$770,000 in super at 60 puts you comfortably above ASFA’s comfortable retirement benchmark and in the top tier of Australian retirement balances at this age. The question at this level is not whether retirement at 60 is viable. It clearly is. The questions that actually matter are: which super fund and investment option should your money be in for retirement, how do you manage the Age Pension taper at 67, and how do you make sure $770K stays comfortable for 30 years rather than running down prematurely through poor structuring.

This article covers all of it.

Is $770K Enough to Retire at 60 in Australia?

Yes, comfortably and clearly, for a single homeowner. $770K is $140,000 above ASFA’s comfortable retirement benchmark of $630,000 for singles at age 67, and you are retiring seven years earlier. At $58,000 to $62,000 a year spending with a balanced investment approach, this balance supports the full ASFA comfortable standard throughout retirement with real breathing room.

According to the ASFA Retirement Standard (February 2026 update):

- Single homeowner, comfortable lifestyle: $54,240 a year

- Single homeowner, modest lifestyle: $35,199 a year

- Couple homeowners, comfortable lifestyle: $77,375 a year

- Couple homeowners, modest lifestyle: $50,866 a year

At $58,000 to $62,000 a year, a single homeowner at $770K is living above the ASFA comfortable standard. That means everything in that standard, including private health insurance, a car, regular domestic travel, occasional international trips and genuine discretionary spending, plus meaningful additional flexibility.

For couples, $770K combined is workable at moderate spending but below ASFA’s comfortable couple standard of $77,375. A couple targeting the full comfortable standard at this combined balance would benefit from one partner continuing part-time work through the early 60s.

What the Numbers Look Like: $770K at 60

Projection assuming an account-based pension with 5% net annual return:

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 60 | $770,000 | $58,000 | $35,600 | $747,600 |

| 61 | $747,600 | $58,500 | $34,455 | $723,555 |

| 62 | $723,555 | $59,000 | $33,228 | $697,783 |

| 63 | $697,783 | $59,500 | $31,914 | $670,197 |

| 64 | $670,197 | $60,000 | $30,510 | $640,707 |

| 65 | $640,707 | $60,000 | $29,035 | $609,742 |

| 66 | $609,742 | $60,000 | $27,487 | $577,229 |

| 67 | $577,229 | Pension starts | ~$540,000 |

At 67, approximately $540,000 remains and the Age Pension begins. For a single homeowner, this is above the full pension threshold of $314,000 and below the part pension cut-off of approximately $695,500 (May 2026, Services Australia). This means a meaningful part pension from day one.

At $540,000 in super at 67, the taper ($3 per fortnight per $1,000 above $314,000) reduces the full pension by approximately $678 per fortnight, or $17,628 a year. Initial Age Pension: approximately $12,126 a year. As the balance draws down through the late 60s and 70s toward the $314,000 threshold, entitlements grow steadily toward the full $29,754.

Combined income from 67: approximately $12,000 to $15,000 in part pension plus $35,000 to $40,000 in drawdown gives total annual income around $47,000 to $55,000. As the balance draws down and pension grows, this gradually improves through the 70s.

Please note: All figures are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

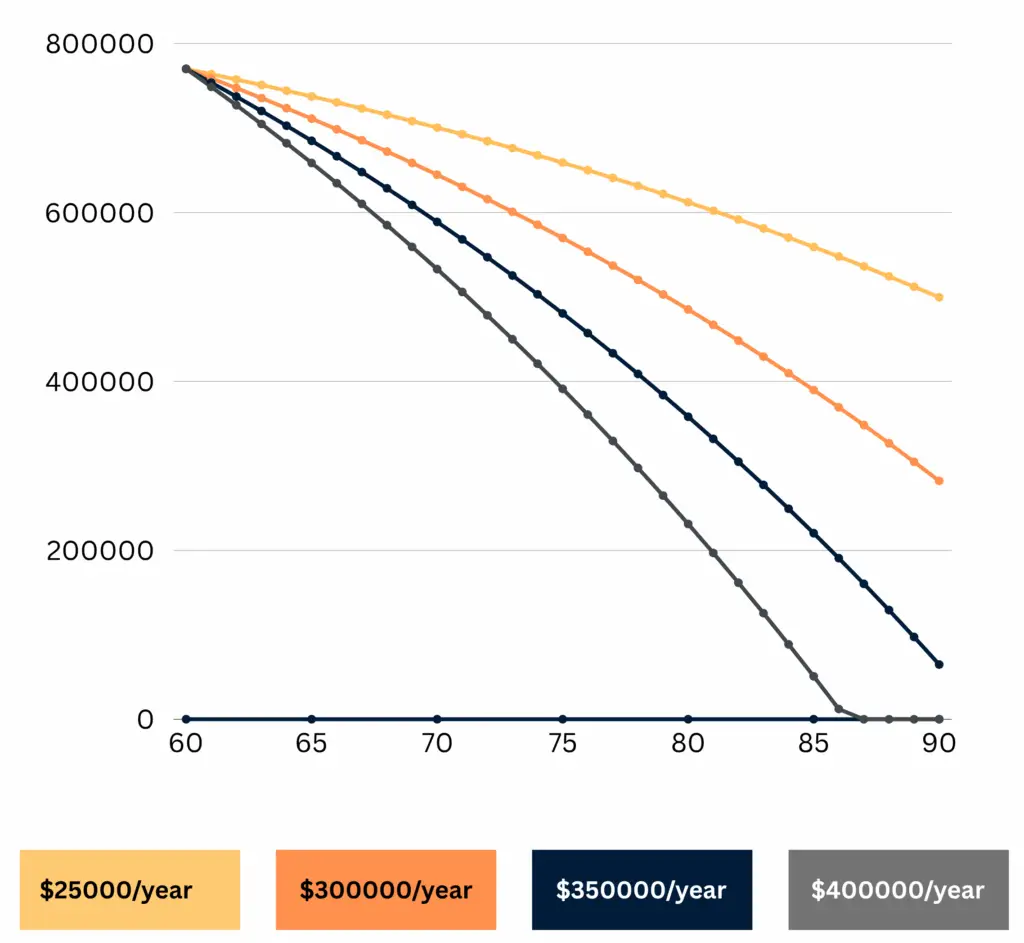

This Line Chart Visualise the depletion of $770K across ages 60 to 90 with spending levels at $25K, $30K, $35K, and $40K per year.

Which Super Fund and Investment Option for $770K in Retirement?

This is the question the GSC data for this page tells us readers are actually asking. “Super funds comparison Australia,” “best super funds for long-term growth Australia,” “best low-fee pension product Australia,” “best high growth super fund”, these queries are appearing because someone at $770K thinking about retirement is actively deciding where their money should be.

It is a genuinely important question. At this balance, the difference between a well-structured fund and a poorly-structured one is not trivial. A 0.5% difference in annual fees on $770K is $3,850 a year in lost returns that compound against you over 30 years.

Industry funds versus retail funds. Large industry funds (like Australian Super, Hostplus, Aware Super) generally carry lower fees than most retail funds for equivalent investment options. This fee advantage compounds significantly at $770K over a 30-year retirement. Australian Super’s balanced option fee structure, for example, runs notably lower than most retail fund equivalents. That said, the best fund for any individual depends on their specific investment options, insurance arrangements and service needs, not just the headline fee comparison.

The investment option inside the fund matters as much as the fund itself. Phil made this point directly in Episode 22 of the Wealthlab Podcast: “A balanced fund is not a true balanced fund with most of these funds these days. They are every day of the week a growth fund that they slap the name balanced on.” Understanding what your fund actually holds, not just the label it uses, affects your real return. Watch Episode 22 on YouTube.

Growth versus balanced for a 30-year retirement. For someone retiring at 60 with $770K and a 30-year horizon, the question of whether to use a high growth option (80%+ in shares and property) versus a balanced option (60 to 70% growth) is worth examining seriously. High growth funds have historically returned 7% to 9% per annum over rolling ten-year periods on the ASX. Balanced funds have returned 5% to 7%. The gap in outcomes over 30 years is significant.

The risk with a high growth option is sequence-of-returns: a sharp fall in the first two to three years of retirement when your balance is at its highest is more damaging than the same fall a decade later. The standard approach is to hold one to two years of spending in cash outside the pension account and keep the remaining balance in a balanced or growth option. This gives the growth assets time to recover without forcing you to sell at a low point.

Scott covered the long-term impact of investment choice in retirement directly in Episode 1 of the Wealthlab Podcast. A growth portfolio compared to a conservative one on identical spending funded the couple 15 years longer. Watch Episode 1 here.

Fees in the pension phase specifically. When comparing super funds for retirement income, look at the fee structure in pension phase, not accumulation phase. Some funds charge differently once you have converted to an account-based pension. Administration fees, investment fees and any ongoing advice fees all reduce your effective return. On $770K, even a 0.3% fee difference is over $2,300 a year.

SMSF as an option at this balance. Some Australians with $770K consider a self-managed super fund (SMSF), which allows direct control over investments including commercial property, direct shares and other assets. SMSFs carry a fixed cost base that generally makes them cost-effective from around $500,000 to $600,000 upwards. They also require meaningful ongoing administrative responsibility. For people who want to hold commercial property directly in super, an SMSF is the primary mechanism.

The key message: at $770K, reviewing your fund, investment option and fee structure before you retire is not an optional extra. It is one of the highest-value financial decisions you will make.

Age Pension at 67: The Trajectory for $770K

Current Age Pension rates as at May 2026 (Services Australia):

- Single (including supplements): approximately $29,754 a year

- Couple combined (including supplements): approximately $44,856 a year

Updated each March and September.

With approximately $540,000 remaining at 67, the initial part pension of around $12,000 a year is meaningful but not the dominant income source at this point. As the balance draws down through the 70s, pension entitlements grow. The full $29,754 becomes available once the balance falls below $314,000, likely in the early to mid-80s at moderate spending levels.

From that point, combined income from full pension plus remaining drawdown provides strong income security in the later retirement years, precisely when healthcare costs typically rise.

Phil and Dan worked through the assets test taper and how it evolves with real balances in Episode 10 of the Wealthlab Podcast. Watch Episode 10 here.

Our pension and Centrelink page covers the full application process and how to structure assets for maximum entitlements.

A Real Budget for $770K at 60

A sample $60,000 annual budget for a single homeowner:

| Category | Annual spend |

|---|---|

| Groceries and food | $12,000 |

| Housing costs, rates and insurance | $7,500 |

| Healthcare and private health cover | $9,500 |

| Transport and vehicle running costs | $6,000 |

| Domestic and international travel | $15,000 |

| Dining out and social activities | $6,000 |

| Utilities, phone and subscriptions | $3,500 |

| Clothing, personal and gifts | $500 |

This sits above the ASFA comfortable standard of $54,240 and includes a strong travel allocation, top-level private health and meaningful social spending. For most Australians, this is a genuinely comfortable and fulfilling retirement, not a budget one.

What Makes the Most Difference at $770K

Getting the investment option right before you retire. Reviewing your fund and investment option now, not after you retire, is the single highest-leverage financial decision available to you at this balance. A 30-year retirement at 5% versus 7% net return on $770K produces dramatically different outcomes.

Managing the first three years carefully. Sequencing risk, the impact of a sharp market fall in the early years when your balance is at its highest, is the main structural risk at this balance. One to two years of spending in cash outside your account-based pension means you are never forced to sell growth assets at a low point.

Planning the Age Pension trajectory. Arriving at 67 with $540,000 and a modest part pension is a different starting position from someone with $300,000 and near-full pension. Understanding the taper trajectory and how drawdown decisions in your 60s affect pension timing in your 70s and 80s is genuinely valuable. Episode 10 covers this well.

Knowing what fees you are actually paying. At $770K, audit your fund’s fee structure before you set up your account-based pension. Administration fees, investment fees and any adviser service fees all compound against your balance over 30 years.

Use the free Wealthlab super calculator to model how different spending levels, growth rates and fee structures affect your balance through retirement. Our retirement planning page has more on pre-retirement structuring decisions.

FAQ: Retiring at 60 with $770K in Australia

Can I retire at 60 with $770K in Australia? Yes, comfortably for a single homeowner. At $58,000 to $62,000 annual spending and 5% net return, $770K leaves approximately $540,000 at 67 when the Age Pension begins supplementing income. Combined income from part pension and ongoing drawdown sustains the ASFA comfortable standard well into the 80s.

What is the best way to invest $770K in super for retirement? Most retirees use a balanced or growth investment option inside an account-based pension as the core structure. At $770K with a 30-year horizon, a growth-oriented option typically outperforms a conservative one significantly over time. Keeping one to two years in cash provides stability without sacrificing long-term returns. Fund fees matter more at this balance than at lower amounts.

How does super fund comparison affect retirement at $770K? Meaningfully. A 0.5% annual fee difference on $770K is $3,850 a year, compounding over 30 years into a very significant difference in outcomes. Large industry funds generally carry lower fees than retail funds for equivalent investment options. The investment option inside the fund matters as much as the fund itself.

What is the best super fund for long-term growth in Australia? This depends on your specific investment option, fee structure and individual circumstances. Generally, large industry funds have outperformed retail funds over long periods on a net-of-fees basis for members in their default options. For retirees, the relevant comparison is the pension phase fee structure and the range of investment options available, not accumulation phase returns. A financial adviser can compare specific funds against your situation.

What is a low-fee pension product in Australia? A low-fee account-based pension is typically offered by large industry funds with administration fees under 0.2% per annum and investment fees under 0.5% for balanced or growth options. Some funds also offer fee caps at higher balances that reduce the effective fee rate on amounts above certain thresholds. Reviewing and comparing fee structures before converting to pension phase is worth the time at $770K.

Should I consider an SMSF at $770K? It is worth examining. At $770K, the fixed costs of running an SMSF (accounting, audit, administration) are generally spread over a sufficient base for it to be cost-competitive with retail funds. The main advantages are investment control, including direct shares and commercial property. The main cost is administrative responsibility.

Will I receive the Age Pension with $770K at 60? By 67, at $58,000 to $62,000 annual spending from 60, approximately $540,000 remains. Above the full pension threshold of $314,000, so a part pension of around $12,000 a year initially. Pension entitlements grow as the balance draws down through the 70s, with the full $29,754 arriving when the balance falls below the threshold, likely in the early to mid-80s.

Is $770K enough for a couple to retire at 60? As a combined balance, $770K is workable but below ASFA’s comfortable couple standard of $77,375 a year. A couple targeting genuine comfort at this combined balance would benefit from one partner continuing part-time work through the early 60s, or from building the combined balance toward $900,000 to $1,000,000 before stopping.

What to Do Next

At $770K, the retirement is not in question. The planning work is in the structure: which fund, which investment option, what fees, how to manage the Age Pension taper, and how to handle the first few years of drawdown. These decisions have a larger cumulative impact on your 30-year retirement outcome than almost anything else from this point forward.

Or take the free Wealthlab retirement quiz for a general read on your retirement position. Or book a free, no-pressure chat with the Wealthlab team to work through the fund, investment and structuring questions that matter at this balance level.