“How much super do I need to retire at 60?” is one of the most searched retirement questions in Australia. But it’s actually two questions wrapped in one: how much do I need, and am I on track to get there?

This guide answers both. It covers the 2026 super balance targets at every age from 30 to 67, what different balances actually fund at retirement, how the Age Pension changes the picture from 67, and what to do if your balance is behind where it should be.

The Short Answer: How Much Super Do You Need to Retire at 60?

For a single Australian homeowner wanting a modest to comfortable lifestyle at 60, the target range is:

| Lifestyle target | Super needed at age 60 | Annual income it supports |

|---|---|---|

| Modest (homeowner) | $350,000 to $450,000 | $25,000 to $32,000 per year |

| Mid-range (homeowner) | $450,000 to $600,000 | $32,000 to $42,000 per year |

| ASFA comfortable (homeowner) | $750,000 to $900,000 | $54,837 per year |

For couples, add roughly $100,000 to $150,000 to each figure given shared fixed costs and two Age Pension entitlements from 67.

These figures are higher than the ASFA benchmarks for retirement at 67 because retiring at 60 means funding seven extra years before the Age Pension starts. That seven-year bridge is the defining planning challenge for anyone retiring before 67.

Please note: All figures, projections and scenarios in this article are for general illustration only. Individual outcomes depend on personal circumstances, spending levels, investment returns, fees and government policy. This is general information, not personal advice.

Super Balance Targets by Age: Are You on Track?

The table below shows the super balance you should be tracking toward at each age milestone for a comfortable retirement at 67 (single homeowner, based on ASFA February 2026 standard of $630,000 at 67). These figures assume the 12% employer SG, a balanced investment option averaging 7% gross returns, and no additional contributions beyond the employer minimum.

| Age | On-track balance target | Average actual balance (APRA data) |

|---|---|---|

| 30 | $55,000 to $75,000 | ~$45,000 (men) / ~$36,000 (women) |

| 35 | $100,000 to $135,000 | ~$83,000 (men) / ~$66,000 (women) |

| 40 | $150,000 to $200,000 | ~$133,000 (men) / ~$102,000 (women) |

| 45 | $210,000 to $275,000 | ~$185,000 (men) / ~$142,000 (women) |

| 50 | $280,000 to $370,000 | ~$268,000 (men) / ~$207,000 (women) |

| 55 | $360,000 to $460,000 | ~$322,000 (men) / ~$254,000 (women) |

| 60 | $430,000 to $530,000 | ~$396,000 (men) / ~$313,000 (women) |

| 67 | $630,000 (single) / $730,000 (couple) | ASFA comfortable benchmark |

Sources: ASFA Retirement Standard February 2026; APRA Quarterly Superannuation Statistics December 2025

What the gap column tells you: At every age, average actual balances sit below the comfortable retirement track. This is not unusual. The majority of Australians retire on below-ASFA-comfortable balances and use the Age Pension to supplement. The gap is not a crisis, it’s the design of the system, but it is information worth acting on in your working years.d market variation.

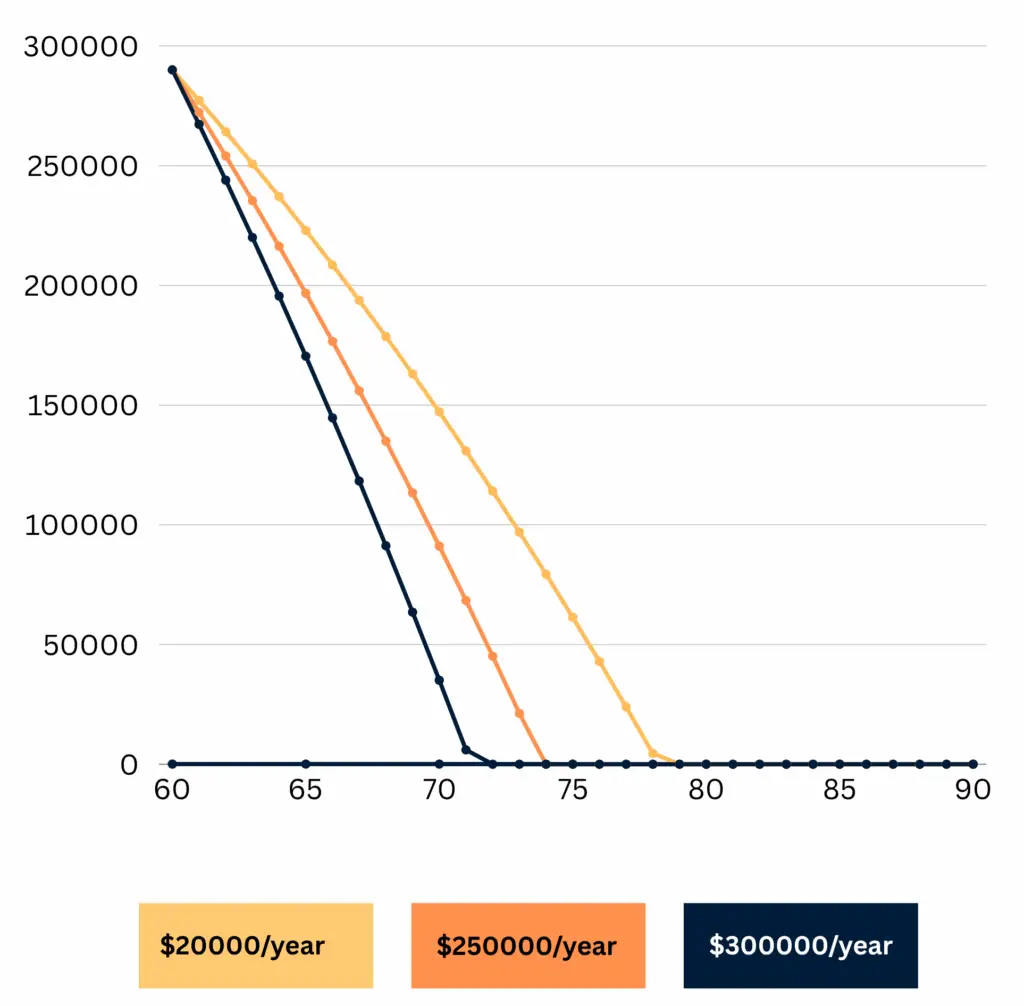

This line chart showing your super balance from age 60 to 90 under different spending levels ($20K, $25K, $30K/year) offers a clear comparison of how long your funds could last.

The 2026 ASFA Retirement Standard: What Each Level Covers

The ASFA Retirement Standard (updated February 2026) is the most widely used benchmark for retirement adequacy in Australia.

| Standard | Single annual income | Couple annual income | Lump sum needed at 67 |

|---|---|---|---|

| Modest | $36,700 | $52,800 | $110,000 (single) / $120,000 (couple) |

| Comfortable | $54,837 | $77,375 | $630,000 (single) / $730,000 (couple) |

Both standards assume home ownership and supplement from the Age Pension. The modest standard relies primarily on the Age Pension with super as a small supplement. The comfortable standard relies primarily on super with a partial pension supplement that grows over time.

What comfortable actually covers: Private health insurance (hospital and extras), a reliable car replaced as needed, annual domestic holidays, an overseas trip every seven years, regular dining out and social activities, ability to replace household items and appliances. Not luxury, but genuine independence and choice.

What modest covers: Basic private health cover, a budget car or public transport, infrequent domestic travel, limited dining out and social activities. Reliant on government concessions (pensioner concession card) to manage healthcare and utility costs.

Source: ASFA Retirement Standard, February 2026

What Different Balances at 60 Actually Fund

Here’s what various starting balances at 60 support in practice, using a 5% net annual return in a balanced account-based pension and assuming home ownership.

$300,000 at 60: Supports $20,000 to $23,000 per year during the bridge to 67. Arrives at 67 with approximately $175,000 to $215,000, qualifying for the full Age Pension of approximately $29,000 per year. Combined income from 67: approximately $35,000 to $38,000 annually. Workable for a homeowner with no debt and low fixed costs.

$400,000 at 60: Supports $25,000 to $30,000 per year during the bridge. Arrives at 67 with approximately $290,000 to $330,000. Likely qualifies for the full or near-full Age Pension. Combined income from 67: approximately $40,000 to $44,000 annually. Mid-range modest to comfortable territory for a homeowner.

$500,000 at 60: Supports $30,000 to $35,000 per year. Arrives at 67 with approximately $380,000 to $430,000. Part Age Pension applies. Combined income from 67: approximately $45,000 to $50,000 annually. Approaches the ASFA comfortable standard.

$630,000 at 60: Supports $35,000 to $40,000 per year. Arrives at 67 with approximately $490,000 to $550,000. Part Age Pension. Combined income from 67: approximately $50,000 to $58,000. Comfortably in ASFA comfortable territory. Well-funded retirement by any Australian benchmark.

$800,000+ at 60: Supports $42,000 to $50,000+ per year. Arrives at 67 with $600,000 to $700,000+. May exceed the Age Pension assets test initially, though as the balance draws down over time a part pension typically becomes available. Combined income from 67: $55,000 to $65,000+.

The Seven-Year Bridge: The Retirement at 60 Planning Problem

Retiring at 60 means seven full years of self-funded retirement before Age Pension eligibility at 67. During that window, every dollar of income comes from your own super balance.

This is why the super needed to retire at 60 is significantly higher than the ASFA figure for retirement at 67. The ASFA $630,000 benchmark is for retirement at 67, where the Age Pension immediately provides $29,000 per year as a floor.

At 60 with $630,000, you spend seven years drawing from super before the pension arrives. At $35,000 per year that’s $245,000 in drawdown plus foregone investment earnings over the bridge years. By 67 you have approximately $500,000 remaining, above the full pension threshold but within part pension range.

The practical question for anyone planning retirement at 60: not just “how much do I have?” but “how much do I spend in the bridge years, and what does that leave at 67 when the pension calculation begins?”

Scott and Phil covered the real cost of this gap in Episode 19 of the Wealthlab Podcast: “Is Early Retirement a Trap? The $150K Gap Most Aussies Miss.”

How the Age Pension Changes Everything From 67

The Age Pension is not a fallback for people who didn’t plan. It’s a structural part of how the Australian retirement system is designed to work for the majority of retirees.

Full Age Pension rates from March 2026:

| Per fortnight | Per year | |

|---|---|---|

| Single | ~$1,116 | ~$29,000 |

| Couple combined | ~$1,682 | ~$43,700 |

Assets test thresholds for homeowners (March 2026):

| Full pension threshold | Part pension cut-off | |

|---|---|---|

| Single | Below $321,500 | Up to ~$695,500 |

| Couple combined | Below $481,500 | Up to ~$1,045,500 |

Source: Services Australia: Age Pension (Current as at May 2026)

For most Australians retiring at 60 with $300,000 to $500,000 in super, the drawdown during the bridge years reduces the balance enough by 67 to qualify for a full or substantial part Age Pension. That pension then becomes the floor income, reducing the required super drawdown and extending how long the balance lasts.

This interaction between super and the Age Pension is the core of retirement income planning. Understanding it early allows you to structure drawdowns and assets in a way that maximises your combined income. Phil and Dan walked through real case studies in Episode 10 of the Wealthlab Podcast: “How the Age Pension Really Works.”

Super Consumers Australia: An Alternative Benchmark

Most of the coverage of retirement savings targets refers to ASFA. But there is a second widely respected benchmark worth knowing: Super Consumers Australia.

Super Consumers Australia uses actual ABS data on what retirees genuinely spend rather than a modelled lifestyle budget. Their finding: a typical single retiree spending at a medium level needs around $322,000 in super at retirement. At that level, the Age Pension covers approximately 67% of living costs and super tops up the rest.

Their benchmark is lower than ASFA because retirees typically spend less in reality than lifestyle budgets suggest, and because the Age Pension provides a larger share of actual income for most Australians than ASFA’s modelling reflects.

The two benchmarks bracket a useful range:

- Super Consumers Australia: $322,000 (medium spending, actual data)

- ASFA comfortable: $630,000 (comfortable lifestyle, modelled)

Where you want to be within that range depends on what you actually want your retirement to look like.

What If Your Balance Is Behind the Target?

If your balance is below the on-track figure for your age, you have more options in your 50s than most people realise.

Salary sacrifice into super. Every dollar contributed before tax is taxed at 15% rather than your marginal rate. On a $90,000 salary at a 37% marginal rate, each $10,000 of salary sacrifice saves approximately $2,200 in tax while boosting your balance. The concessional contributions cap is $30,000 per year including your employer’s 12% SG.

Catch-up concessional contributions. If your total super balance is under $500,000 and you’ve had unused concessional cap space in the past five years, you can carry forward those unused amounts and contribute them on top of the $30,000 annual cap in a single year. Unused amounts from the 2020/21 financial year expire permanently on 30 June 2026. Check your carry-forward balance in myGov now if this applies to you. Scott and Phil covered this strategy in detail in Episode 7 of the Wealthlab Podcast.

Downsizer contributions. If you’re 55 or over and own your home, the downsizer contribution rules allow you to contribute up to $300,000 per person from the sale proceeds of your home into super, outside the standard contribution caps. For a homeowner with significant property equity, this can close a large super gap very quickly. See our full guide on downsizer contributions Australia.

Review your investment option. Many Australians in their 50s are in a default balanced option that is more conservative than necessary for a 25 to 30 year retirement horizon. At 50, you likely have 10 or more years before retirement. Staying in a growth or high-growth option for another 5 to 7 years before gradually moderating can meaningfully improve your end balance. As Scott covered in Episode 1 of the Wealthlab Podcast, the long-term gap between growth and conservative returns is larger than most people appreciate.

Work an extra year or two. Each additional year of work adds employer SG, avoids drawdown, and allows existing balances to compound. At $400,000, working one more year at $80,000 improves your retirement position by approximately $55,000 to $65,000 combined (SG contributions, avoided drawdown, one more year of investment growth).

Women and Super: The Gap That Needs Addressing

Women in Australia retire with substantially less super than men. The average balance at 60 to 64 is approximately $313,000 for women versus $396,000 for men, based on APRA data. Women also live longer, an average of 85 years versus 81 for men, meaning their super needs to last four years longer.

The gap comes from career breaks for caring responsibilities, higher rates of part-time work, and lower average lifetime earnings. It’s structural, not personal.

The most effective strategies for women approaching retirement who want to close this gap are catch-up contributions (particularly after returning from career breaks), spouse contribution splitting from a higher-earning partner, and reviewing investment options (women tend to hold more conservative super options despite needing longer growth horizons).

Scott and Phil covered this in Episode 17 of the Wealthlab Podcast: “Retirement Age Revealed: The Truth for Women.”

Frequently Asked Questions

How much super do I need to retire at 60 in Australia?

For a single homeowner, roughly $350,000 to $450,000 to support modest spending of $25,000 to $32,000 per year through the seven-year bridge to Age Pension eligibility at 67. For a comfortable lifestyle of $35,000 to $42,000 per year, $500,000 to $650,000 at 60 is a reasonable target. ASFA’s comfortable benchmark of $630,000 is set for retirement at 67, not 60; retiring at 60 on the same balance requires more conservative spending in the early years.

How much super should I have at 40 in Australia?

Approximately $150,000 to $200,000 for someone targeting a comfortable retirement at 67 on the employer SG alone. If your balance is below this range, additional contributions through salary sacrifice and the concessional cap are the most tax-effective way to close the gap over the coming decade.

How much super should I have at 50?

Approximately $280,000 to $370,000 to be on track for a comfortable retirement at 67 without additional contributions. The average actual balance at 50 is around $268,000 for men and $207,000 for women, meaning the majority of Australians are below the comfortable track at this age. The 50s are the highest-impact decade for catch-up contributions and salary sacrifice.

Is $500,000 enough to retire at 60 in Australia?

For a single homeowner, $500,000 at 60 supports a comfortable mid-range retirement, drawing $30,000 to $35,000 per year during the bridge and arriving at 67 with approximately $380,000 to $430,000. A part Age Pension from 67 plus reduced super drawdown produces a combined income of around $45,000 to $50,000 annually, which is close to the ASFA comfortable standard for a single homeowner.

Is $300,000 enough to retire at 60 in Australia?

For a single homeowner with no debt and modest spending expectations, yes. Drawing $20,000 to $23,000 per year, $300,000 bridges to 67 with enough remaining to qualify for the full Age Pension of approximately $29,000 per year. Combined income from 67 of $35,000 to $38,000 per year is the ASFA modest standard territory. For a renter or someone with a mortgage, $300,000 at 60 is tight.

What is the average super balance at 60 in Australia?

Approximately $396,000 for men aged 60 to 64 and $313,000 for women aged 60 to 64, based on APRA Quarterly Superannuation Statistics December 2025. These are averages that include a wide range of balances. The median (midpoint) is lower than both.

What is the ASFA comfortable retirement standard for 2026?

$630,000 in super for a single homeowner at age 67 and $730,000 for a couple. This funds annual spending of $54,837 for a single person and $77,375 for a couple, including private health insurance, a reliable car, annual domestic holidays, regular dining out and the ability to replace household items as needed. Updated February 2026.

How much super do I need to retire at 65 in Australia?

Retiring at 65 requires two fewer years of bridge funding before the Age Pension starts at 67. A single homeowner targeting $35,000 per year spending needs approximately $400,000 to $500,000 at 65, less than the equivalent target at 60 because the Age Pension bridge is only two years rather than seven.

How does the Age Pension affect how much super I need?

Significantly. The Age Pension of approximately $29,000 per year for a single person reduces the amount you need to draw from super after 67. For most Australians with moderate super balances, the Age Pension provides 40% to 70% of retirement income from 67, meaning the super balance needs to fund the gap above that floor rather than the entire retirement lifestyle.

Check Where You Actually Stand

Every balance-by-age table is a rough guide. Your actual number depends on your salary, how long you work, your investment option, your spending plans, and whether you’re single or part of a couple.

The free Wealthlab super calculator takes about two minutes and shows you how your actual balance compares to on-track targets and what your projected retirement income looks like based on your current trajectory.

If you want a proper retirement income plan built around your specific numbers, book a free chat with the Wealthlab team,or take the free Wealthlab retirement quiz .