$610,000 in super at 60 puts you above ASFA’s comfortable retirement benchmark, well above the median Australian balance for this age group, and in a position where the real question is not whether you can retire. It is what kind of retirement $610K actually buys, what it costs to live comfortably in Australia right now, and how the numbers hold up across a retirement that could easily run 25 to 30 years.

Those are the questions this article answers with real numbers, current figures and honest context.

Is $610K Enough to Retire Comfortably at 60?

Yes, clearly, for a single homeowner. $610K at 60 sits above ASFA’s comfortable retirement benchmark of $630,000 for singles at age 67. You are retiring seven years earlier, which means the balance needs to work harder through the gap to the Age Pension. But at $52,000 to $55,000 a year spending with a balanced investment approach, it gets there comfortably.According to the ASFA Retirement Standard (February 2026 update), annual retirement costs for a homeowner are:

- Single homeowner, comfortable lifestyle: $54,240 a year

- Single homeowner, modest lifestyle: $35,199 a year

- Couple homeowners, comfortable lifestyle: $77,375 a year

- Couple homeowners, modest lifestyle: $50,866 a year

At $52,000 to $54,000 a year, a single homeowner with $610K is living squarely at the ASFA comfortable standard. That covers everything that standard includes: top-level private health insurance, a car with full running costs, annual domestic holidays and one overseas trip every seven years, regular dining out, home maintenance and genuine discretionary spending.

For couples, $610K combined is workable but below ASFA’s comfortable couple standard of $77,375. A couple aiming for genuine comfort at this combined balance would benefit from one partner continuing part-time work through the early 60s.

What Retirement Actually Costs in Australia in 2026

The GSC data for this post tells us clearly that people reading it are also searching for cost of living information. That makes sense. $610K sounds like a lot until you look at what life actually costs.

Here is what retirement spending looks like across three lifestyle levels for a single homeowner in 2026:

| Lifestyle | Annual spend | What it covers |

|---|---|---|

| Modest | $35,000 to $38,000 | Essentials, Medicare, public transport, local activities, limited travel |

| Comfortable | $52,000 to $55,000 | Private health, car, annual domestic holidays, dining out, home maintenance |

| Generous | $70,000 to $80,000 | Regular overseas travel, higher-end dining, car upgrades, gifts to family |

Cost of living in major Australian cities matters. Retirement spending is not the same in Brisbane as it is in Sydney or Melbourne. Housing costs are exempt from the Age Pension assets test if you own your home, but ongoing costs, rates, insurance, maintenance and proximity to services all vary significantly.

As a rough guide for homeowners in 2026:

- Melbourne and Sydney: Higher council rates, body corporate fees if in a unit, higher healthcare costs due to specialist concentration. Comfortable retirement spending trends toward the upper end of the ASFA comfortable range, around $56,000 to $60,000 a year.

- Brisbane and Gold Coast: Slightly lower ongoing housing costs than Sydney/Melbourne, strong healthcare infrastructure, warmer climate reduces some lifestyle costs. Comfortable retirement around $52,000 to $56,000 a year.

- Perth and Adelaide: Generally lower cost of living than east coast capitals. Comfortable retirement spending can track closer to $50,000 to $54,000 a year for homeowners.

- Regional Queensland, regional Victoria, coastal NSW: Lower housing and living costs for homeowners, but potentially higher transport costs and reduced access to specialist healthcare. Many retirees find genuine comfort at $42,000 to $48,000 a year in well-serviced regional areas.

These are general observations based on ABS and ASFA data. Individual circumstances vary considerably.

The cost of living pressure for retirees is real and has tightened in recent years. Insurance premiums, healthcare out-of-pocket costs, council rates and energy prices have all increased faster than general inflation for many retirees. Building a 3% to 4% annual spending increase into your retirement projections, rather than assuming flat costs, gives a more realistic picture of what your super needs to do.

What Happens When You Turn 67?

Once you qualify for the Age Pension, it can provide:

- ~$28,500/year for singles

- ~$43,000/year for couples

This income reduces your need to draw heavily from your super, extending the longevity of your retirement savings and giving you room to handle unexpected expenses, healthcare costs, or lifestyle upgrades.your super, extending the longevity of your retirement savings and giving you room to handle unexpected expenses, healthcare costs, or lifestyle upgrades.

What the Numbers Look Like: $610K at 60

Projection assuming an account-based pension with 5% net annual return:

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 60 | $610,000 | $52,000 | $27,900 | $585,900 |

| 61 | $585,900 | $52,500 | $26,670 | $560,070 |

| 62 | $560,070 | $53,000 | $25,354 | $532,424 |

| 63 | $532,424 | $53,500 | $23,946 | $502,870 |

| 64 | $502,870 | $54,000 | $22,444 | $471,314 |

| 65 | $471,314 | $54,000 | $20,866 | $438,180 |

| 66 | $438,180 | $54,000 | $19,209 | $403,389 |

| 67 | $403,389 | Pension starts | ~$375,000 |

At 67, roughly $375,000 remains and the Age Pension begins. For a single homeowner, this balance sits above the full pension assets test threshold of around $314,000 (current as at May 2026, Services Australia), meaning a part pension initially.

At $375,000, the assets test taper ($3 reduction per $1,000 above the threshold) reduces pension by approximately $183 per fortnight, or roughly $4,758 a year. So the initial Age Pension is approximately $24,996 a year rather than the full $29,754.

As the balance draws down through the early to mid-70s toward the $314,000 full pension threshold, entitlements increase. Once the balance falls below that threshold, the full pension of $29,754 kicks in and the annual drawdown requirement from super drops significantly.

Please note: All figures are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

Age Pension Rates and the Assets Test in 2026

Current Age Pension rates as at May 2026 (Services Australia):

- Single (including supplements): approximately $29,754 a year

- Couple combined (including supplements): approximately $44,856 a year

Updated each March and September by the Australian Government.

The assets test thresholds for homeowners (May 2026):

- Full pension: assets below approximately $314,000 (single homeowner)

- Part pension cut-off: assets above approximately $695,500 (single homeowner)

- The taper reduces pension by $3 per fortnight for every $1,000 of assets above the full pension threshold

At $375,000 in super at 67, a single homeowner receives a part pension and transitions to the full pension as the balance draws down through the 70s. The practical effect: combined income from partial pension plus drawdown is comfortably in the $48,000 to $55,000 range from 67 onwards, sustaining the ASFA comfortable lifestyle well into the 80s.

Phil and Dan worked through the assets test taper with real case studies in Episode 10 of the Wealthlab Podcast, including how different retirement balances translate to specific pension entitlements and when the full pension threshold is reached. Watch Episode 10 on YouTube.

Our pension and Centrelink page covers how to apply, what counts in the assets test and how to structure your affairs before 67.

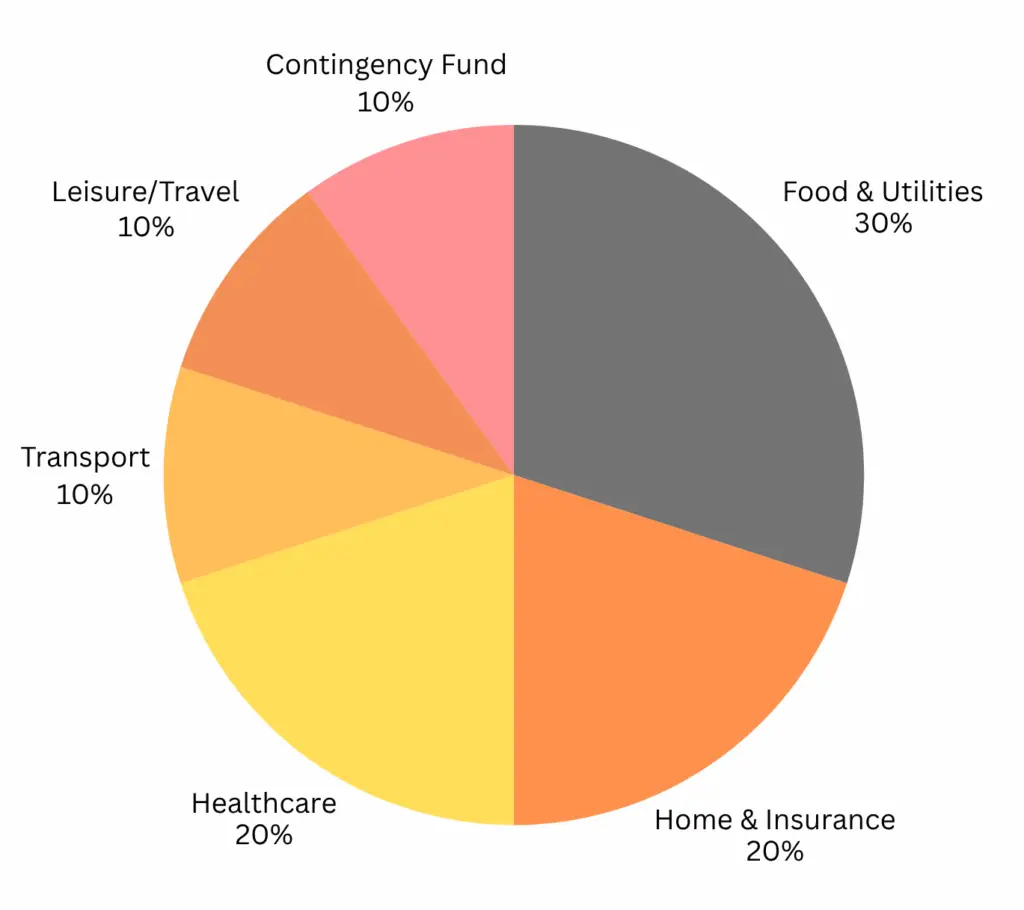

A Real Budget for a Comfortable Retirement at $610K

A sample $54,000 annual budget for a single homeowner in a capital city:

| Category | Annual spend |

|---|---|

| Groceries and food | $11,000 |

| Housing costs, rates and insurance | $7,500 |

| Healthcare and private health cover | $9,000 |

| Transport, vehicle and registration | $6,000 |

| Domestic and international travel | $12,000 |

| Dining out and social activities | $5,000 |

| Utilities, phone and subscriptions | $3,000 |

| Clothing and personal care | $500 |

This matches ASFA’s comfortable standard. The travel allocation reflects ASFA’s assumption of annual domestic holidays and one international trip approximately every seven years. For someone in regional Queensland or coastal NSW, the same lifestyle typically costs $4,000 to $8,000 less per year due to lower housing-related costs.

The Cost of Living Crisis and What It Means for Retirees

“Cost of living crisis” is a real concern for Australians at or approaching retirement. Inflation from 2022 to 2024 ran at rates not seen in a generation, and while headline inflation has moderated, several categories that matter most to retirees remain stubbornly elevated: insurance, healthcare out-of-pocket costs, energy bills and council rates.

For a retiree on a fixed income from super and eventually the Age Pension, this matters more than it does for wage earners who may receive cost-of-living pay adjustments.

The practical response at $610K: two things matter most. First, keeping some growth assets in your investment mix so returns outpace inflation over the long run. Second, building a spending increase assumption into your projections, typically 3% to 3.5% a year, rather than assuming costs stay flat.

Scott addressed this directly in Episode 1 of the Wealthlab Podcast, showing how a conservative or cash-heavy portfolio in retirement quickly falls behind inflation even before drawdowns are factored in, while a growth-oriented portfolio maintains purchasing power over a 25 to 30-year retirement. Watch Episode 1 here.

Where to Retire in Australia: Does Location Matter for $610K?

“Best place to retire in Queensland” and “average living cost in Melbourne” are appearing in the GSC data for this page. They are fair questions for someone at this balance.

The honest answer: location matters less for financial outcomes than most people think, and more for lifestyle and healthcare access than the numbers suggest.

From a pure cost-of-living perspective, retiring to regional Queensland, the Sunshine Coast, regional Victoria or coastal NSW as a homeowner reduces annual spending by $5,000 to $10,000 compared to the Sydney or Melbourne CBD fringe. Over a 25-year retirement, that difference compounds significantly.

From a healthcare access perspective, proximity to specialist medical care, public hospitals and aged care services matters more as you move through your 70s and 80s. Many retirees who move to regional areas for lower costs find themselves relocating back to larger centres when health needs increase.

With $610K, the financial flexibility to retire comfortably in most Australian cities exists. The question of where to retire is genuinely more about lifestyle, proximity to family, climate and community than about whether the balance is sufficient.

What to Do Before You Retire at 60 with $610K

Review your investment option now. The default in many super funds is not optimised for a retirement drawdown phase. Understanding your actual asset allocation and whether it suits 25 to 30 years of retirement is a basic first step.

Consider catch-up concessional contributions if you are still working. At $610K, your balance is above the $500,000 threshold that determines catch-up contribution eligibility. But if your balance was below $500,000 in a recent prior year, unused concessional cap from those years may still be accessible. Worth checking with a financial adviser. The rules are explained with a worked example in Episode 10 of the podcast. Watch it here.

Plan your Age Pension structure before 67, not after. With a balance around $375,000 at 67, your transition from part pension to full pension is gradual. How your assets are structured at pension age affects entitlements from day one. Getting advice on this a year or two before you turn 67 is worth doing. Our superannuation page covers pre-retirement strategy in more detail.

Build a cash buffer before you retire. One to two years of spending in cash outside your pension account protects against being forced to sell growth assets during a market downturn in the early retirement years. Sequencing risk, the impact of poor market returns in the first two to three years of drawdown, is the main structural risk for someone at this balance.

The free Wealthlab super calculator models different spending levels and growth scenarios for your specific balance.

FAQ: Retiring at 60 with $610K in Australia

Can I retire at 60 with $610K in Australia? Yes, comfortably. At $52,000 to $54,000 a year spending and 5% net return, $610K leaves approximately $375,000 at 67 when the Age Pension begins. Part pension initially of around $25,000 a year, building toward full pension as the balance draws down. Combined income from 67 sustains the ASFA comfortable lifestyle well into the 80s.

How much does it cost to live comfortably in retirement in Australia? According to ASFA’s February 2026 standard, a comfortable retirement for a single homeowner costs $54,240 a year. For couples, $77,375. These include private health insurance, a car, domestic travel, dining out and home maintenance. In capital cities the actual figure trends slightly higher; in regional areas slightly lower.

Is $610K above or below the ASFA comfortable benchmark? ASFA’s comfortable benchmark is $630,000 at age 67. At $610K retiring at 60, you are $20,000 below that benchmark and seven years earlier. The gap is small and the balance is above median. For a single homeowner spending around $52,000 to $54,000 a year, $610K at 60 comfortably funds the ASFA comfortable standard throughout retirement.

Will I get the Age Pension with $610K at 60? By 67, at $52,000 to $54,000 annual spending, approximately $375,000 remains. This is above the full pension assets test threshold of $314,000 for a single homeowner, so you receive a part pension initially of around $25,000 a year. As the balance draws down through the early 70s below the threshold, entitlements increase to the full $29,754 a year.

What is the cost of living in Melbourne for retirees? For a single homeowner in Melbourne, a comfortable retirement typically costs $56,000 to $60,000 a year, slightly above the national ASFA standard, due to higher council rates, insurance premiums and cost of living generally. $610K supports this comfortably with appropriate investment returns and Age Pension support from 67.

Is Queensland a good place to retire? For many Australians, yes. Warmer climate, lower housing-related costs compared to Sydney and Melbourne, and a large retiree population with supporting services make Queensland attractive. Comfortable retirement spending in Queensland, particularly the Sunshine Coast, Gold Coast or regional areas, typically runs $48,000 to $54,000 a year for homeowners, which $610K supports well.

How does the cost of living crisis affect retirement planning? Insurance, healthcare out-of-pocket costs, energy and council rates have risen faster than headline inflation in recent years, directly affecting retirees on fixed income. Building a 3% to 3.5% annual spending increase into retirement projections and maintaining some growth assets in your investment mix are the practical responses. A cash-heavy portfolio does not keep pace with real retirement costs over 25 years.

Is $610K enough for a couple to retire at 60? As a combined balance, $610K falls below ASFA’s comfortable couple standard of $77,375 a year. It is workable at more modest spending around $50,000 to $55,000 combined, but a couple aiming for genuine comfort generally benefits from one partner continuing part-time work through the early 60s, or from delaying retirement until a higher combined balance is reached.

What to Do Next

If you are approaching 60 with around $610K in super, the core planning questions are how your money is invested through the seven-year gap, what your actual retirement spending looks like (including how it will change over time), and how to structure your assets to maximise Age Pension entitlements from 67. At this balance, retirement is clearly achievable. The value of good advice is in the structuring, not the numbers.

Not sure where your retirement stands? take the free Wealthlab retirement quiz for a general snapshot. Or book a free, no-pressure chat with the Wealthlab team to talk through your specific situation.