$660,000 in super at 60 puts you above ASFA’s comfortable retirement benchmark and well ahead of the median Australian balance for this age group. The question at this level is not whether you can retire. It is how to structure the retirement you have worked to build so that it stays comfortable for 30 years, maximises your Age Pension entitlements, and does not leave money quietly eroding in the wrong investment option.

That is what this article covers.

The Honest Answer First

Yes, you can retire at 60 with $660K. Clearly and confidently, for most homeowners.

$660K exceeds ASFA’s comfortable retirement benchmark of $630,000 for singles at age 67, and you are retiring seven years earlier. At $52,000 to $55,000 a year spending with a balanced investment approach, $660K supports the full ASFA comfortable standard throughout retirement, including private health insurance, a decent car, annual domestic travel, dining out and genuine discretionary spending. Not a budget retirement. Not a luxury one. A genuinely comfortable, stress-free life.

For couples, $660K combined is workable but below ASFA’s comfortable couple standard of $77,375 a year. A couple in this position generally benefits from one partner continuing to work part-time into their early 60s, or from delaying retirement until a higher combined balance is reached.

What the Numbers Look Like: $660K at 60

Projection assuming an account-based pension with 5% net annual return:

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 60 | $660,000 | $54,000 | $30,300 | $636,300 |

| 61 | $636,300 | $54,000 | $29,115 | $611,415 |

| 62 | $611,415 | $54,500 | $27,846 | $584,761 |

| 63 | $584,761 | $55,000 | $26,488 | $556,249 |

| 64 | $556,249 | $55,000 | $25,062 | $526,311 |

| 65 | $526,311 | $55,000 | $23,566 | $494,877 |

| 66 | $494,877 | $55,000 | $21,994 | $461,871 |

| 67 | $461,871 | Pension starts | ~$430,000 |

At 67, approximately $430,000 remains and the Age Pension begins. For a single homeowner, this balance is above the full pension threshold of around $314,000 (current as at May 2026, Services Australia) but well below the part pension cut-off of approximately $695,500. This means a meaningful part pension from day one at 67.

At $430,000 in super at 67, the assets test taper reduces the full pension ($29,754) by $3 per fortnight for every $1,000 above $314,000. That is $116,000 above the threshold, producing a taper reduction of approximately $348 per fortnight, or $9,048 a year. Initial Age Pension: approximately $20,706 a year.

As the balance draws down through the late 60s and early 70s, pension entitlements increase. Once the balance falls below $314,000, likely in the mid-70s at this spending level, the full pension of $29,754 kicks in. From that point, drawdown requirements from super drop sharply and combined income comfortably sustains the lifestyle into the 80s and beyond.

Please note: All figures are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

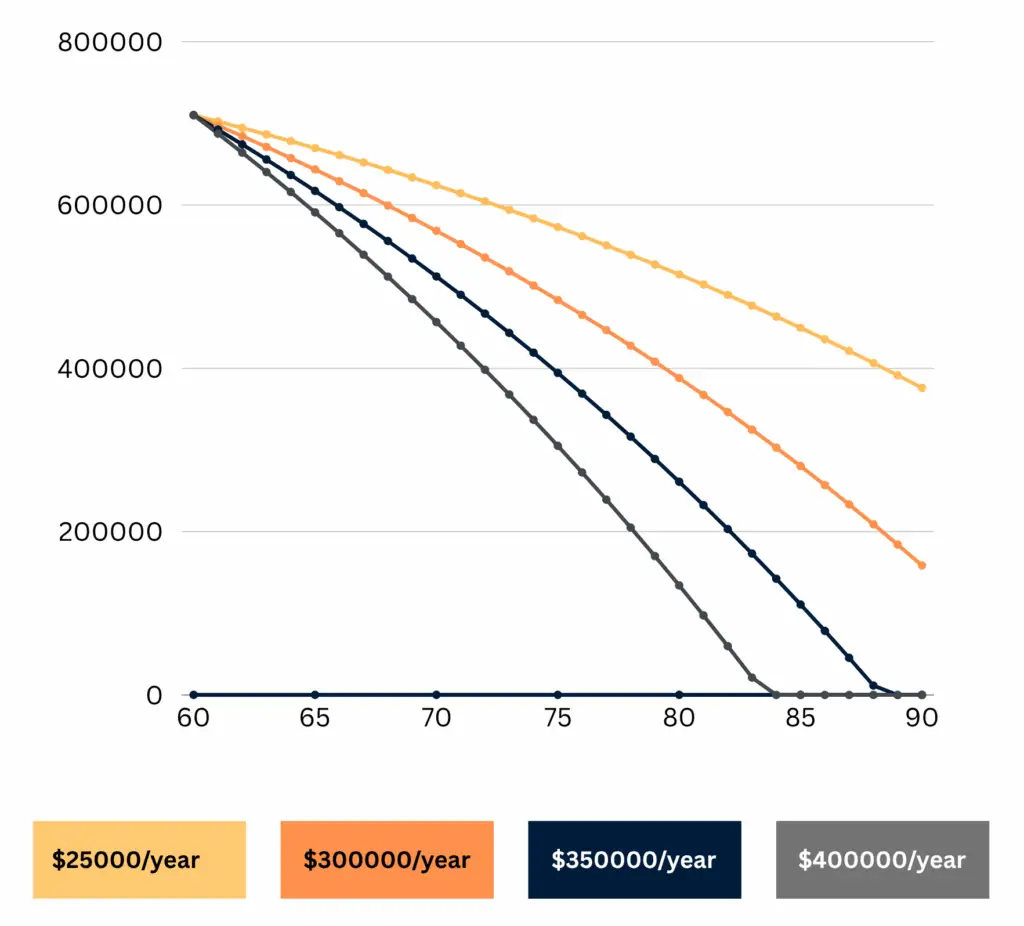

This line chart tracking the decline of $660K from age 60 to 90 under different annual spending levels ($20K, $25K, $30K, $35K) would help illustrate this.

What the ASFA Comfortable Standard Means in Practice

According to the ASFA Retirement Standard (February 2026 update):

- Single homeowner, comfortable lifestyle: $54,240 a year

- Single homeowner, modest lifestyle: $35,199 a year

- Couple homeowners, comfortable lifestyle: $77,375 a year

- Couple homeowners, modest lifestyle: $50,866 a year

At $54,000 to $55,000 a year, a single homeowner with $660K is living squarely at the ASFA comfortable standard. A sample annual budget:

| Category | Annual spend |

|---|---|

| Groceries and food | $11,500 |

| Housing costs, rates and insurance | $7,000 |

| Healthcare and private health cover | $9,000 |

| Transport and vehicle running costs | $5,500 |

| Domestic and international travel | $12,500 |

| Dining out and social activities | $5,500 |

| Utilities, phone and subscriptions | $3,000 |

| Clothing, personal and miscellaneous | $500 |

This is not a constrained budget. It covers top-level private health insurance, a car you can replace when needed, an annual domestic trip and an international trip every few years, regular dining out, and genuine lifestyle freedom. At $660K from 60, this level of spending is sustainable.

The Key Planning Work at This Balance Level

For someone at $660K, the planning questions are different from someone at $300K who is figuring out whether retirement is viable at all. At $660K the retirement is viable. The planning work shifts to optimisation: making sure the money is structured and invested in ways that maximise what you receive over 30 years.

Investment mix through the gap years. A 60-year-old with $660K likely has 30 years of retirement ahead. A conservative or cash-heavy investment option loses ground to inflation every year, eroding the real value of the balance even before drawdowns are counted. A balanced investment option with 60 to 70% growth assets is generally more appropriate and substantially improves long-term outcomes at this time horizon.

Scott and Phil went through this with real case study numbers in Episode 1 of the Wealthlab Podcast. A growth portfolio kept the couple funded into their late 90s. A conservative portfolio on identical spending ran out 15 years earlier. At $660K, the difference between these outcomes is large in absolute dollar terms. Watch Episode 1 on YouTube.

Managing the Age Pension taper deliberately. Arriving at 67 with $430,000 means a part pension of around $20,700 a year. That pension grows toward the full $29,754 as the balance draws down. Understanding this trajectory, and how to manage drawdowns in ways that accelerate the transition to full pension where appropriate, is a core part of retirement optimisation at this balance level.

Phil and Dan covered the assets test taper in detail with real case studies in Episode 10 of the Wealthlab Podcast. Watch Episode 10 on YouTube.

Structuring assets to avoid the part pension zone lingering. Some retirees deliberately draw down more aggressively in their early 70s to get below the full pension threshold sooner, trading a modest reduction in balance for full pension entitlements earlier. Others prefer to draw conservatively and stay in the part pension zone longer. Which approach is better depends on health, spending needs, other assets and personal circumstances. This is not a one-size-fits-all decision and is worth examining with a financial adviser.

Sequencing risk in the first three years. When your balance is at its highest (which it is at $660K on day one of retirement), a significant market fall combined with regular withdrawals has the largest impact on long-term outcomes. Keeping one to two years of spending in cash outside your account-based pension provides a buffer so you are never forced to sell growth assets at a low point.

Renters at $660K: A Different Calculation

If you are renting rather than owning your home, the picture changes. ASFA’s modest lifestyle cost for a single private renter is approximately $49,676 a year, compared to $35,199 for a single homeowner. A comfortable lifestyle for a renter is not separately benchmarked but in practice runs $15,000 to $20,000 higher than for homeowners due to rent costs.

At $660K with $65,000 to $70,000 annual spending to cover rent and comfortable living, the balance draws down significantly faster. You may still receive a part pension at 67, but the combined income is lower and the balance runs down more quickly through the 70s.

$660K at 60 as a renter is workable but requires more careful management than for a homeowner. The downsizer contribution rules are worth understanding for renters who own or have sold a property, as they provide a direct pathway to boost super before retirement.

How the Retirement Age Decision Changes at $660K

Retiring at 60 with $660K. The scenario described in this article. Seven-year gap, arrives at 67 with approximately $430,000, part pension initially building toward full pension through the early 70s. Annual income from 67 sustains the ASFA comfortable standard long-term.

Retiring at 62 with $660K as the starting point. Two more years of contributions (approximately $16,000) and compounding brings the opening retirement balance to around $740,000 to $760,000. The gap to pension age drops to five years. Arriving at 67 with a larger balance, perhaps $510,000 to $520,000, means a smaller initial part pension but significantly more capital providing income flexibility through the late 60s and 70s. Total lifetime income from this position is materially higher.

Retiring at 65 with $660K as the starting point. Five more years grows the balance to roughly $850,000 to $900,000. Only a two-year gap before the Age Pension. Spending at $60,000 to $65,000 a year becomes straightforwardly sustainable. For anyone who can work to 65 from this balance, the financial outcome improvement is significant.

The psychology of this decision was captured well in Episode 5 of the Wealthlab Podcast. The spreadsheet answer and the personal answer are both real, and both matter. Watch Episode 5 here.

Age Pension Rates and Thresholds for 2026

Current Age Pension rates as at May 2026 (Services Australia):

- Single (including supplements): approximately $29,754 a year

- Couple combined (including supplements): approximately $44,856 a year

Full pension assets test threshold for single homeowners: approximately $314,000. Part pension cut-off for single homeowners: approximately $695,500.

Updated each March and September by the Australian Government.

Our pension and Centrelink page covers the application process, how the assets and income tests work and how to structure assets to maximise entitlements.

What to Do Before You Retire at 60 with $660K

Review your investment option before you stop work. The default option in many super funds is not designed for a 30-year retirement drawdown. Understanding what you actually hold inside your fund and whether the allocation is appropriate for your time horizon is a basic first step many people skip.

Set up an account-based pension. This converts your super into a regular, tax-free income stream while keeping the balance invested. Draw above the government minimum (4% at age 60 to 64) but deliberately, not reactively. Having a clear annual spending target before you retire protects against the common pattern of overspending in the first two years.

Build a cash buffer. One to two years of spending in a high-interest savings account or term deposit outside your pension provides the sequencing risk protection described above without requiring you to hold large amounts permanently in cash.

Consider your Age Pension strategy now. The assets and income test at 67 are determined by your position at the time of application, not at retirement. How your assets are structured in the years before 67, whether super versus non-super, account-based pension versus lump sum, affects your entitlements from day one. Getting advice on this two to three years before 67 is meaningfully worthwhile.

Check how your own balance projects at different spending levels using the free Wealthlab super calculator. Our retirement planning page and superannuation page have more on pre-retirement strategy and drawdown structure.

FAQ: Retiring at 60 with $660K in Australia

Can I retire at 60 with $660K in Australia? Yes, comfortably for a single homeowner. At $54,000 to $55,000 annual spending and 5% net return, $660K leaves approximately $430,000 at 67 when the Age Pension begins. Part pension of around $20,700 a year initially, growing toward full pension of $29,754 as the balance draws down through the early 70s. Combined income sustains the ASFA comfortable standard throughout.

Is $660K above the ASFA comfortable retirement benchmark? Yes. ASFA’s comfortable benchmark is $630,000 at age 67. At $660K retiring at 60, you are $30,000 above that benchmark but retiring seven years earlier. The balance is sufficient to sustain the comfortable standard throughout retirement for a single homeowner.

How long will $660K last from age 60? At $54,000 to $55,000 annual spending and 5% net return, the balance draws down to approximately $430,000 by 67. With part Age Pension supplementing income from 67 and transitioning to full pension through the early 70s, combined income sustains the comfortable lifestyle into the mid to late 80s for most homeowners.

What is the Age Pension situation with $660K at 60? By 67, approximately $430,000 remains. Above the full pension threshold of $314,000 for a single homeowner, so a part pension of around $20,700 a year initially. As the balance draws down below $314,000 in the early to mid-70s, entitlements transition to the full $29,754 a year.

What lifestyle does $660K support at 60? The full ASFA comfortable standard for a single homeowner: $54,240 a year covering private health insurance, a car, annual domestic travel, dining out, home maintenance and genuine discretionary spending. Not constrained or budget. A genuinely comfortable, active retirement.

Can I retire at 67 with $400K? Yes, with some care. At $400K at 67, a single homeowner is above the full pension threshold of $314,000, so a part pension initially. Combined income from a $20,000 to $25,000 drawdown plus a part pension of around $20,000 to $25,000 totals $40,000 to $50,000 a year, close to ASFA’s comfortable standard. As the balance draws down below $314,000, full pension entitlements arrive. It is a workable but more constrained position than $660K at 60.

Is $660K enough for a couple to retire at 60? As a combined balance, it is workable at modest to moderate spending but falls below ASFA’s comfortable couple standard of $77,375. A couple targeting genuine comfort would benefit from one partner continuing part-time work through the early 60s or from reaching a combined balance closer to $800,000 to $900,000 before stopping.

What is the preservation age in Australia? 60 for anyone born after 30 June 1964. Once you reach 60 and have retired from the workforce, you can access your super tax-free. The Age Pension eligibility age is 67. There is no single official retirement age in Australia.

What to Do Next

At $660K you have built a strong foundation for retirement. The work now is in the structure: investment mix, drawdown strategy, Age Pension positioning and sequencing risk management. These decisions do not change how much you have, but they meaningfully change how long it lasts and how much you receive from the government along the way.

Not sure how your retirement is structured? or take the free Wealthlab retirement quiz for a general read on your position. Or book a free, no-pressure chat with the Wealthlab team to work through the specifics with someone who does this every day.