Reaching 67 with $500,000 in super puts you in a genuinely solid position. You’re at Age Pension eligibility age, your super is fully accessible tax-free, and $500K sits above the median balance for Australians in this age group. The question isn’t really whether you can retire. It’s how comfortably, and what you need to do to make it last.

This guide gives you honest numbers, 2026 Age Pension rates, and the practical steps that make $500K at 67 work well, not just technically.

Is $500K Enough to Retire at 67 in Australia?

Yes, $500K at 67 is enough to fund a comfortable to very comfortable retirement for most Australian homeowners. Here’s why 67 is the best age to retire with this balance.

You hit Age Pension eligibility the moment you turn 67. There’s no seven-year gap to bridge like there is at 60. Your $500K and the Age Pension start working together immediately, which is a fundamentally different and much more favourable retirement equation.

ASFA’s 2026 Retirement Standard puts a comfortable retirement at $54,240 per year for a single homeowner and $77,375 for a couple. With $500K in super plus the Age Pension, most homeowners in this situation can hit or get close to those figures without drawing too aggressively on their balance.

The key variables are still home ownership, spending level, and how your super is invested. But at 67 with $500K, you have more room to work with than most Australians.

How Much Will You Actually Have to Spend?

This is where most blogs give you a vague table and move on. Let’s be more specific.

At 67, a single homeowner with $500K in super would be partially above the full Age Pension assets threshold ($321,500 from March 2026). That means a part pension, not a full one. Here’s what the combined income looks like:

Single homeowner, $500K in super at 67:

- Estimated Age Pension: approximately $22,000 to $24,000 per year (part pension, assets-tested)

- Super drawdown at 5% per year: approximately $25,000 per year

- Total combined income: approximately $47,000 to $49,000 per year

That’s above ASFA’s comfortable standard for singles and gives real flexibility for healthcare, travel, and day-to-day living.

Couple, $500K combined super at 67:

- Estimated Age Pension: approximately $38,000 to $40,000 per year (part to full pension depending on combined assets)

- Super drawdown at 5%: approximately $25,000 per year

- Total combined income: approximately $63,000 to $65,000 per year

That comfortably covers ASFA’s comfortable couples standard of $77,375 at reduced drawing, or funds a genuinely good retirement lifestyle with slightly higher drawdown.

Use the free Wealthlab super calculator to model your specific balance, drawdown rate, and pension entitlement in your own numbers.

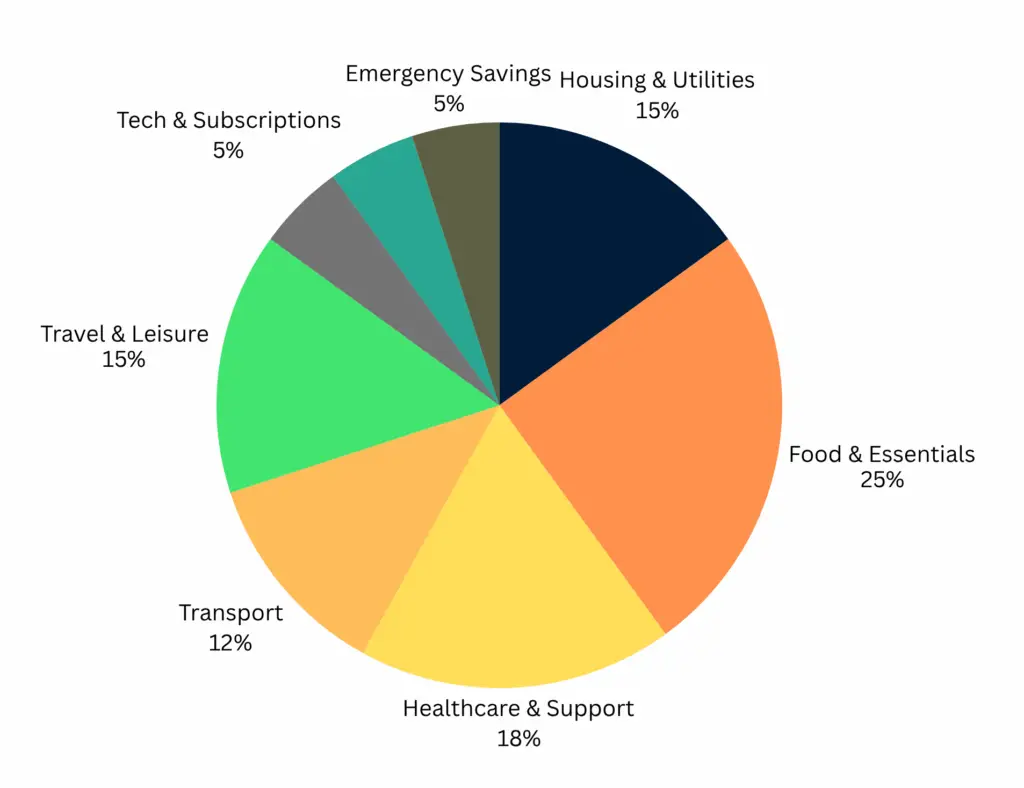

Here’s a sample pie chart breakdown of a $35K retirement lifestyle:

| Category | % of Budget |

|---|---|

| Housing & Utilities | 15% |

| Food & Essentials | 25% |

| Healthcare & Support | 18% |

| Transport | 12% |

| Travel & Leisure | 15% |

| Tech & Subscriptions | 5% |

| Miscellaneous | 5% |

| Emergency Savings | 5% |

Applying for the Age Pension at 67: What You Need to Know

One of the most important practical steps retirees miss is applying for the Age Pension at the right time. Services Australia does not backdate payments beyond your application date, so if you delay applying, you lose those payments permanently.

The process for applying for the Age Pension in Australia involves:

- Confirming eligibility on the Services Australia who can get Age Pension page. You need to be 67, an Australian resident for at least 10 years (with five continuous), and pass the assets and income tests.

- Gathering your documents, including identity documents, super fund details, property valuations, and bank statements.

- Submitting your claim through myGov or in person at a Services Australia service centre.

- Waiting for assessment, which can take several weeks.

The advice from financial planners is to apply for the Age Pension up to 13 weeks before you turn 67. That way your payments start from your 67th birthday rather than from whenever you get around to lodging the claim.

Scott and Phil covered the real-world mistakes people make with Age Pension timing and structuring in Episode 9: When Super Fund Advice Can Cost You the Age Pension. Worth watching before you apply.

Cost of Living in Retirement: What $500K Actually Has to Cover

One of the most searched questions among Australians approaching retirement is how to manage the cost of living in retirement, and whether super will keep pace with rising costs.

The cost of living crisis has hit retirees harder than most. ASFA data shows retirees’ major expenses, including electricity, healthcare, insurance, and food, have risen faster than general CPI over the past two years. The comfortable retirement benchmark for couples rose to $77,375 in early 2026, up from around $73,875 a year earlier.

What this means practically for someone with $500K at 67 is that the investment mix inside super still matters. If your $500K is sitting in a conservative or cash-heavy option, real returns after inflation may be minimal. At 5% nominal return and 3% inflation, you’re generating 2% real growth. At 3% nominal in a conservative fund, you’re barely keeping pace.

Keeping a meaningful allocation to growth assets, even in retirement, is one of the most important ways to protect your purchasing power over a 20 to 25 year retirement. Scott covered this directly in Episode 1: Why Playing It Safe in Retirement Can Cost You More. The data is clear: a growth-oriented portfolio consistently outperforms a conservative one over long retirement periods.

Best Retirement Advice for People Retiring at 67 With $500K

The most valuable retirement advice for people in this position isn’t about investment strategy in isolation. It’s about getting the structure right across super, the Age Pension, and tax.

Get the Age Pension structure right from day one. How you draw your super affects your deeming income and therefore your pension entitlement. Drawdown strategies can be designed to maximise combined super and pension income. This is not something the super fund itself will do for you, which is exactly the point Scott and Phil made in Episode 22: Grow Super Only With Free DIY Tools?.

Understand the difference between general and personal advice. Your super fund can give you intra-fund advice on your own fund’s products. An independent financial adviser can look at your full picture, including the Age Pension interaction, tax, estate planning, and investment mix across all assets. If you’re searching for “financial advisors near me” or “retirement advice near me” in Australia, what you’re really looking for is a licensed financial planner who specialises in retirement. Wealthlab’s retirement planning service is specifically built around this.

Review your super fund before you retire, not after. Many Australians arrive at 67 in whatever fund their employer chose for them 20 years ago. The fees, investment options, and pension phase features of that fund may not be the best fit for retirement. A financial adviser near you can assess whether your current fund is suitable or whether a different structure would serve you better.

Don’t ignore the Pensioner Concession Card. Even as a part pensioner, you qualify for the Pensioner Concession Card, which provides discounts on medicines through the PBS, council rates reductions (in most states), and cheaper energy bills. Over a full retirement, this adds up to thousands of dollars. It’s free, automatic once you’re on the pension, and widely undervalued.

Retirement Villages and Housing in Retirement

“Retirement villages near me” is a search that comes up often for people around 67, and it’s worth addressing directly because it has major financial implications.

Moving into a retirement village at 67 with $500K changes your assets test position significantly. Entry contributions (often $300,000 to $600,000 for a decent village in a metro area) are treated differently to your family home for Centrelink purposes. In many cases, the entry fee is partially assessable as an asset, which can affect your Age Pension entitlement.

The key questions before committing to a retirement village:

- Is the entry contribution refundable, and on what terms?

- How does the departure fee structure work (often 20% to 40% of the entry price)?

- How will it affect your Age Pension assets test?

This is one of the areas where getting retirement financial advice before signing anything is most important. Getting it wrong can cost you tens of thousands in reduced pension entitlements or exit fees.

How Long Will $500K Last at 67?

At a 5% investment return and moderate drawdown, here’s how $500K tracks at different annual spending levels from age 67:

| Annual Spending from Super | Balance at Age 80 | Balance at Age 90 |

|---|---|---|

| $20,000 per year | ~$430,000 | ~$330,000 |

| $30,000 per year | ~$290,000 | ~$100,000 |

| $40,000 per year | ~$155,000 | Near depleted |

These figures assume the Age Pension is also supplementing your income, meaning the total income at each row is higher than the super drawdown alone. At $30K drawn from super plus $22,000 from the Age Pension, total income is $52,000 per year, above the comfortable single standard, and your balance at 90 still has around $100,000 remaining.

The $40K scenario is where it gets tight. But remember, most retirees naturally reduce spending in their late 70s and 80s as health and mobility change spending patterns. ASFA’s older retiree standard shows spending typically drops 15 to 20% after age 80.

Retirement Financial Advice Near You: What to Look For

If you’re searching for retirement financial advice in Australia, here’s what actually matters.

The adviser should hold an Australian Financial Services Licence (AFSL) or be a representative of a licensee. You can check credentials on the MoneySmart financial advisers register. The register shows qualifications, complaints history, and current licence status.

Beyond credentials, what you want is an adviser who specialises in retirement planning, not just wealth accumulation. The strategies are different. Tax in accumulation phase, sequencing risk, Centrelink interactions, and estate planning all require retirement-specific knowledge.

Wealthlab’s team of retirement financial advisers works specifically with Australians in this transition, from final working years through to full retirement. If you’re looking for a retirement financial adviser near you, start with a free 15-minute call to see whether it’s the right fit.

FAQs

Can I retire at 67 with $500K in super?

Yes. At 67 you hit Age Pension eligibility, your super is fully accessible tax-free, and $500K combined with the part Age Pension gives most single homeowners a combined income of $47,000 to $49,000 per year. For couples with $500K combined, the figure is around $63,000 to $65,000. Both comfortably support a solid retirement for homeowners.

How do I apply for the pension in Australia?

Apply through myGov or at a Services Australia service centre. Gather your super fund statements, bank statements, and property details before you apply. Do it up to 13 weeks before you turn 67 so payments begin from your birthday. The Services Australia Age Pension page has the full application process.

What is the best interest rate for retirement savings in Australia?

Interest rates in 2026 have improved from pandemic lows, making cash and term deposits more attractive than they were. However, for a 20 to 25 year retirement, relying on cash rates alone means your balance loses real value to inflation over time. A diversified portfolio combining cash, bonds, and growth assets typically delivers better long-term outcomes for retirees.

How does the cost of living affect retirement with $500K?

Retirees’ core expenses, particularly healthcare, insurance, utilities, and food, have risen faster than general CPI in recent years. This means your super needs to generate real returns above inflation, not just nominal income. Keeping growth assets in your portfolio is the most effective way to protect purchasing power over a long retirement.

What is the best retirement advice for someone with $500K at 67?

Apply for the Age Pension early, set up an account-based pension with a drawdown strategy designed around your pension entitlement, keep growth assets in your investment mix, and get independent advice on the structure before you start drawing. The interaction between super drawdowns and pension entitlements is where most value is gained or lost in retirement.

Should I consider a retirement village with $500K?

Potentially, but get financial advice before committing. Entry fees for retirement villages can significantly affect your Age Pension assets test position, and departure fee structures can be complex. $500K gives you options, but understanding the full financial impact before signing is essential.

Where can I find a retirement financial adviser near me?

Check the MoneySmart financial advisers register to verify credentials. Look for a planner who specialises in retirement income rather than general wealth management. Wealthlab works with retirees across Australia and offers a free initial call to assess your situation. Book here.

Ready to Make Your $500K Work Properly at 67?

Getting the structure right at retirement makes a bigger difference to your income than most people realise. The combination of when you apply for the Age Pension, how you draw from super, and how your investments are positioned can add or subtract thousands per year from your retirement income.

Book a free 15-minute call with Wealthlab and get a clear picture of exactly what $500K at 67 means for your specific situation.