If you’re sitting on $265,000 in super and wondering whether to retire at 60 or push to 65, you’re asking exactly the right question. Five years sounds short. In retirement terms, it can be the difference between the money lasting and the money running out.

This article runs the real comparison: what $265K does if you stop at 60, what it does if you stop at 65, and what most people in this position are missing when they make that call.

Why Retiring at 60 vs 65 Is Such a Big Decision

The gap between retiring at 60 and retiring at 65 is not just five years of income. It’s five extra years of super contributions, five more years of compounding growth, five fewer years of drawdown before the Age Pension starts, and a significantly different balance by the time you hit 67.

Scott and Phil covered the early retirement trap in detail on the podcast. In Episode 19, they walked through how retiring one year earlier than planned can shift a retirement from funded to running out by 79. With $265K in super, the version of this that applies at 60 vs 65 is even more stark. Watch Episode 19 on YouTube.

The core issue is that the Age Pension doesn’t start until 67. Retiring at 60 means seven years of fully self-funded living. Retiring at 65 cuts that to two years. That difference in the self-funding gap is what drives most of the numbers below.

Retiring at 60 with $265K: What the Numbers Look Like

At 60, you’ve hit preservation age. If you stop working and retire, you can convert your super into a tax-free account-based pension and start drawing income.

At $28,000 to $30,000 a year spending and a 5% net return, here’s how $265K tracks through to the Age Pension at 67:

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 60 | $265,000 | $28,000 | $11,850 | $248,850 |

| 61 | $248,850 | $28,500 | $11,018 | $231,368 |

| 62 | $231,368 | $29,000 | $10,118 | $212,486 |

| 63 | $212,486 | $29,500 | $9,149 | $192,135 |

| 64 | $192,135 | $30,000 | $8,107 | $170,242 |

| 65 | $170,242 | $30,000 | $7,012 | $147,254 |

| 66 | $147,254 | $30,000 | $5,863 | $123,117 |

| 67 | $123,117 | Pension starts | ~$113,000 |

By 67, around $113,000 remains in super and the Age Pension begins. For a single homeowner, that balance falls well under the full pension assets test threshold of around $314,000 (current as at May 2026, Services Australia), so near-full pension entitlements are likely.

Please note: All figures in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.

Retiring at 65 with $265K: A Very Different Picture

Now compare what happens if you work five more years before stopping.

Assuming a starting balance of $265K at 60, ongoing employer contributions at 11.5% of a $70,000 salary, and a 7% annual return inside super, the balance at 65 would be in the range of $490,000 to $530,000. That is almost double the $265K starting point, thanks to contributions and compounding together over five years.

With that larger balance at 65, the numbers look quite different:

- The Age Pension gap to bridge is just two years instead of seven

- The opening drawdown balance is nearly twice as large

- Spending at $40,000 to $45,000 a year becomes much more manageable

- The balance at 67 is likely high enough for at least a part pension, with the full pension coming into range as it draws down through the 70s

The contrast is significant. Retiring at 65 with a balance in the $490K to $530K range puts someone in a genuinely comfortable position. Retiring at 60 with $265K is workable for a homeowner spending carefully, but it requires discipline and realistic expectations.rst appears.

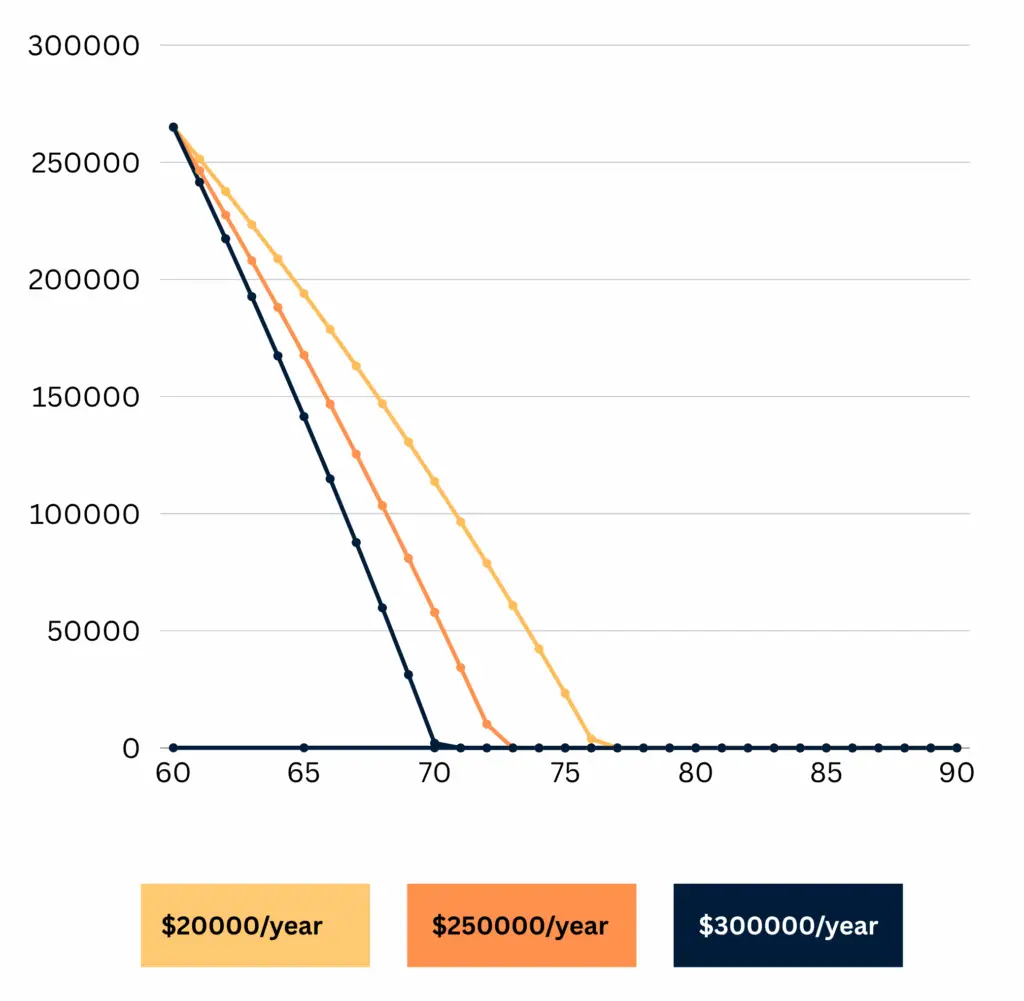

This line chart showing depletion of $265K from age 60 to 90 under three spending levels: $20K, $25K, and $30K. This will help visualise your options clearly.

The ASFA Retirement Standard for 2026

According to the ASFA Retirement Standard (February 2026 update), retirement costs for a homeowner are:

- Single, modest lifestyle: $35,199 a year

- Single, comfortable lifestyle: $54,240 a year

- Couple, modest lifestyle: $50,866 a year

- Couple, comfortable lifestyle: $77,375 a year

At $28,000 to $30,000 a year, the scenario above for retiring at 60 with $265K sits below the modest standard. That is the honest reality. It is not a comfortable retirement by ASFA’s measure, but for homeowners without debt and realistic expectations, many Australians manage well on less than ASFA’s modest figure, particularly in the early years.

The Age Pension: The Number That Changes Everything

Current Age Pension rates as at May 2026 (Services Australia):

- Single (including supplements): approximately $29,754 a year

- Couple combined (including supplements): approximately $44,856 a year

These figures are updated by the government each March and September.

Once the Age Pension starts at 67, the pressure on your super drops sharply. Someone spending $30,000 a year and receiving close to the full pension needs to draw very little from their own savings to cover the gap. That dramatically extends how long the remaining super balance lasts.

For a clear walkthrough of how the assets test and income test work in practice, Episode 10 of the Wealthlab Podcast runs through real case studies. Watch it on YouTube.

What Retiring at 60 Actually Requires

Owning your home outright is not optional with $265K. Without it, the numbers fall apart. Every projection above assumes zero housing costs.

Spending discipline in the first few years is critical. The early years carry a disproportionate weight on your total retirement outcome. Drawing heavily in years one and two from a modest balance compounds into a real problem a decade later.

Keeping some growth in your investments matters more than most people realise. In Episode 1 of the Wealthlab Podcast, Scott ran through what happens to a growth portfolio versus a conservative one over a long retirement. The gap in outcomes is significant, and at $265K, parking everything in cash is one of the riskier things you can do. Watch Episode 1 here.

Part-time work in the early 60s is worth considering seriously. Even $15,000 to $20,000 a year from part-time work between 60 and 63 delays super drawdown by years and improves the Age Pension position at 67.

Want to see how your specific balance plays out under different retirement ages and spending levels? The free Wealthlab super calculator runs those scenarios in a couple of minutes.

The Honest Side-by-Side

| Retire at 60 with $265K | Retire at 65 with ~$500K | |

|---|---|---|

| Self-funding gap to Age Pension | 7 years | 2 years |

| Estimated balance at 67 | ~$113,000 | ~$370,000 to $430,000 |

| Likely pension entitlement at 67 | Near full pension | Part pension initially |

| Annual spending capacity (comfortable) | $28,000 to $30,000 | $40,000 to $50,000 |

| Risk of running short | Higher | Lower |

| Lifestyle | Modest, homeowner required | Moderate to comfortable |

Five extra years of work is a real cost in terms of your time and health. But the financial difference between these two scenarios is large enough that it is worth knowing clearly before making the decision. Many people do not do this comparison before they stop working and end up with fewer options later.

Common Mistakes in This Situation

Assuming the Age Pension starts automatically is one of the most common issues. You need to apply through Centrelink, and the assets and income tests can surprise people. Getting advice on how to structure your affairs before 67, not after, makes a meaningful difference.

Withdrawing large lump sums early is the other major one. An early renovation or overseas trip sounds reasonable in year one, but from a modest base, large withdrawals in the first few years are very hard to recover from.

Underestimating healthcare costs catches people in their 70s. These tend to rise sharply and are often not factored into early retirement budgets. Our retirement planning page covers how to think about this.

FAQ: Retiring at 60 vs 65 with $265K

Can I retire at 60 with $265K in Australia? For a single homeowner spending around $28,000 to $30,000 a year, it is workable. It requires careful drawdown management and the Age Pension topping up income from 67. It is not a comfortable retirement by ASFA’s definition, but for the right circumstances it can be a realistic one.

Is retiring at 60 vs 65 a big financial difference? Yes. Five extra years of work typically more than doubles the super balance available at retirement when you factor in contributions and compounding. It also cuts the self-funding gap before the Age Pension from seven years to two. The financial difference between the two scenarios is substantial.

How much will I have at 67 if I retire at 60 with $265K? At $28,000 to $30,000 a year spending and 5% net returns, roughly $113,000 to $120,000 remains at 67. That puts most single homeowners within range of the full Age Pension assets test threshold.

When can I access my super? At 60, if you have retired from the workforce. Preservation age is 60 for anyone born after 1 July 1964. See our superannuation page for more detail on conditions of release.

Will I qualify for the Age Pension if I retire at 60 with $265K? Almost certainly by 67. Drawing down over seven years from $265K typically leaves a balance well below the full pension assets test threshold for a single homeowner, currently around $314,000 (May 2026). Your home is exempt from the assets test.

What if I retire at 62 or 63 instead? That can be a useful middle path. Two or three more years of contributions and reduced drawdown years meaningfully changes the trajectory without committing to another full five years of work. Some people use a transition to retirement strategy to reduce hours rather than stop entirely.

What is the difference between retiring at 60 and retiring at 65 in terms of the Age Pension? Retiring at 60 means seven years of fully self-funded retirement before the Age Pension starts. Retiring at 65 means only two. That five-year difference in the self-funding gap is the main reason the financial outcomes between the two scenarios are so different.

What to Do Next

If you are trying to decide between retiring at 60 and 65 with a balance around $265K, the clearest thing you can do is model both scenarios with your actual numbers, not general tables. Your salary, super fund, expected spending and housing situation all affect the outcome in ways a generic comparison cannot capture.

Not sure where your retirement actually stands? or take the free Wealthlab retirement quiz for a general read on your position. Or book a free, no-pressure chat with the Wealthlab team to talk through your situation with someone who lo