You might have seen the ads: “compare the pair,” “profits go to members,” smiling people running on beaches.

But the reality behind the super fund landscape is a bit more complex — and, in our view, deserves a closer look.

Podcast Spotlight: Industry Super – A Bubble About to Burst?

This month on the podcast, we unpack the history, structure, and investment challenges facing industry super funds — and why, for most of our clients, we’ve chosen a different path.

🎧 Listen to the episode here: youtu.be/YzNUYF8ezAU

Why this matters:

At Wealthlab, over 80% of our client base now use retail super funds — and there’s a reason for that. While industry funds played an important role in Australia’s retirement system, the landscape has changed. Many of these funds have become enormous — with tens of billions under management — and that scale comes with challenges:

Slower response to market shifts

Performance drag from “herding” large sums

Limited personalisation or visibility for individual member

Why retail funds often make more sense for our clients:

In our experience, retail funds offer:

More flexibility and transparency

A structure where your money is actually invested in your name

Tools and strategies that let us tailor the setup to your goals — not just your age bracket

To be clear, this doesn’t mean industry funds are “bad.” In fact, some of our clients still hold them when it makes sense — for insurance, simplicity, or consolidation purposes.

But if you’ve worked with us, chances are you’re already in a retail fund, and this episode breaks down the why behind that move.

What we cover in the episode:

Where industry funds came from (hint: unions and the 1980s)

What changed after APRA’s performance testing crackdown

How “too much money” actually becomes a problem

Why being just another number in a billion-dollar pool affects your retirement outcomes

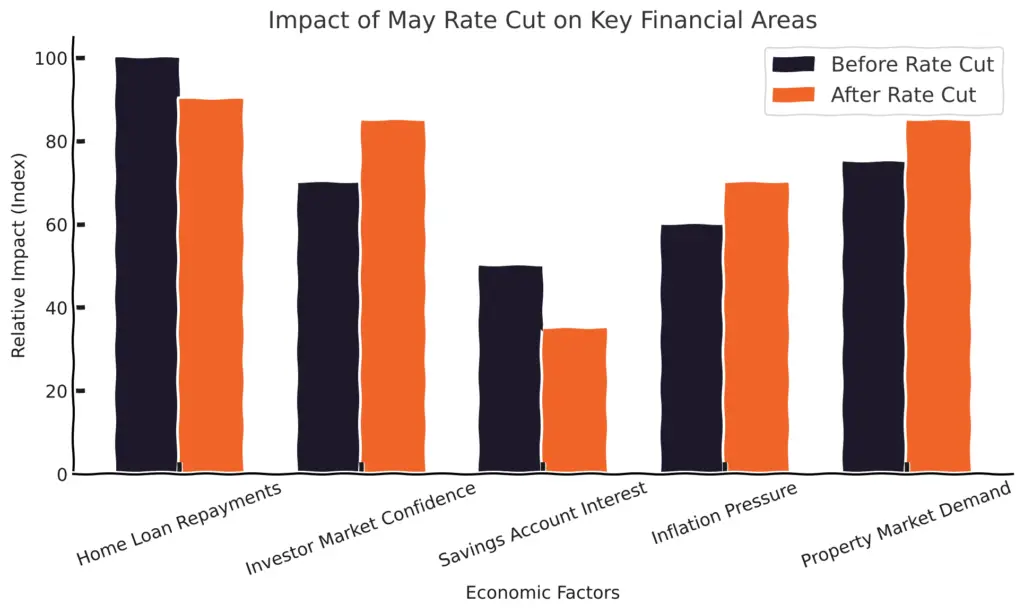

Bonus Breakdown: Interest Rate Cuts — What’s the Real Impact?

The RBA cut rates by 25 basis points this May, bringing the cash rate to 3.85%. It’s a shift that could affect a number of everyday financial decisions:

For homeowners:

→ Some lenders may pass on the cut, reducing repayments — a good moment to check your rate and options.

For investors:

→ Lower rates may support short-term optimism in markets, but they’re also a reminder to stay grounded in long-term strategy.

For people with cash savings:

→ With interest rates lower, some may reconsider leaving too much sitting in cash if it’s not keeping pace with inflation.

Final Thoughts

If you’ve already worked with us — this episode may give you some insight into why we made the switch to a retail fund with you.

If you haven’t yet — and your super still feels vague, generic, or out of your control — this might be your sign to take a closer look.

We’ll break it down in plain English. No pressure, no product-pushing, no beach-running extras.