nsion at 67 and still leave a meaningful balance when the pension starts.

What $280K does not support on its own is a comfortable retirement in ASFA’s terms. According to the ASFA Retirement Standard (February 2026), a comfortable retirement costs a single homeowner around $54,240 a year. $280K cannot sustain that level of spending from 60 to 67 without running dangerously low before the Age Pension arrives.

For couples, $280K as a combined balance is very tight. For a single homeowner who owns their home outright, spends carefully and understands what they are signing up for, it is a realistic base.

The more interesting question is whether waiting another one to two years, or using a transition to retirement strategy to build the balance a little further, changes the picture enough to be worth it. For most people at this balance, the answer is yes.

What the Numbers Look Like If You Retire at 60 Now

At $28,000 to $30,000 a year spending and 5% net return inside an account-based pension:

| Age | Opening balance | Withdrawal | Net growth (5%) | Closing balance |

|---|---|---|---|---|

| 60 | $280,000 | $28,000 | $12,600 | $264,600 |

| 61 | $264,600 | $28,500 | $11,806 | $247,906 |

| 62 | $247,906 | $29,000 | $10,945 | $229,851 |

| 63 | $229,851 | $29,500 | $10,018 | $210,369 |

| 64 | $210,369 | $30,000 | $9,018 | $189,387 |

| 65 | $189,387 | $30,000 | $7,969 | $167,356 |

| 66 | $167,356 | $30,000 | $6,868 | $144,224 |

| 67 | $144,224 | Pension starts | ~$132,000 |

By 67, roughly $132,000 remains and the Age Pension begins. For a single homeowner, that balance falls well under the full pension assets test threshold of around $314,000 (current as at May 2026, Services Australia), which means near-full pension entitlements are likely.

Combined income at 67, from the near-full single pension of approximately $29,754 plus modest drawdown from the remaining balance, puts annual retirement income in the range of $35,000 to $42,000. That is a workable figure for a homeowner with no debt.

Please note: All figures are approximate and for illustrative purposes only. Individual outcomes will vary based on spending, investment returns, fees and personal circumstances. This is general information, not personal advice.some super left to top it up.

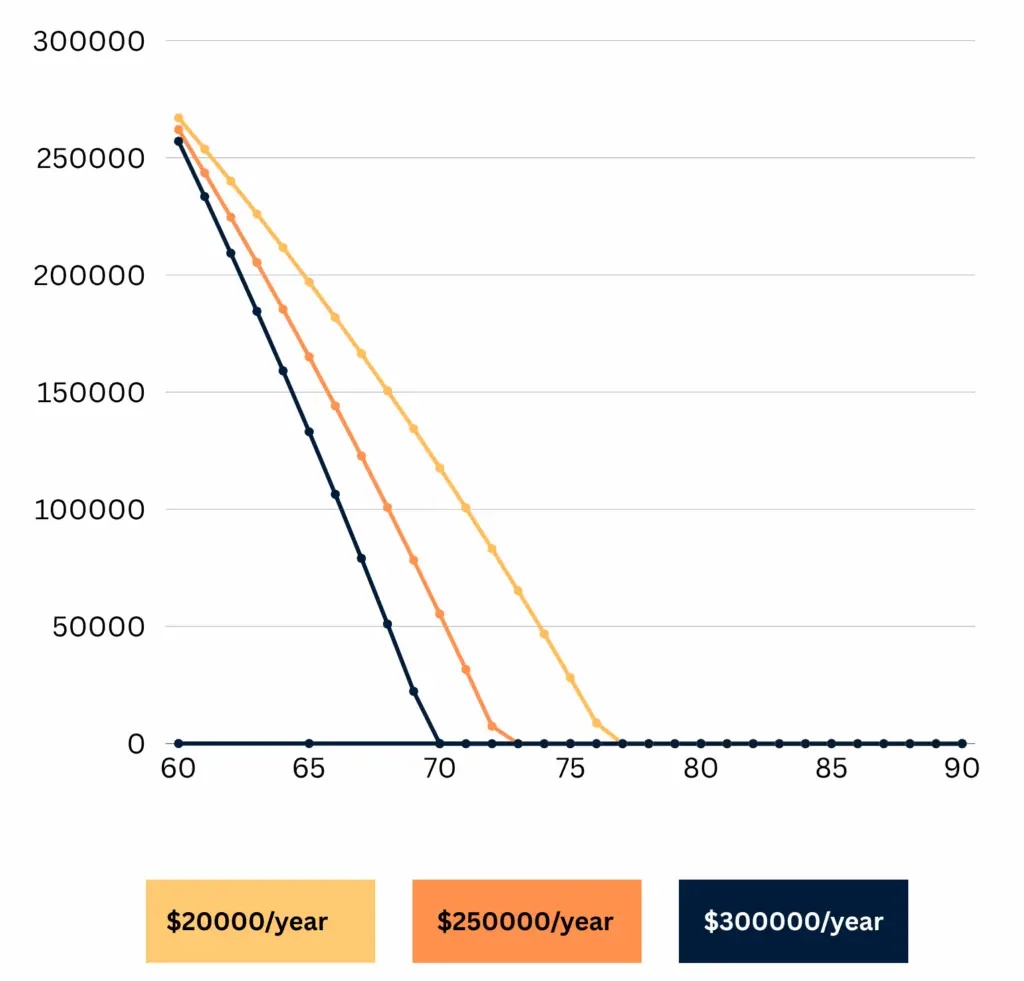

This line chart visualising how $280K depletes from age 60 to 90 under three spending levels helps show your likely outcomes.

.

What If You’re Not Quite Ready to Stop?

This is where $280K becomes genuinely interesting. The difference between retiring at 60 with $280K and retiring at 62 with $340K to $360K is not just $60,000 to $80,000. It’s two fewer years of drawdown before the Age Pension, a significantly higher balance at 67, and more comfortable spending room throughout.

Two years of employer contributions at 11.5% Super Guarantee on a $70,000 salary adds around $16,100. Two years of compounding growth at 7% on the existing balance adds another $40,000 to $42,000. That’s roughly $56,000 to $58,000 more going into retirement, before any personal contributions.

If you can work even part-time for two more years rather than stopping entirely at 60, the retirement outcome from $280K improves considerably.

The Transition to Retirement Option

One option worth understanding at this balance level is a transition to retirement (TTR) pension. From preservation age (60), you can start a TTR pension while still working. This lets you draw up to 10% of your super balance as income each year, which many people use to reduce work hours without reducing their take-home pay.

The typical setup: salary sacrifice more into super to reduce your tax while drawing income from your TTR pension to replace what you sacrificed. This can grow your super faster while reducing hours. Scott and Phil covered the mechanics of TTR and preservation age in Episode 18 of the Wealthlab Podcast. Watch Episode 18 on YouTube.

A TTR pension earns 15% tax on investment earnings rather than the zero tax you get in a fully retired pension phase, so it is generally more of a transitional tool than a long-term strategy. Whether it makes sense for your specific situation depends on your income, tax position and super fund. Speaking with a financial adviser before setting one up is worth doing.

The ASFA Retirement Standards for 2026

According to the ASFA Retirement Standard (February 2026 update):

- Single homeowner, modest lifestyle: $35,199 a year

- Single homeowner, comfortable lifestyle: $54,240 a year

- Couple homeowners, modest lifestyle: $50,866 a year

- Couple homeowners, comfortable lifestyle: $77,375 a year

At $28,000 to $30,000 a year, retiring at 60 with $280K sits below the modest standard. That is the honest position. It is not a comfortable retirement by these measures, but for homeowners in the right circumstances, many Australians live well below the ASFA modest benchmark, particularly in their early 60s before healthcare costs rise.

Age Pension Rates for 2026

Current Age Pension rates as at May 2026 (Services Australia):

- Single (including supplements): approximately $29,754 a year

- Couple combined (including supplements): approximately $44,856 a year

Updated each March and September by the Australian Government.

Once the Age Pension starts at 67, the financial picture shifts significantly. For someone spending $30,000 a year, near-full pension covers the majority of living costs. The remaining super balance then needs only to fund the gap, which dramatically extends how long it lasts.

Phil and Dan walked through the Age Pension assets and income test in detail with real case studies in Episode 10 of the Wealthlab Podcast. If you are not clear on how the tests work and how your super balance affects your entitlements, it is a genuinely useful listen. Watch Episode 10 on YouTube.

What This Balance Level Requires to Make Retirement Work

Own your home outright. Every projection above assumes zero housing costs. With rent or a mortgage, $280K becomes very difficult to sustain from 60 to 67. Clearing the mortgage before retiring, even if it means working another six to twelve months, changes the outcome substantially.

Draw down conservatively in the first few years. Retirement spending tends to be highest in the early years, when people are active and keen to travel and spend on the home. From a base of $280K, drawing $35,000 to $40,000 a year early on is a meaningful risk. Keeping spending close to $28,000 to $30,000 through the early 60s preserves considerably more capital for the later years when healthcare costs rise and flexibility matters most.

Maintain growth exposure in your investment mix. Retirement is not the signal to move everything to cash. A portfolio sitting entirely in cash loses ground to inflation every year even before withdrawals. Scott addressed this directly in Episode 1 of the Wealthlab Podcast, comparing growth versus conservative portfolios over a long retirement. The gap in outcomes is significant. Watch Episode 1 here.

Plan for the Age Pension before you hit 67, not after. You need to apply through Centrelink, and how you have structured your assets in the years before pension age affects what you receive. Episode 9 of the podcast covers a real case study where super fund advice caused an avoidable Age Pension loss. Watch Episode 9 here.

Want to see how your numbers hold up under different retirement ages and spending levels? The free Wealthlab super calculator runs through the scenarios in a couple of minutes.

Should You Retire Now or Wait?

This is not a question with one answer. For some people at $280K, stopping at 60 is the right call because of health, burnout or circumstances that make continuing work genuinely unrealistic. The numbers work at a modest level.

For others, another year or two of work, or a transition to part-time through a TTR strategy, can be the difference between a retirement that feels tight and one that feels genuinely comfortable. The financial difference between stopping at 60 and stopping at 62 with $280K as a starting point is meaningful enough to understand clearly before deciding.

The question Phil raised in Episode 5 of the podcast captures it well: the spreadsheet says one thing, but living, breathing people with emotions say another. Both matter. Watch Episode 5 on YouTube.

Our retirement planning page covers the broader decisions involved in timing retirement. Our superannuation page has more on preservation age, TTR and access rules.

FAQ: Retiring at 60 with $280K in Australia

Can I retire at 60 with $280K in Australia? For a single homeowner spending around $28,000 to $30,000 a year, yes. $280K in an account-based pension at 5% net return can bridge the seven-year gap to the Age Pension at 67, leaving around $132,000 at pension age. It funds a modest retirement, not a comfortable one in ASFA’s terms, but it is workable for the right circumstances.

How long will $280K last in retirement from age 60? At $28,000 to $30,000 a year spending and 5% net return, approximately seven years before drawing down significantly, at which point the Age Pension supplements income. With near-full pension entitlements from 67, the combined income can sustain a homeowner well into their 80s.

Is it worth waiting to retire if I have $280K at 60? Often yes, even by one or two years. Two more years of employer contributions and compounding can add $55,000 to $60,000 to your balance before retirement, reduce drawdown years before the Age Pension and significantly improve spending comfort throughout retirement. Whether the trade-off is worth it depends entirely on personal circumstances.

What is a transition to retirement pension and should I use one? A TTR pension lets you access up to 10% of your super each year from preservation age (60) while still working. Many people use it to reduce hours without reducing income by drawing from their TTR pension while salary sacrificing more into super. Whether it is the right strategy for your situation depends on your income, tax position and fund. Speaking with a financial adviser before setting one up is worth doing.

Will I get the Age Pension if I retire at 60 with $280K? Almost certainly by 67. Drawing down over seven years from $280K typically leaves a balance well under the full pension assets test threshold for a single homeowner, currently around $314,000 (May 2026). Your home is exempt from the assets test.

What is the Age Pension rate for a single person in 2026? Approximately $29,754 a year including supplements, as at May 2026. Updated each March and September by the government. Check current rates at Services Australia.

What lifestyle does $280K support in retirement at 60? For a single debt-free homeowner, a modest lifestyle covering essentials, healthcare, some local activities and limited travel. Below ASFA’s $35,199 modest standard, but achievable for homeowners whose actual spending is lower than the benchmark figure.

Is $280K enough for a couple to retire at 60? As a combined balance, it is very tight. ASFA’s modest lifestyle standard for a couple is $50,866 a year and the seven-year gap before pension eligibility makes this difficult to sustain on $280K combined. For couples in this position, delaying retirement or having one partner continue part-time work generally makes the outcome substantially more comfortable.

What to Do Next

If you are approaching 60 with around $280K in super, the clearest thing you can do is model both options, retiring now versus working another one to two years, with your actual numbers rather than general projections. The difference is large enough that it is worth understanding before you decide.

Not sure where your retirement stands? or take the free Wealthlab retirement quiz z for a general read on your retirement position. Or book a free, no-pressure chat with the Wealthlab team to talk through your numbers with someone who works through this every day.