$510,000 in super at 60 puts you above the median Australian retirement balance and within genuine reach of a comfortable retirement. Not just a workable one. Not just surviving on $28,000 a year until the pension kicks in. A retirement with private health cover, domestic travel, social spending and real breathing room.

Whether $510K actually delivers that depends on three things: your spending level, whether you own your home, and how the money is invested through the seven-year gap before the Age Pension starts at 67. This article runs through all of it with real numbers.

Is $510K Enough to Retire Comfortably at 60?

For a single homeowner spending around $45,000 to $50,000 a year, yes. $510K sits just below ASFA’s comfortable retirement benchmark of $630,000 for singles at age 67, but that benchmark assumes retiring at 67, not 60. Retiring seven years earlier with $510K is a different calculation, and it still works at the right spending level.

The honest read: $510K at 60 comfortably funds a lifestyle between ASFA’s modest standard of $35,199 a year and the comfortable standard of $54,240 a year. For most homeowners, that middle ground covers everything that matters: healthcare, a decent car, regular domestic travel, eating out and genuine leisure. It is not the ASFA comfortable standard in full, but for many people it is the retirement they actually want.

For couples, $510K as a combined balance is tighter. ASFA’s comfortable standard for couples is $77,375 a year. A couple relying on $510K combined would need to spend more conservatively, around $45,000 to $50,000 together, or delay retirement until a higher combined balance is reached.

What the Numbers Look Like: $510K at 60

Projection assuming an account-based pension with 5% net annual return:

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 60 | $510,000 | $45,000 | $23,250 | $488,250 |

| 61 | $488,250 | $45,000 | $22,163 | $465,413 |

| 62 | $465,413 | $45,500 | $20,995 | $440,908 |

| 63 | $440,908 | $46,000 | $19,745 | $414,653 |

| 64 | $414,653 | $46,500 | $18,408 | $386,561 |

| 65 | $386,561 | $47,000 | $16,978 | $356,539 |

| 66 | $356,539 | $47,500 | $15,452 | $324,491 |

| 67 | $324,491 | Pension starts | ~$300,000 |

At 67, approximately $300,000 remains and the Age Pension begins. For a single homeowner, the full pension assets test threshold is around $314,000 (current as at May 2026, Services Australia). At $300,000 you are right at or just below that threshold, meaning near-full pension entitlements.

Combined income from 67: approximately $29,754 a year in Age Pension plus modest ongoing drawdown from $300,000, bringing total annual income to around $42,000 to $50,000. That comfortably sustains the lifestyle for a homeowner well into the 80s.

Please note: All figures are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

What a Comfortable Retirement at $510K Actually Looks Like

According to the ASFA Retirement Standard (February 2026 update):

- Single homeowner, modest lifestyle: $35,199 a year

- Single homeowner, comfortable lifestyle: $54,240 a year

- Couple homeowners, modest lifestyle: $50,866 a year

- Couple homeowners, comfortable lifestyle: $77,375 a year

At $45,000 to $47,000 a year spending, a single homeowner at this balance is living between the two ASFA standards. In practical terms, that looks like:

A sample $46,000 annual budget:

| Category | Annual spend |

|---|---|

| Groceries and food | $9,000 |

| Housing costs, rates and insurance | $6,000 |

| Healthcare and private health cover | $8,000 |

| Transport and vehicle | $5,000 |

| Domestic travel and holidays | $10,000 |

| Dining out and social activities | $4,000 |

| Utilities, phone and subscriptions | $3,500 |

| Contingency and personal | $500 |

This is not a budget that requires sacrifice. For most Australians who own their home outright and have paid off consumer debt, this is a genuinely comfortable life.

What Lifestyle Can $510K Support?

With careful budgeting, retiring at 60 with $510K can still allow for:

- Essential household costs (utilities, food, and insurance)

- Basic healthcare expenses

- Transport or vehicle upkeep

- Modest domestic travel

- Dining out, hobbies, and leisure activities

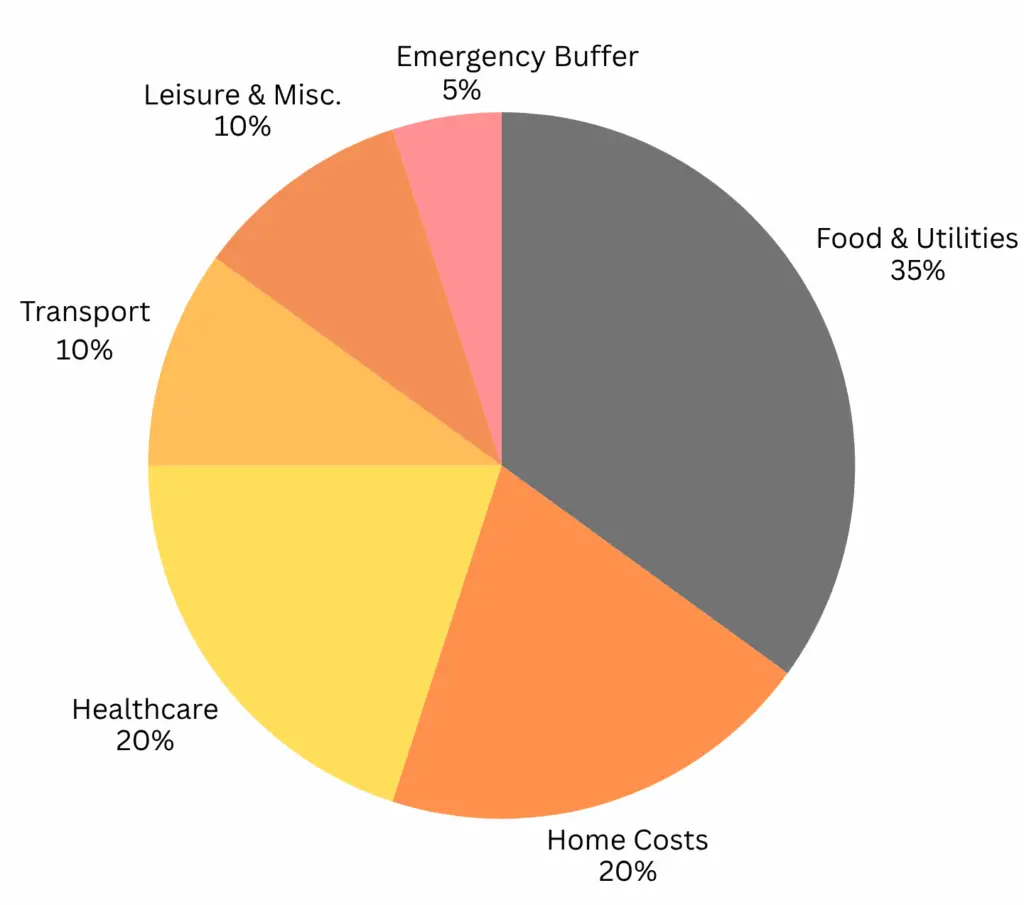

Suggested Budget Breakdown (for $30K/year)

| Category | % of Budget |

|---|---|

| Food & Utilities | 30% |

| Housing Costs | 20% |

| Healthcare | 20% |

| Transport | 10% |

| Leisure & Travel | 15% |

| Contingency/Emergencies | 5% |

How Retirement Age Changes Everything at $510K

The age you stop work is the single biggest lever on how well $510K performs. This comparison is worth sitting with before you decide.

Retiring at 60 with $510K

The standard scenario above. Seven-year gap to the Age Pension, drawing around $45,000 to $47,000 a year, arriving at 67 with approximately $300,000. Near-full pension entitlements from 67, combined income around $42,000 to $50,000 continuing for the long term.

Retiring at 62 with $510K

Two extra years of work means two more years of employer contributions (roughly $16,000 on a $70,000 salary at 11.5%) and two more years of compounding on the existing balance. Starting balance at 62 could be closer to $570,000 to $590,000. The self-funding gap drops from seven years to five. Arriving at 67 with considerably more, and spending capacity goes up meaningfully.

Retiring at 65 with $510K

If $510K is your balance today at 60 and you work until 65, your balance at retirement could be $650,000 to $700,000 depending on returns and contributions. Only two years to bridge before the Age Pension starts. Combined income from 67 could be $50,000 to $60,000 a year with substantially less pressure on your balance. The maths strongly favours the extra years if you are in reasonable health and can manage it.

Scott and Phil discussed the psychology and the numbers on this directly in Episode 19 of the Wealthlab Podcast. Retiring one year earlier than planned can push a retirement from funded to running out at 79 on similar balances. With $510K the same dynamic applies, just with more buffer. Watch Episode 19 on YouTube.

Retiring at 55 with $510K

Difficult without substantial assets outside super. Super cannot be accessed until 60, so five years of living costs must come from elsewhere before your super is even available. The gap to the Age Pension extends to twelve years. Not impossible, but it requires detailed planning around non-super savings and disciplined spending through those early years.

The Seven-Year Gap: What to Watch

The years from 60 to 67 are the most financially critical in early retirement. The decisions made in this period, how much you spend, how your money is invested, and whether you take any large lump sums, have an outsized impact on everything that follows.

Sequencing risk matters here. A sharp market fall in the first two to three years of retirement, when your balance is at its highest and you are drawing regularly, can significantly worsen long-term outcomes compared to the same fall a decade later. Keeping one to two years of spending in cash outside your pension account means you are not forced to sell growth assets at a low point to fund day-to-day costs.

Staying invested for growth is more important than most people realise. It is tempting to move everything to cash at 60. It feels safe. But with 25 to 30 years of retirement ahead, inflation at 3% a year means a cash-heavy portfolio loses real purchasing power every year even before withdrawals are made. In Episode 1 of the Wealthlab Podcast, Scott and Phil compared a growth portfolio to a conservative one over a long retirement with identical spending. The growth portfolio funded the couple to their late 90s. The conservative one ran out 15 years earlier.

Large early withdrawals compound into a problem. An early renovation, a trip to Europe, a lump sum to help the kids. These are all understandable in year one of retirement, but from a base of $510K, pulling $60,000 to $80,000 in the first year or two meaningfully changes your position at 67 and your Age Pension eligibility.

The Age Pension at 67: What Changes

The Age Pension starts at 67 for anyone born on or after 1 January 1957. You need to apply through Centrelink and pass both assets and income tests.

Current Age Pension rates as at May 2026 (Services Australia):

- Single (including supplements): approximately $29,754 a year

- Couple combined (including supplements): approximately $44,856 a year

These are updated each March and September.

For a single homeowner arriving at 67 with around $300,000 remaining in super, the full pension threshold of roughly $314,000 means very high or full pension entitlements. That $29,754 a year adds a significant floor under your retirement income, dramatically reducing how much you need to draw from super from that point.

How you structure your assets in the two to three years before 67 affects what you receive. Getting advice on this before pension age, not after, is one of the most valuable things you can do at this balance level. Phil and Dan walked through real case studies of this in Episode 10 of the Wealthlab Podcast. Watch Episode 10 on YouTube.

Our pension and Centrelink page covers the assets test, income test and application process in more detail.

Smart Moves to Make Before You Retire

Review your investment option now. The default investment option in many super funds is not designed for a retirement drawdown phase. Understanding what you actually hold inside your fund, and whether the mix suits your retirement needs, is a basic first step that many people do not take until after they retire.

Check for catch-up concessional contributions. If your total super balance is under $500,000, you can contribute more than the standard $30,000 annual concessional cap by using unused cap from the previous five financial years. In your final working years this can both boost your balance and reduce tax on a higher income. The worked example in Episode 10 of the podcast covers exactly this scenario. Watch it here.

Consolidate any multiple super accounts. More than one account means more than one set of fees. Consolidating before you retire is a simple admin step with real compounding benefit over a 25-year retirement.

Understand your Age Pension position before 67. How your super balance, savings and other assets sit at pension age affects your entitlements from day one. Planning this structure in advance, rather than applying reactively, makes a difference. See our superannuation page for more on super strategy in the lead-up to retirement.

Want to see how different spending scenarios affect your specific position? The free Wealthlab super calculator models these in a couple of minutes.

FAQ: Retiring at 60 with $510K in Australia

Can I retire at 60 with $510K in Australia? Yes, comfortably for a single homeowner spending around $45,000 to $50,000 a year. With 5% net returns in an account-based pension, $510K leaves approximately $300,000 at age 67, at which point near-full Age Pension entitlements bring combined annual income to $42,000 to $50,000. This sustains a comfortable retirement for a homeowner well into the 80s.

What lifestyle does $510K support at 60? Between ASFA’s modest and comfortable standards for a single homeowner: all essentials covered, private health insurance, a decent car, regular domestic travel, dining out and meaningful leisure. Roughly $45,000 to $47,000 a year. Not the full ASFA comfortable standard of $54,240, but genuinely comfortable for most homeowners.

How long will $510K last from age 60? At $45,000 to $47,000 annual spending and 5% net return, approximately 21 to 23 years before drawing down significantly. With near-full Age Pension from 67 reducing reliance on super, combined income sustains a homeowner well into the mid to late 80s.

Will I qualify for the Age Pension with $510K at 60? Almost certainly by 67. At $45,000 a year spending from 60, you arrive at 67 with approximately $300,000 remaining, which is at or just below the full pension assets test threshold for a single homeowner of around $314,000 (May 2026). Your home is exempt. The exact entitlement depends on all assets and income at the time of application.

Is $510K above or below average for retirement in Australia? Significantly above the median. APRA data shows the median super balance for men aged 60 to 64 is around $302,000 and for women around $211,000. $510K is well above both medians, though below ASFA’s comfortable retirement benchmark of $630,000 for singles at age 67.

Should I keep working past 60 if I have $510K? The maths supports it if you can manage it. Working to 62 adds roughly $55,000 to $70,000 to your balance through contributions and compounding, reduces the gap to the Age Pension from seven years to five, and meaningfully improves spending comfort throughout retirement. Whether the trade-off is worth it is a personal decision, but the financial case for even two more years is clear.

Is $510K enough for a couple to retire at 60? As a combined balance, it is workable at modest spending levels but below ASFA’s comfortable couple standard of $77,375 a year. A couple spending $45,000 to $50,000 combined from $510K is stretched but manageable, particularly with both qualifying for Age Pension at 67. One partner continuing part-time work through the early 60s significantly improves the outcome.

What is the Age Pension rate for a single person in 2026? Approximately $29,754 a year including supplements, as at May 2026. Updated each March and September. Check current rates at Services Australia.

What to Do Next

If you are approaching 60 with around $510K in super, the most useful thing you can do before you retire is get a clear picture of three things: how the money should be invested during your retirement, what your Age Pension position will look like at 67, and whether an extra year or two of work meaningfully changes your outcome. For most people at this balance, the difference between stopping at 60 and stopping at 62 is large enough to be worth understanding clearly.

Not sure where your retirement stands? take the free Wealthlab retirement quiz for a general read on your position. Or book a free, no-pressure chat with the Wealthlab team to talk through what $510K means for your specific retirement.