shrinking in real terms.

Defensive component (40% to 50%): Bonds, cash, term deposits, and fixed income. This smooths volatility and provides stable drawdown capacity in down years, so you’re not forced to sell growth assets at a loss to fund living expenses.

The exact split depends on your risk tolerance and spending needs, but the principle is consistent: staying too conservative too early is one of the biggest retirement mistakes Australians make. Scott walked through the real cost of over-conservatism in Episode 1: Why Playing It Safe in Retirement Can Cost You More. The data from that episode showed a conservative portfolio running out 15 years earlier than a growth-oriented one for the same starting balance.

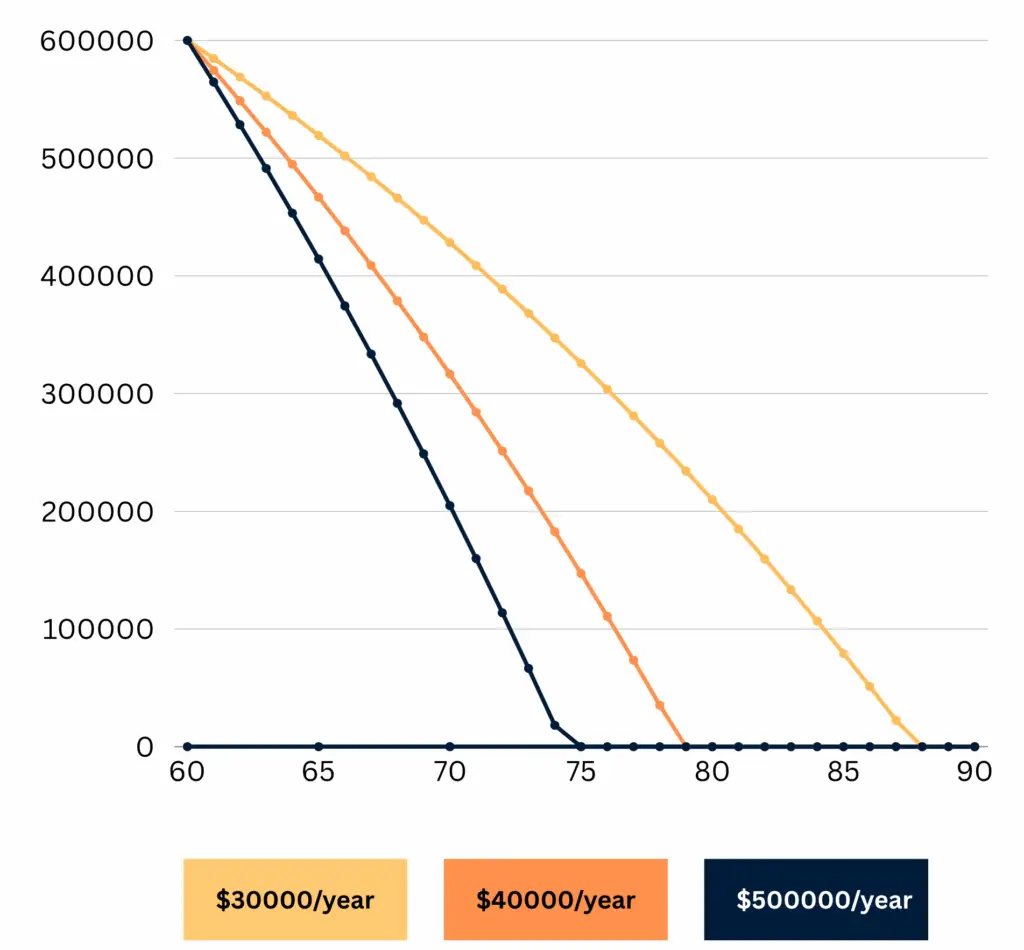

This Line Chart Show how $600K depletes from age 60 to ~90 at annual spending levels of $30K, $40K, and $50K.

Best Way to Invest $600K for Early Retirement

If you’re approaching 55 with $600K in super and asking how to best invest it, the answer has two layers: what’s inside super and what’s outside it.

Inside super (the $600K): Keep this in a growth to balanced investment option until at least 60. Over the five years between 55 and 60, your super stays invested and doesn’t get touched. At 6% average return, $600K grows to around $800K by the time you access it at 60. At 3% in a conservative fund, it grows to around $695K. That $100K difference compounds further through retirement.

Outside super (your bridge funding): This is what funds ages 55 to 60. Options include a cash or bond portfolio for stability, term deposits with staggered maturities to provide regular income, Australian dividend-paying shares for income with some growth, or investment property income if you have it. The MoneySmart retirement planner is a useful tool for modelling how different investment scenarios affect your income across the full retirement period.

Best Investment for a 55 Year Old in Australia

Beyond the portfolio mix, the best investments for a 55 year old Australian planning early retirement tend to share a few characteristics.

Low fees. At 55, you still have 30 or more years of compounding ahead. Fee differences that seem small compound dramatically over that period. A 1% annual fee difference on $600K over 25 years is well over $150,000 in lost returns.

Tax efficiency. Super in pension phase is tax-free on earnings. That’s a significant advantage over investing outside super. Keeping as much of your wealth inside super (within the transfer balance cap of $2 million) is generally the most tax-efficient structure.

Liquidity. At 55, some of your investments need to be accessible without penalty for the bridge years before super access. Illiquid assets like property or unlisted funds can create problems if you need cash before 60.

Inflation protection. At 3% inflation, prices double roughly every 24 years. A 55 year old planning to live to 85 needs their portfolio to at least keep pace with inflation for 30 years. Growth assets inside super are the primary tool for achieving this.

Best Jobs to Retire Early: What Income Helps Bridge the Gap at 55?

Not everyone retiring at 55 stops working entirely. Many people shift to part-time or flexible work that reduces income demands on their savings while maintaining purpose and routine.

The jobs that tend to work well for people semi-retiring at 55 in Australia share a few qualities: they can be done part-time or on a consultancy basis, they draw on established expertise rather than physical labour, and they’re flexible enough to allow extended travel or family time.

Common paths include consulting in your previous industry (typically 2 to 3 days per week), non-executive board or advisory roles, teaching, tutoring or mentoring in your field, freelance or project-based work, and property management or investment-related activities.

Even $20,000 to $25,000 per year in part-time income between 55 and 60 changes the retirement equation significantly. It cuts your annual drawdown on savings by half or more, meaning your super arrives at 60 considerably larger than if you drew everything from assets. It also keeps social connection and structure, which research consistently shows improves retirement wellbeing.

Cost of Living Crisis Australia: How It Affects Retiring at 55 With $600K

The cost of living in Australia has risen materially in the past two years, and it directly affects how far $600K stretches in early retirement.

ASFA’s comfortable retirement standard for a single person now sits at $54,240 per year, up from around $48,000 three years ago. For couples it’s $77,375 per year. The biggest drivers for retirees have been electricity, healthcare, insurance, and food, all of which have risen faster than general CPI.

What this means practically for someone retiring at 55 with $600K:

Spending $40,000 per year from ages 55 to 60 (before super access) means drawing $200,000 from outside savings. If your bridge fund is only $150,000, there’s a gap that needs part-time income or a reduced spending plan.

From 60, drawing $40,000 per year from super while it earns 5 to 6% means your $600K balance erodes slowly but has enough growth to last well into your 70s before the Age Pension takes over at 67.

The cost of living pressure also reinforces why keeping a meaningful allocation to growth assets matters. A static portfolio that earns less than inflation means your real income declines every year even if the nominal balance looks stable.

How Long Will $600K Last in Retirement?

At a 5 to 6% investment return from age 60 (when super access begins), here’s how $600K tracks:

| Annual Spending from Super | Balance at Age 75 | Balance at Age 85 |

|---|---|---|

| $30,000 per year | ~$570,000 | ~$430,000 |

| $40,000 per year | ~$400,000 | ~$195,000 |

| $50,000 per year | ~$235,000 | Near depleted |

From age 67, the Age Pension supplements income significantly. A single homeowner drawing $40,000 from super would receive around $20,000 to $22,000 per year in part Age Pension (assets-tested on the remaining balance), bringing total income to around $60,000 to $62,000 per year. That covers a comfortable retirement well above ASFA’s single standard.

Run your own numbers through the free Wealthlab super calculator to see how your balance, retirement age, and spending interact over the full retirement timeline.

Please note: These figures are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

The Five Years Before Super Access: Making 55 to 60 Work

This is the most underplanned part of early retirement and the one that most often causes problems.The bridge between 55 and 60 needs a dedicated funding strategy. Here’s what works:

A separate investment account outside super. This should hold enough to fund five years of living expenses, either in cash, term deposits, or a conservative investment portfolio. Staggering term deposits annually (one maturing each year) is a practical and low-stress way to generate predictable income.

Keeping super untouched and growing. The temptation to access super early (through severe hardship provisions or similar) should be resisted where possible. Every dollar that stays in super’s tax-advantaged environment continues to grow at a higher after-tax rate than most alternatives.

Health insurance planning. Before 60, you lose access to your employer’s group health insurance. Private health insurance becomes a personal cost and needs to be factored into your budget. Healthcare costs are one of the fastest-rising expense categories for retirees. The Services Australia financial information service can provide free guidance on entitlements and costs at different retirement ages.

The Age Pension From 67: Why It Changes Everything

At 67, the Age Pension starts and transforms the retirement equation for people with $600K.

A single homeowner who has drawn down $600K to around $400,000 by age 67 would be partially above the full pension threshold. They’d receive a part pension of around $20,000 to $24,000 per year. Combined with a $20,000 to $25,000 drawdown from remaining super, total income sits at $44,000 to $49,000 per year, comfortably above the modest standard and approaching comfortable.

For couples, the combined picture is even stronger. Understanding how to structure the drawdown between 60 and 67 to maximise your Age Pension entitlement from 67 is one of the highest-value planning decisions in retirement. Phil and Dan covered real case studies on how this plays out in Episode 10: How the Age Pension Really Works.

You can also check your eligibility and entitlements on the Services Australia Age Pension page and the who can get Age Pension page.

FAQs

Can I retire at 55 with $600K in super in Australia?

Yes, with the right structure. The key challenge is the five-year gap before super access at 60 and the 12-year gap before the Age Pension at 67. You’ll need savings or income outside super to fund ages 55 to 60, then a clear drawdown strategy for the super years. $600K is a solid foundation for this plan.

What is the best retirement portfolio for a 55 year old?

A balanced to growth-oriented portfolio with 50% to 60% in growth assets (shares, property, infrastructure) and 40% to 50% in defensive assets (bonds, cash). Shifting too conservative too early is the most common and costly mistake. At 55, you could have 30 years of retirement ahead. Growth assets are essential for maintaining real income over that timeframe.

What is the best way to invest $600K for retirement at 55?

Keep $600K inside super in a growth to balanced option to maximise the five years of tax-advantaged compounding before access at 60. Fund the bridge years (55 to 60) from a separate investment account outside super, structured for liquidity and stability.

How does the cost of living crisis affect my $600K retirement plan?

Rising costs, particularly electricity, healthcare, insurance, and food, mean your spending in retirement will be higher than benchmarks from a few years ago. The comfortable retirement standard for a single is now $54,240 per year. Build your retirement budget around current costs, not outdated figures, and ensure your portfolio has enough growth allocation to keep pace with inflation over 25 to 30 years.

What jobs are good for retiring early at 55?

Part-time consulting, advisory roles, tutoring, freelancing, or property-related work are all common paths. Even $20,000 to $25,000 per year in part-time income between 55 and 60 dramatically reduces the drawdown on your savings and allows your super to arrive at 60 larger than if you drew everything from investments.

How much outside super do I need to retire at 55?

As a guide, you need enough to fund five years of living expenses before super access at 60. At $35,000 per year in spending, that’s $175,000. At $45,000, it’s $225,000. Part-time income reduces this requirement significantly. The bridge fund doesn’t all need to be cash. A diversified investment portfolio generating income can also serve this purpose.

Ready to Plan Your Early Retirement?

Not sure whether retiring at 55 with $600K is realistic for your situation? Take the free Wealthlab retirement quiz for a general snapshot of your retirement readiness. Or book a free, no-pressure chat with the Wealthlab team to talk through your circumstances.