Yes, you can retire at 60 with $150K in Australia. But let’s be straight about what that means, because the honest answer is more nuanced than a simple yes.

$150,000 in super is well below the national average. It’s below every benchmark for a comfortable retirement. And retiring at 60 means seven years before the Age Pension starts at 67. That gap is the main challenge, not the balance itself.

The good news is that $150K, managed carefully, can bridge that gap. And once the Age Pension kicks in at 67, the picture changes considerably. Here’s exactly how it works.

Is $150K Enough to Retire at 60 in Australia?

On its own, $150K is not enough to fund a full 25 to 30 year retirement. But that’s not really the question. The question is whether it’s enough to get you to 67, when the Age Pension starts doing most of the heavy lifting.

For a single homeowner with no debt and modest spending, $150K can realistically fund the seven years between 60 and 67. After that, the Age Pension provides around $29,000 per year (from March 2026), and your remaining super tops it up.

What you need to make it work:

- You own your home outright. Renters face a fundamentally different retirement with this balance because housing costs consume the Age Pension before anything else.

- You have modest spending expectations, around $20,000 to $25,000 per year in the early years.

- You don’t make large lump sum withdrawals in the first few years.

- You keep your super invested rather than switching to cash.

If you tick those boxes, retiring at 60 with $150K is a real plan, not wishful thinking.

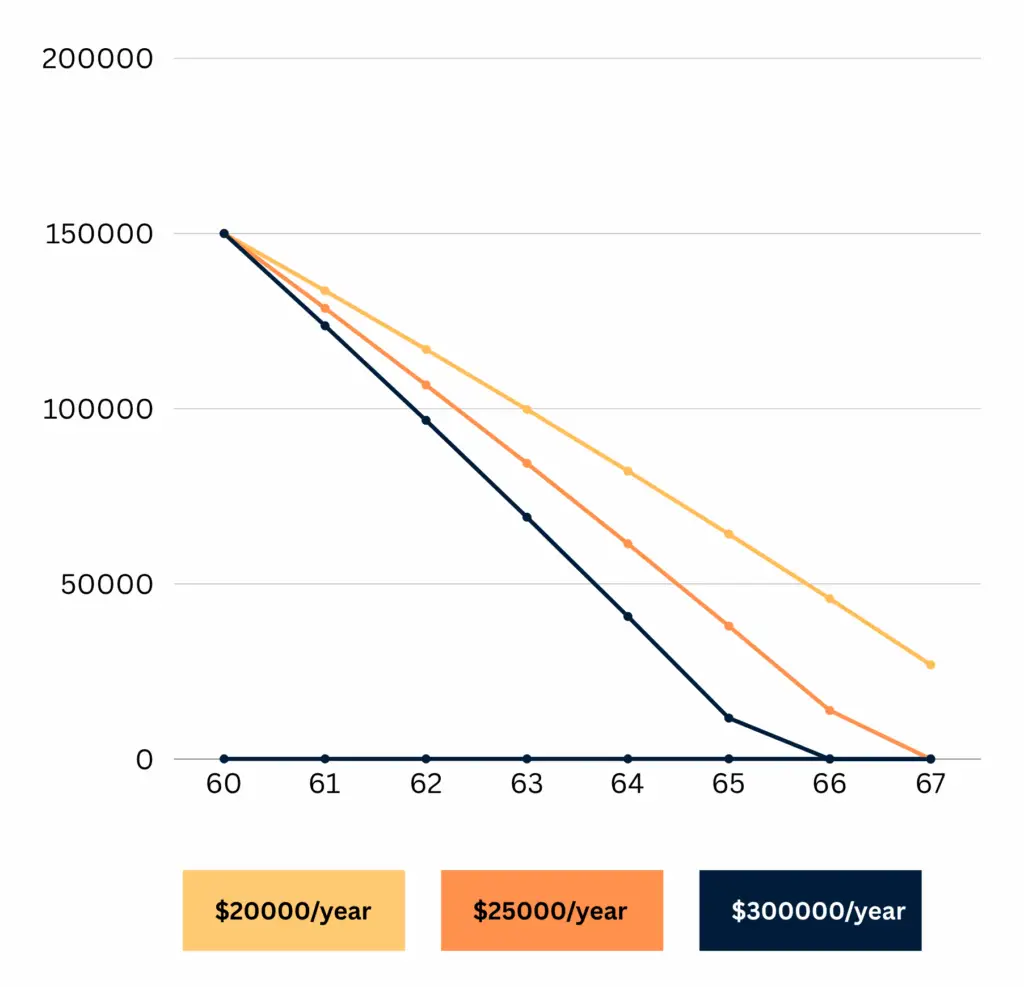

This Line Chart showing how $150K depletes from age 60 to 67 at $20K–$30K spending levels.

How Long Will $150K Last in Retirement?

This is the key number to understand. At a moderate return of 5% per year, here’s how $150K tracks at different spending levels:

| Annual Spending | Balance at Age 67 | Balance at Age 75 |

|---|---|---|

| $18,000 per year | ~$65,000 | ~$15,000 |

| $22,000 per year | ~$30,000 | Depleted ~72 |

| $28,000 per year | Near zero | Depleted ~65 |

The $22K scenario is the realistic middle ground for most homeowners. You arrive at 67 with around $30,000 left, the Age Pension starts at ~$29,000 per year, and your total income from that point is around $30,000 to $33,000 annually, covering a modest but functional lifestyle.

The $28K scenario is where it gets tight. Spending that much between 60 and 67 depletes $150K almost entirely before the pension starts. That’s why keeping drawdowns conservative in the early years is the most important lever you have.

Use the free Wealthlab super calculator to model your own spending level and see exactly where your balance lands at 67.

What Lifestyle Can $150K Support at 60?

Realistically, a single homeowner retiring at 60 with $150K can fund:

- Groceries, utilities, rates, and household bills

- Basic private health insurance

- A modest car and running costs

- GP visits, medications, and routine healthcare

- Local activities, hobbies, and social outings

- One domestic trip per year

What it won’t comfortably cover on $150K alone:

- Regular interstate or overseas travel

- Major home repairs or renovations

- Significant healthcare costs or dental work

- Financially supporting adult children

That changes from 67. Once the Age Pension supplements your income, you have a combined annual income that covers ASFA’s modest retirement standard ($35,503 per year for a single homeowner in 2026) and leaves a small buffer for unexpected costs.

Retiring at 60 in Australia: The Age Pension Is the Plan

With $150K in super, the Age Pension isn’t a backup. It’s the central pillar of your retirement income. Understanding it properly matters.

From March 2026, the maximum full Age Pension for a single person is approximately $29,000 per year, including all supplements. For couples, it’s around $43,700 per year combined. You can check the current rates on the Services Australia Age Pension page.

With $150K in super, you’d be well under the full pension assets threshold for a single homeowner ($321,500 as of March 2026). That means you’d receive the full pension, not a reduced part pension, from the moment you’re eligible at 67.

The practical implication is that your goal between 60 and 67 is simply to not run out entirely before the pension starts. Even arriving at 67 with $20,000 to $40,000 remaining means you have a small buffer on top of the full pension income.

Phil and Dan walked through how the Age Pension assets and income tests actually work with real case study numbers in Episode 10: How the Age Pension Really Works. If you’re in this situation, it’s worth a watch.

How to Make $150K Last Until 67: The Practical Steps

Set up an account-based pension at 60. This converts your super into an income stream where fund earnings become tax-free. You control how much you draw each year, and the balance stays invested. It’s far more efficient than leaving money in accumulation phase or taking a lump sum. The Services Australia thinking about retirement page has useful background on your options as you approach retirement age.

Draw the minimum you can live on. The minimum drawdown for an account-based pension at age 60 to 64 is 4% per year. On $150K that’s $6,000 per year. You’ll likely need more than that, but the principle is to take only what you need and leave the rest invested.

Keep growth assets in your portfolio. This is where people with modest balances make the most expensive mistake. Switching to cash or term deposits because $150K feels fragile actually accelerates how quickly it runs out. At 2% cash returns, $150K generates $3,000 per year. At 5 to 6% in a balanced portfolio, it generates $7,500 to $9,000 per year while you draw from it. That’s the difference between surviving the seven-year gap and not. Scott explained exactly why this matters in Episode 1: Why Playing It Safe in Retirement Can Cost You More.

Consider part-time work in the early years. Even $10,000 to $15,000 per year from part-time work between 60 and 65 can halve the drawdown from your super. That means you arrive at 67 with significantly more remaining, and you still qualify for the full Age Pension because your super balance stays under the threshold.

Know your Centrelink entitlements before you retire. Beyond the Age Pension, retirees with low incomes and assets may be eligible for the Pensioner Concession Card (which provides discounts on medicines, utilities, and transport), rent assistance if applicable, and advance pension payments for large unexpected costs. The Services Australia financial services for retirement page has the full picture of what’s available.

Can I Retire at 55 With $150K?

Technically yes, but super can’t be accessed until age 60. If you want to retire at 55, you need five years of income from savings, investments, or other sources before you can touch your super. With $150K in super and limited other assets, this is very tight.

If you’re considering early retirement at 55, it’s worth using the Services Australia financial information service, which offers free guidance on what’s available at different ages and how to plan the transition.

Retire at 60 With $150K: What About Couples?

For couples, $150K combined is extremely tight. $150K each is a more workable position.With $150K combined at 60, you’d be drawing down a joint balance across two people’s needs. At $35,000 combined annual spending, $150K depletes in under five years before the couple’s Age Pension starts at 67. This is a situation where part-time work, downsizing, or other income sources become essential rather than optional.

With $150K each ($300K combined), the picture improves substantially. The couple arrives at 67 with a meaningful combined balance, qualifies for the full couple’s Age Pension (around $43,700 per year), and has total combined income of around $55,000 to $60,000 per year, which sits above ASFA’s modest couples standard of $50,866.

Retiring at 60 vs 65 With $150K: Does Waiting Help?

Waiting from 60 to 65 makes a significant difference with a $150K balance.

At 60: Seven years until Age Pension. $150K must fund all income. Tight but achievable with low spending.

At 65: Only two years until Age Pension. $150K barely moves before Centrelink starts helping. At $22,000 annual spending for two years, you arrive at 67 with around $110,000 remaining, plus the full Age Pension starting immediately. This is a fundamentally more comfortable position.

Even two extra working years, or two years of reduced part-time work, transforms what $150K can deliver.

FAQs

Can I retire at 60 with $150K in Australia?

Yes, particularly if you own your home outright and are comfortable with modest spending of $18,000 to $22,000 per year in the years before the Age Pension starts at 67. The Age Pension is the foundation of this retirement plan, not the super balance itself.

How long will $150K last in retirement?

At $20,000 annual spending with a 5% investment return, $150K lasts approximately 10 to 12 years before depleting. In practice, for a retirement starting at 60, the Age Pension from 67 means your super doesn’t need to last 25 years on its own. It just needs to bridge the seven-year gap.

Can I retire comfortably at 60 with $150K?

A comfortable retirement in the ASFA sense requires considerably more. But a modest, secure retirement is achievable for homeowners. From 67, the Age Pension provides around $29,000 per year for singles, and combined with a small super drawdown, total income of $30,000 to $35,000 per year covers basic living costs well.

What happens to my super at 60?

At 60, you can access your super tax-free if you have retired or met another condition of release. The most tax-efficient option is converting it to an account-based pension, where earnings become tax-free and you draw a regular income. Taking large lump sums is generally less efficient for a $150K balance. The ATO page on conditions of release explains the rules.

Will I qualify for the full Age Pension with $150K in super?

Almost certainly yes, as a homeowner. From March 2026, single homeowners with assessable assets under $321,500 receive the full pension. With $150K in super and limited other assets, you’d be well under that threshold.

Can I retire at 60 with $150K and a partner?

It depends on your combined balance and spending. $150K combined is very tight. $150K each gives you more room, especially with the couple’s Age Pension of around $43,700 per year from 67. Part-time work for one or both partners in the early years makes a substantial difference.

Ready to Work Out If This Can Work for You?

The numbers above give you a framework, but your situation, your home, your health, your partner’s income, and your actual spending habits, shape whether $150K at 60 delivers a secure retirement or a stressful one.

Book a free 15-minute call with Wealthlab to get a clear picture of exactly where you stand, how the Age Pension fits in, and what adjustments would make the biggest difference to your retirement outcome.