Retiring at 60 in Australia is legal, increasingly common, and achievable at a range of super balances. Whether it is right for you depends on how much you have, what you plan to spend, whether you own your home, and how you manage the seven-year gap before the Age Pension starts at 67.

This guide answers the question directly, uses $370K as a worked example throughout, and covers the real benchmarks, the Age Pension interaction, how much super you should have at 60, and the practical steps that make retirement at 60 work.

Can You Retire at 60 in Australia?

Yes. There is no minimum age for retirement in Australia and no law requiring you to keep working. The rules that actually matter are:

Preservation age is 60. For anyone born after 1 July 1964, you can access your super tax-free from age 60 once you have retired from the workforce. You do not need to wait until 65 or 67.

The Age Pension starts at 67. That is the gap you need to plan for. Between 60 and 67, your super is your primary income source. From 67, Centrelink supplements it, which significantly extends how long your savings last.

Retirement age in Australia has no single official definition. The government sets the Age Pension eligibility age at 67. Super access starts at 60. Many Australians now retire somewhere between those two points and bridge the gap with savings.

Scott and Phil covered the exact conditions of release, what “retiring” actually means under super rules, and common mistakes about when you can and cannot access super in Episode 18 of the Wealthlab Podcast. Watch Episode 18 on YouTube.

How Much Super Should You Have at 60?

This is one of the most searched retirement questions in Australia, and the honest answer depends on what you want retirement to look like.

The most widely used benchmarks are from the ASFA Retirement Standard (February 2026 update):

| Modest lifestyle | Comfortable lifestyle | |

|---|---|---|

| Single homeowner | $35,199/year | $54,240/year |

| Couple homeowners | $50,866/year | $77,375/year |

The lump sum ASFA estimates for a comfortable retirement starting at age 67 is $630,000 for a single person and $690,000 to $730,000 for a couple. These assume the Age Pension supplements income from day one.

Retiring at 60 means you need more, not less. Seven years of drawdown before the Age Pension arrives means the same lifestyle requires a larger starting balance. As a practical guide:

- Single homeowner, modest lifestyle ($32,000–$35,000 a year): $330,000–$450,000 at 60 is workable

- Single homeowner, comfortable lifestyle ($50,000–$54,000 a year): $550,000–$700,000 at 60

- Couple, modest lifestyle ($45,000–$50,000 combined): $450,000–$600,000 combined at 60

- Couple, comfortable lifestyle ($70,000–$77,000 combined): $700,000–$900,000 combined at 60

The median super balance for Australians aged 60 to 64 is approximately $302,000 for men and around $211,000 for women according to APRA data. Most Australians retire with less than the ASFA comfortable benchmark. The Age Pension is what makes that workable.

For a deep dive on the gap between what most Australians have and what they actually need, Scott and Phil covered it in Episode 19 of the Wealthlab Podcast. Watch Episode 19 on YouTube.

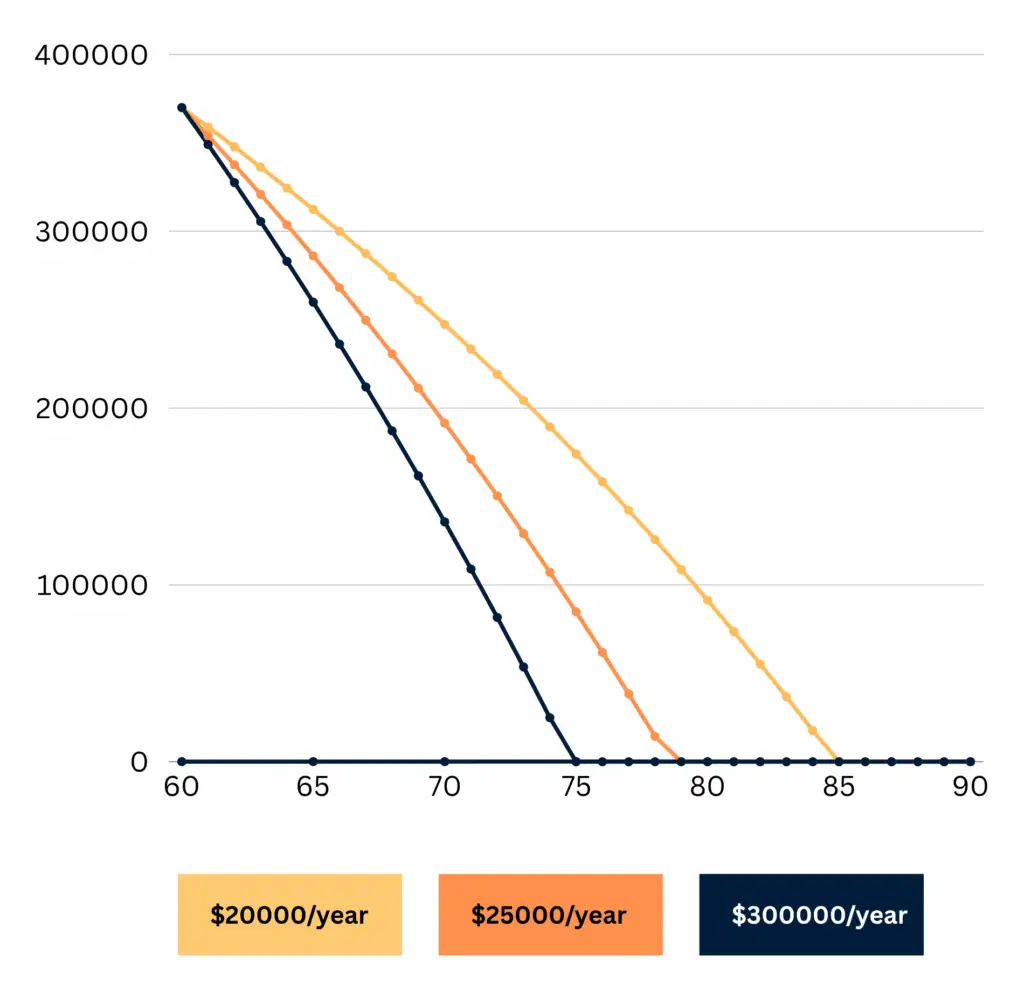

This Line Chart Track how $370K depletes from age 60 to 90 at $20K, $25K, and $30K annual spending levels.

How Much Do You Need to Retire in Australia at 60? What $370K Funds

$370,000 in super at 60 is a real, workable retirement starting point for a single homeowner with modest spending expectations. Here is the honest picture.

What $370K supports: A single homeowner spending $30,000 to $33,000 a year can manage the seven-year gap to the Age Pension comfortably and arrive at 67 with a meaningful balance intact. That is below ASFA’s modest standard of $35,199, but for homeowners without debt whose actual spending is lower than the benchmark, it is genuinely achievable.

What $370K does not support: A comfortable ASFA-standard retirement at $54,000 a year is not sustainable from $370K at 60 without significant other assets or continued income. Spending at $40,000 to $45,000 a year from a $370K base puts real pressure on the balance before the Age Pension arrives.

Please note: All figures in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

What the Numbers Look Like: $370K at 60

Projection assuming an account-based pension with 5% net annual return:

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 60 | $370,000 | $30,000 | $17,000 | $357,000 |

| 61 | $357,000 | $30,500 | $16,325 | $342,825 |

| 62 | $342,825 | $31,000 | $15,591 | $327,416 |

| 63 | $327,416 | $31,500 | $14,796 | $310,712 |

| 64 | $310,712 | $32,000 | $13,936 | $292,648 |

| 65 | $292,648 | $32,000 | $13,032 | $273,680 |

| 66 | $273,680 | $32,000 | $12,084 | $253,764 |

| 67 | $253,764 | Pension starts | ~$234,000 |

At 67, approximately $234,000 remains and the Age Pension begins. For a single homeowner, this falls well under the full pension assets test threshold of around $314,000 (current as at May 2026, Services Australia), meaning near-full pension entitlements of approximately $29,754 a year.

Combined income from 67: near-full pension plus modest drawdown from $234,000 puts annual income in the range of $37,000 to $43,000. For a homeowner with no debt, that is a comfortable and sustainable position through the 70s and 80s.

How Much to Retire at 60: A Practical Budget at $370K

A sample $31,000 annual budget for a single homeowner retiring at 60:

| Category | Annual spend |

|---|---|

| Groceries and food | $8,500 |

| Housing costs, rates and insurance | $5,500 |

| Healthcare and Medicare gap costs | $5,000 |

| Transport and vehicle running costs | $4,500 |

| Domestic travel and leisure | $4,000 |

| Utilities, phone and subscriptions | $2,500 |

| Dining out and social activities | $1,000 |

This sits just below ASFA’s modest standard of $35,199 for a single homeowner but reflects a realistic spending pattern for many Australians who own their home outright, have no commuting costs and have paid off consumer debt. Most retirees find their actual spending is lower than benchmark figures suggest in the early years.

Retiring at 60 in Australia: The Age Pension Picture

Current Age Pension rates as at May 2026 (Services Australia):

- Single (including supplements): approximately $29,754 a year

- Couple combined (including supplements): approximately $44,856 a year

Updated each March and September.

The Age Pension is not automatic. You need to apply through Centrelink and pass both the assets test and the income test. For a single homeowner arriving at 67 with around $234,000, the full pension assets test threshold of $314,000 means near-full entitlements from day one. That $29,754 covers the majority of a modest single retirement lifestyle, leaving your remaining super to fund discretionary spending.

Phil and Dan covered the assets test mechanics, income test thresholds and how super balances translate to actual pension entitlements with real case studies in Episode 10 of the Wealthlab Podcast. Watch Episode 10 on YouTube.

Our pension and Centrelink page covers the application process and how to structure assets to maximise entitlements.

How Much Super Do You Need to Retire at Different Spending Levels?

The question “how much super do I need to retire” has no single answer. Here is the practical range for a single homeowner retiring at 60 with a 5% net return and a full Age Pension from 67:

| Annual spending | Super needed at 60 | Age Pension from 67 |

|---|---|---|

| $28,000 | $280,000–$320,000 | Near full |

| $32,000 | $350,000–$400,000 | Near full |

| $40,000 | $500,000–$560,000 | Part pension |

| $50,000 | $620,000–$700,000 | Part pension initially |

| $55,000 | $680,000–$770,000 | Part pension initially |

These are general ranges. The lower end applies where returns are closer to 6%, the upper end where returns average 4.5%. Individual circumstances vary.

How Much Should I Save for Retirement? Boosting $370K Before You Stop Work

If $370K is your current balance and you have one to three years left before retiring, several strategies can meaningfully improve your position.

Salary sacrifice into super reduces your taxable income while growing your balance. Contributions are taxed at 15% rather than your marginal rate, which is often 32.5% or higher. Even $10,000 to $20,000 a year in extra contributions before you retire makes a significant difference.

Catch-up concessional contributions allow you to use unused concessional cap from the previous five financial years if your total super balance is under $500,000. This can let you contribute substantially more than the standard $30,000 cap in a single year. The rules and a worked example are covered in Episode 10 of the podcast.

Downsizer contributions allow homeowners aged 55 or older who have owned their home for at least 10 years to contribute up to $300,000 per person ($600,000 for a couple) into super from the proceeds of a home sale. This is separate from the standard contribution caps. Our superannuation page has more detail on all of these.

The free Wealthlab super calculator models how different contribution levels and spending scenarios affect your retirement balance.

Mortgage, Debt and Retiring at 60

“Mortgage loan” is appearing as a search query for this page, and for good reason. Carrying a mortgage into retirement at 60 changes the picture significantly.

If you have $370K in super but still owe $200,000 on your home, the calculations above do not apply. Your housing cost is no longer zero and your super may not stretch as far. Whether to pay off the mortgage before retiring, use super to clear it at 60, or carry it into retirement depends on your interest rate, remaining balance, and pension-phase tax treatment.

Scott and Phil addressed this directly in Episode 5 of the Wealthlab Podcast. The spreadsheet says keep the super invested if returns are higher than the mortgage rate, but the emotional reality of debt-free retirement also matters. Watch Episode 5 here.

Transition to Retirement: If You Are Not Quite Ready to Stop

“Transition to retirement” is among the queries appearing for this page. For people approaching 60 who want to reduce hours rather than stop entirely, a TTR pension allows you to draw up to 10% of your super balance per year from age 60 while still working.

A TTR strategy typically works best when combined with salary sacrifice: you sacrifice pre-tax income into super (taxed at 15%) and replace the lost take-home pay by drawing from your TTR pension. This can reduce your tax bill while growing your super faster in the final working years.

The full TTR mechanics, which funds offer the best options, and when a TTR makes sense versus when it does not, are covered in the Wealthlab TTR strategy guide. Episode 18 covers the rules in practical terms. Watch Episode 18 here.

Retiring at 60: How Long Will $370K Last?

This depends heavily on spending and investment returns. At 5% net return:

| Annual spending | Balance at 67 (est.) | Age Pension | Income from 67 |

|---|---|---|---|

| $28,000 | ~$254,000 | Near full ($29,754) | $38,000–$44,000 |

| $32,000 | ~$207,000 | Full ($29,754) | $35,000–$40,000 |

| $40,000 | ~$92,000 | Full ($29,754) | $32,000–$35,000 |

At $40,000 annual spending from a $370K base, the balance is largely drawn down by 67 and the retirement becomes heavily pension-reliant from that point. This is workable for a homeowner but leaves very little buffer for healthcare costs or unexpected expenses in the 70s and 80s. Keeping spending closer to $30,000 to $32,000 in the early years preserves significantly more capital and financial flexibility.

What to Do Before You Retire at 60

Review your investment option. Switching to cash at retirement is one of the most common ways to undermine a solid balance. With 25 to 30 years ahead, a balanced or growth option maintains purchasing power in ways cash cannot. Scott made this case with real numbers comparing a growth portfolio to a conservative one in Episode 1. Watch it here.

Set up an account-based pension. This converts super into a regular, tax-free income stream while keeping the balance invested. Draw above the minimum (4% at ages 60 to 64) deliberately, not reactively.

Plan your Age Pension position. How your super and other assets are structured in the years before 67 affects your entitlements from day one. Structuring this before pension age rather than reacting at application time is one of the highest-value moves at this balance level. Episode 9 of the podcast covers a real case where super fund advice caused an avoidable Age Pension loss. Watch it here.

Build a cash buffer. One to two years of spending outside your pension account protects against being forced to sell growth assets during a market dip in the early retirement years.

FAQ: Retiring at 60 in Australia

Can I retire at 60 in Australia? Yes. Super is accessible tax-free from age 60 for anyone born after 1 July 1964 who has retired from the workforce. There is no legal minimum retirement age. The practical challenge is the seven-year gap before the Age Pension starts at 67.

Can I retire at 60 with $370K in Australia? For a single homeowner spending around $30,000 to $33,000 a year, yes. $370K at 5% net return leaves approximately $234,000 at age 67 when the Age Pension begins, providing near-full pension entitlements of around $29,754. Combined income from 67 is in the range of $37,000 to $43,000.

How much super should I have at 60? For a modest lifestyle ($32,000–$35,000 a year), $330,000 to $450,000 at 60 is workable for a single homeowner. For a comfortable lifestyle ($50,000–$54,000 a year), $550,000 to $700,000. For couples, significantly more. ASFA’s 2026 benchmarks assume retirement at 67; retiring at 60 requires more.

How much super do you need to retire at 60 in Australia? There is no single answer, but as a guide: a single homeowner spending $30,000 a year needs around $330,000 to $380,000. Spending $40,000 a year needs around $500,000 to $560,000. Couples need more in combined terms. The Age Pension from 67 makes lower balances workable for homeowners.

What is the retirement age in Australia? There is no single official retirement age. Super becomes accessible at age 60 (preservation age) for anyone born after 1 July 1964. The Age Pension starts at 67. There is no mandatory retirement age for most occupations.

How much do you need to retire in Australia? ASFA estimates $630,000 for a single homeowner comfortable retirement and $690,000 to $730,000 for a couple, both assuming retirement at 67. Retiring at 60 requires more. A modest lifestyle for a single homeowner at 60 is achievable from around $330,000 to $400,000, with the Age Pension supplementing from 67.

What is the Age Pension rate in 2026? Approximately $29,754 a year for a single person including supplements, and $44,856 combined for a couple. Updated each March and September. Check current rates at Services Australia.

Should I pay off my mortgage before retiring at 60? Generally yes if you have a choice. The projections above assume zero housing costs. Carrying a mortgage into retirement significantly increases annual spending and reduces how long $370K (or any balance) lasts. Even working an extra 12 months to clear a mortgage before retiring often produces a better outcome than retiring with debt intact.

Can you retire at 60 with $500K in Australia? Yes, with more comfort than $370K. At $30,000 to $35,000 a year spending, $500K arrives at 67 with around $330,000 to $360,000 remaining. This is above the full pension threshold, meaning a part pension initially. More buffer for unexpected costs than $370K, but the planning principles are identical.

What happens to my super when I retire at 60? You can convert it to an account-based pension providing regular tax-free income, take a lump sum, or a combination. In pension phase after 60, fund earnings become tax-free. Minimum drawdown rates apply (4% at ages 60 to 64). See our superannuation page for the full access rules.

What to Do Next

If you are approaching 60 and wondering whether retirement is within reach, the clearest step is to model your specific numbers: your balance, your expected spending, your housing situation and your Age Pension position at 67. General benchmarks are useful context. What matters is whether your individual situation adds up.

Take the free Wealthlab retirement quiz for a general snapshot of your retirement readiness. Or book a free, no-pressure chat with the Wealthlab team to run through your specific position with someone who does this every day.