$430,000 in super at 60 puts you above the median Australian retirement balance. Most Australians retire with less. That is the good news. The honest news is that $430K at 60 sits below ASFA’s comfortable retirement benchmark and requires a clear plan to support a genuinely comfortable lifestyle through the seven-year gap before the Age Pension starts at 67.

This article shows you exactly what $430K funds, what the numbers look like year by year, what the Age Pension adds from 67, and what the difference is between a retirement that works and one that runs tight.

Is $430K Enough to Retire at 60 in Australia?

For a single homeowner spending $34,000 to $38,000 a year, yes. $430K in an account-based pension at 5% net return can bridge the seven-year gap to the Age Pension at 67 and arrive there with a meaningful balance intact. That sits between ASFA’s modest standard of $35,199 and their comfortable standard of $54,240 for a single homeowner, not budget retirement, but not quite the full comfortable standard either.

For couples, $430K combined is tight. ASFA’s modest couple standard is $50,866 a year, and sustaining that from $430K combined through a seven-year gap is very challenging. A couple at this combined balance generally benefits from one partner continuing to work part-time into their early 60s.

According to the ASFA Retirement Standard (February 2026 update):

- Single homeowner, modest lifestyle: $35,199 a year

- Single homeowner, comfortable lifestyle: $54,240 a year

- Couple homeowners, modest lifestyle: $50,866 a year

- Couple homeowners, comfortable lifestyle: $77,375 a year

Please note: All figures in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

What the Numbers Look Like: $430K at 60

Projection assuming an account-based pension with 5% net annual return:

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 60 | $430,000 | $34,000 | $19,800 | $415,800 |

| 61 | $415,800 | $34,500 | $19,065 | $400,365 |

| 62 | $400,365 | $35,000 | $18,268 | $383,633 |

| 63 | $383,633 | $35,500 | $17,407 | $365,540 |

| 64 | $365,540 | $36,000 | $16,477 | $346,017 |

| 65 | $346,017 | $36,000 | $15,501 | $325,518 |

| 66 | $325,518 | $36,000 | $14,476 | $303,994 |

| 67 | $303,994 | Pension starts | ~$283,000 |

At 67, approximately $283,000 remains and the Age Pension begins. For a single homeowner, this balance falls comfortably below the full pension assets test threshold of around $314,000 (current as at May 2026, Services Australia), meaning near-full pension entitlements of approximately $29,754 a year.

Combined income from 67: near-full pension plus modest drawdown from $283,000 puts annual income in the range of $38,000 to $46,000. For a homeowner with no debt, that is a comfortable and sustainable retirement income through the 70s and 80s.

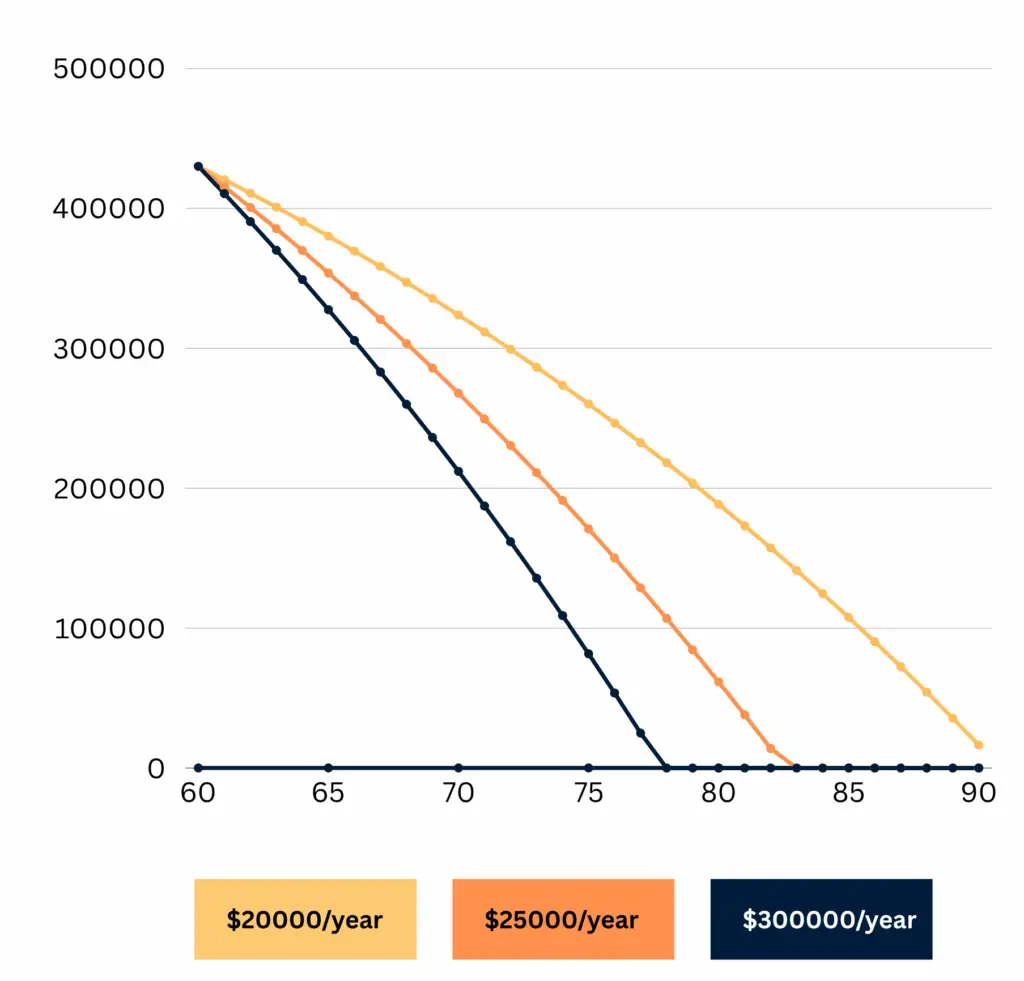

This Line Chart Shows Depletion of $430K from age 60 to 90 under annual spending levels of $20K, $25K, and $30K.

How $430K Compares to the Average Australian Retirement Balance

$430K is above the median super balance for Australians at this age by a meaningful margin. APRA data shows the median balance for men aged 60 to 64 is approximately $302,000, and for women approximately $211,000. A $430K balance puts a single person well above both figures.

That context matters. The anxiety many people feel about their super balance is often calibrated against ASFA’s benchmark figures, which represent a comfortable, not average, retirement. Most Australians retire on significantly less than $430K and manage, partly because the Age Pension is specifically designed to support people in this position.

What $430K does not do is meet ASFA’s comfortable standard of $630,000 for a single person at 67. Retiring seven years earlier with $430K is a different calculation again. The post that owns the comfortable retirement threshold in this cluster is at $510K. At $430K, the honest position is: above average, below comfortable, requires a plan.

A Real Budget for $430K at 60

A sample $35,500 annual budget for a single homeowner:

| Category | Annual spend |

|---|---|

| Groceries and food | $9,500 |

| Housing costs, rates and insurance | $6,000 |

| Healthcare and out-of-pocket costs | $6,500 |

| Transport and vehicle running costs | $5,000 |

| Domestic travel and leisure | $5,000 |

| Utilities, phone and subscriptions | $2,500 |

| Dining out and social activities | $1,000 |

This sits just at ASFA’s modest standard and reflects a comfortable, active lifestyle for a homeowner who owns their home outright, has no commuting costs and has paid off consumer debt. It is not a constrained existence. It is a reasonable, practical retirement budget for someone who owns their home.

The Age Pension from 67: What Changes

Current Age Pension rates as at May 2026 (Services Australia):

- Single (including supplements): approximately $29,754 a year

- Couple combined (including supplements): approximately $44,856 a year

Updated each March and September by the Australian Government.m

Arriving at 67 with approximately $283,000 remaining, a single homeowner qualifies for near-full Age Pension entitlements from day one. That $29,754 a year covers the majority of a modest retirement lifestyle on its own. Combined with drawdown from the remaining $283,000 at a conservative 3% to 4% rate, total income from 67 is in the range of $38,000 to $40,000 a year, a genuinely comfortable position for a homeowner with no debt.

This is where the Age Pension’s real value becomes clear. For a retiree at $430K who spent the gap years carefully, the financial position at 67 is far stronger than it might look at 60. Phil and Dan walked through how the assets test and income test work in practice with real case studies in Episode 10 of the Wealthlab Podcast. Watch Episode 10 on YouTube.

Our pension and Centrelink page covers the application process, test thresholds and how to structure assets for maximum entitlements.

What Makes the Difference Between $430K Working and Running Tight

Owning your home. Every projection above assumes zero housing costs. With rent or a mortgage, a $430K base becomes very difficult to sustain from 60 to 67 at any reasonable lifestyle level. The single biggest factor at this balance is home ownership.

Spending conservatively in the gap years. Drawing $40,000 to $45,000 a year from $430K in the first few years of retirement is a meaningful risk. It reduces the balance at 67 below the full pension threshold, increases drawdown reliance and leaves less buffer for unexpected costs in the 70s and 80s. Keeping spending around $34,000 to $37,000 in the gap years preserves significantly more capital.

Keeping growth in your investment mix. A $430K retiree moving everything to cash at 60 loses ground to inflation every year before any withdrawals. A balanced investment mix at 5% keeps the balance working between drawdowns. Scott covered the compounding impact of this decision directly in Episode 1 of the Wealthlab Podcast. Watch Episode 1 here.

Planning the Age Pension before 67, not after. How your super and other assets are structured at pension age determines your entitlements from day one. Arriving at 67 with $283,000 in a well-structured pension account is a different position from arriving with the same amount in a poorly structured one. Episode 9 covers a real case where super fund advice caused an avoidable Age Pension loss. Watch Episode 9 here.

Not taking large lump sums early. A kitchen renovation or a significant overseas trip in year one or two of retirement is understandable but costly from a $430K base. Large early withdrawals compound into a materially weaker position at 67.

The free Wealthlab super calculator models how different spending levels and growth assumptions affect your specific balance through the gap years.

Retiring at 60 vs 62 vs 65 with $430K

The age you stop working has a large impact on how $430K performs. This comparison is worth understanding before you decide.

Retiring at 60 with $430K. The scenario above. Seven-year gap, arriving at 67 with approximately $283,000, near-full pension, combined income $38,000 to $46,000 from 67.

Retiring at 62 with $430K as the starting point. Two more years of employer contributions (roughly $16,000 at 11.5% on a $70,000 salary) plus compounding grows the opening retirement balance to approximately $490,000 to $510,000. Five-year gap instead of seven. Arriving at 67 with a meaningfully larger balance and more spending room throughout. The difference in retirement comfort between $430K at 60 and ~$500K at 62 is significant.

Retiring at 65 with $430K as the starting point. Five more years grows the balance to approximately $570,000 to $620,000. Only a two-year gap before the Age Pension. Spending at $42,000 to $45,000 a year becomes straightforwardly sustainable. For anyone who can work to 65 from this balance, the financial improvement is substantial.

The psychology of this decision matters as much as the maths. Phil addressed it in Episode 5 of the Wealthlab Podcast: the spreadsheet says one thing, but living, breathing people with emotions say another. Both are real. Watch Episode 5 here.

Boosting $430K Before You Retire

If retirement is still one to three years away and your current balance is around $430K, there are several moves worth considering.

Salary sacrifice into super reduces taxable income and grows your balance simultaneously. At a 32.5% marginal tax rate, contributing $15,000 to $20,000 pre-tax into super saves $2,625 to $3,500 in annual tax.

Catch-up concessional contributions allow you to use unused concessional cap from the previous five financial years if your total super balance is under $500,000. This can allow contributions significantly above the standard $30,000 annual cap in a single year, both boosting the balance and reducing tax in a high-income final working year. The rules and a worked example are in Episode 10 of the podcast.

Check your investment option now. Many people approaching retirement have their super in a default option that was never reviewed. Understanding what you actually hold inside your fund and whether the allocation suits a drawdown phase is a basic step that many skip. Our superannuation page covers investment options and pre-retirement strategy.

FAQ: Retiring at 60 with $430K in Australia

Can I retire at 60 with $430K in Australia? For a single homeowner spending $34,000 to $37,000 a year, yes. At 5% net return, $430K leaves approximately $283,000 at 67 when the Age Pension begins, with near-full pension entitlements of around $29,754. Combined income from 67 is in the range of $38,000 to $46,000. Above average starting position, below the ASFA comfortable benchmark, workable with a clear plan.

How long will $430K last from age 60? At $34,000 to $36,000 annual spending and 5% net return, $430K arrives at 67 with approximately $283,000 remaining. With near-full Age Pension from 67 reducing drawdown reliance, combined income sustains a homeowner comfortably into the mid to late 80s.

Is $430K above average for retirement in Australia? Yes, meaningfully. The median super balance for men aged 60 to 64 is approximately $302,000 and for women approximately $211,000. $430K is above both medians. It is below ASFA’s comfortable benchmark of $630,000 for singles at age 67, but well above what most Australians retire with.

Will I qualify for the full Age Pension with $430K at 60? Almost certainly by 67. Drawing down at $34,000 to $36,000 a year from $430K over seven years typically leaves approximately $280,000 to $300,000 at 67, below the full pension assets test threshold of $314,000 for a single homeowner (May 2026). Near-full pension entitlements from day one at 67.

What lifestyle does $430K support at 60? Between ASFA’s modest and comfortable standards for a single homeowner. Real spending of $35,000 to $38,000 a year covers all essentials, healthcare, a car, regular domestic travel and modest social spending. Comfortable but not lavish. For a homeowner without debt, genuinely manageable.

Is it better to retire at 60 or wait until 62 with $430K? Two more years from $430K adds approximately $55,000 to $70,000 to your balance through contributions and compounding, and reduces the self-funding gap from seven years to five. The difference in retirement comfort and Age Pension position at 67 is meaningful. Whether the extra years are worth it is personal, but the financial case for waiting is clear.

Is $430K enough for a couple to retire at 60? As a combined balance, very tight. ASFA’s modest lifestyle standard for a couple is $50,866 a year, and bridging seven years on $430K combined at that spending level depletes the balance significantly before the Age Pension arrives. One partner continuing to work part-time into the early 60s makes the outcome substantially more comfortable.

What is the Age Pension for a single person in 2026? Approximately $29,754 a year including supplements, as at May 2026. Updated each March and September. Current rates at Services Australia.

What to Do Next

At $430K you are above average, but the gap between a retirement that works and one that runs tight comes down to structure: spending discipline in the gap years, investment mix, Age Pension positioning and whether you take any large lump sums early. Getting those decisions right before you retire is meaningfully more valuable than getting them right two years in.

Not sure where your retirement position stands? Take the free Wealthlab retirement quiz for a general read. Or book a free, no-pressure chat with the Wealthlab team to talk through your specific numbers.