Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. They assume a balanced investment return of approximately 5% per annum after fees. Individual outcomes will vary based on personal circumstances, investment returns, fees, and current government policy. This is general information, not personal advice.

Where $475K sits against the retirement benchmarks

The ASFA Retirement Standard (lump sums updated February 2026) sets the recommended super balances at 67 for homeowners at $630,000 for a comfortable single retirement and $730,000 for a couple. For a modest retirement, the recommended lump sums drop to $110,000 single and $120,000 couple because the Age Pension covers most modest-level spending.

$475,000 sits well above the modest benchmark and about $155,000 below the comfortable single target. As a couple with $475K combined, you are $255,000 below the comfortable couple benchmark, which is a more substantial gap.

For context on where $475K sits nationally, the average super balance for Australians aged 60 to 64 is approximately $381,000 for men and $301,000 for women, based on ASFA’s analysis of ATO data. With $475K, a single man sits about $94,000 above the male average, and a single woman sits about $174,000 above the female average. This is a stronger than average position heading into retirement.

The important caveat: the ASFA benchmarks assume you retire at 67, not 60. Retiring seven years earlier means your super has to fund those extra years before the Age Pension arrives, so a balance that would work at 67 needs tighter management at 60.

The $25K short of $500K reality

$475K is worth thinking about specifically because it sits just below the psychological threshold most Australians mentally target. Many people arrive at 60 with balances in the $460K to $490K range and mentally categorise this as “not quite there” territory.

The practical reality: the difference between $475K and $500K, over a 25 to 30 year retirement, is not the difference between success and failure. It might mean $1,000 to $2,000 less annual retirement income once averaged across the full retirement, or it might mean the money runs out three or four years earlier at the same spending level. It matters, but it does not change the shape of the plan.

What does change the shape at this level is:

- Whether you own your home outright

- Your spending discipline in the gap years between 60 and 67

- Your investment mix through retirement

- Whether you can extend work by a year or two (which we cover below)

How long will $475K super last in retirement?

The answer depends almost entirely on your annual spending, and whether you own your home outright.

| Annual spending | How long $475K lasts on its own | Age super runs out |

|---|---|---|

| $30,000/year | 21 to 24 years | Early to mid 80s |

| $37,000/year | 14 to 17 years | Mid to late 70s |

| $45,000/year | 10 to 12 years | Early 70s |

These figures assume you draw from super only, with no Age Pension until 67. Once the pension starts at 67, your required drawdown from super drops significantly and the remaining balance stretches much further.

The pattern we generally see at this balance level: spending in the $30,000 to $35,000 range through the gap years bridges you to 67 with a useful balance still invested. Spending above $42,000 in that period puts real pressure on the plan.

The 60 to 67 gap: seven years your super carries alone

This is the stretch where a $475K retirement either works or gets tight. From 60 you can access super tax-free (provided you meet a condition of release). But the Age Pension does not start until 67. That is seven years where your super has to cover everything.

Drawing $33,000 a year from age 60 with modest investment returns means consuming roughly $190,000 to $215,000 before the Age Pension begins. That leaves you arriving at 67 with a balance in the range of $260,000 to $290,000, before accounting for the growth still happening on the invested portion.

Scott and Phil walked through the reality of the gap years in Episode 19 of the Wealthlab Podcast: Is Early Retirement a Trap? The $150K Gap Most Aussies Miss. Their finding was that retiring even one year earlier can materially shift the numbers, and that the average couple retiring today has around $540,000 combined, roughly $190,000 below the ASFA comfortable target. For $475K balances, the margin sits close to this pattern.

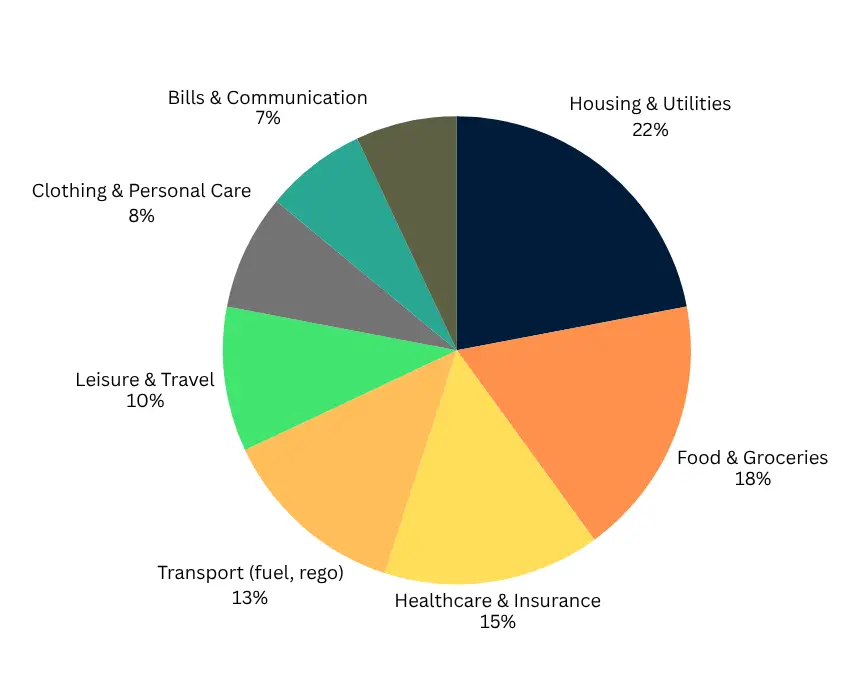

Sample Retirement Budget: Living on $30K/Year

Here’s how a modest retirement budget might break down:

| Category | % of Budget |

|---|---|

| Housing & Utilities | 22% |

| Food & Groceries | 18% |

| Healthcare & Insurance | 15% |

| Transport (fuel, rego) | 13% |

| Leisure & Travel | 10% |

| Clothing & Personal Care | 8% |

| Bills & Communication | 7% |

| Other Essentials & Buffer | 7% |

How much Age Pension will you get with $475K at 67?

From 20 March 2026, the full Age Pension pays $1,200.90 per fortnight for singles ($31,223 a year) and $1,810.40 per fortnight for couples combined ($47,070 a year). A single homeowner with assessable assets under $321,500 qualifies for the full pension. For homeowner couples, the full pension threshold is $481,500 combined.

Source: Services Australia. These figures are set by the Australian Government and are updated each March and September.

Here is what that means specifically at $475K. If you draw around $33,000 a year between 60 and 67, you would likely arrive at 67 with $260,000 to $290,000 remaining. For a single homeowner, that sits below the $321,500 full pension assets threshold, which usually means the full Age Pension of $31,223 a year applies from day one of eligibility.

Combined with a modest drawdown from your remaining super, that produces a total retirement income of $38,000 to $41,000 a year, indexed with pension movements. For a homeowner couple with $475K combined arriving at 67 with around $260,000 left, the couple assets test threshold of $481,500 means the full couple Age Pension of $47,070 is likely, subject to the income test.

One of the structural realities of retiring at a balance in this range is that the assets test tends to work in your favour by the time you reach 67, because your super has been partially drawn down. Phil and Dan walked through how the assets test and income test interact using real case studies in Episode 10 of the podcast, and Scott and Phil covered commonly missed Age Pension opportunities in Episode 20.

$475K single vs $475K as a couple

These two scenarios play out differently.

As a single homeowner at 60, $475K is above the individual male average and well above the female average. It supports a modest retirement lifestyle for most people. Gap-year spending of $30,000 to $33,000 is where the plan generally holds together. Once the single Age Pension of $31,223 kicks in at 67, it becomes the anchor of your retirement income with your remaining super topping it up.

As a couple with $475K combined, the picture is tighter. The ASFA comfortable couple benchmark is $730,000, so $475K combined sits $255,000 below that target. Sustainable combined spending in the gap years is generally $38,000 to $44,000. The offset is that the couple Age Pension of $47,070 a year is substantially higher than the single rate, so from 67 the couple pension carries a bigger share of the load.

For single women specifically, $475K sits well above the female average of $301,000. But the longer female life expectancy (average 85 vs 81 for men) means the plan needs to stretch further. Scott and Phil covered the specific challenges women face with super balances and retirement timing in Episode 17 of the podcast.

What’s the best way to invest $475K for retirement income?

The best way to invest $475K in retirement generally comes down to three principles: keep some growth in the portfolio, manage sequencing risk carefully through the gap years, and avoid the temptation to shift entirely to cash.

Setting up an account-based pension is a common structure for retirees at 60. Rolling super into an account-based pension provides regular, tax-free income from age 60, keeps the money invested, and controls the drawdown rate. It is also generally treated more favourably under the Age Pension means test than lump sums held elsewhere. Our pension and Centrelink page covers this in more detail.

Keeping growth assets in the mix matters at $475K because the margin for error is smaller than at higher balances. Scott and Phil showed in Episode 1 of the podcast: Why Playing It Safe in Retirement Can Cost You More that a growth portfolio expecting 6 to 7% per annum can fund a couple with $500K in super into their late 90s, while the same couple with a conservative portfolio at 3 to 4% runs out 15 years earlier. On $475K, that difference between growth and conservative is what determines whether the money makes it through a 25 to 30 year retirement.

Phil also flagged in Episode 22 that most funds label their default option “balanced” when it actually holds 70% or more in growth assets. It is worth checking what your fund’s balanced option actually contains, because the label often does not match the underlying investment mix.

Holding one to two years of expenses in cash is a common way to manage sequencing risk. If markets drop 20% in the first year of retirement, drawing from cash rather than selling investments at a loss protects the long-term balance. The cash buffer gets topped up when markets recover.

Diversified index funds or a well-managed balanced option give broad market exposure without the concentration risk of individual stocks or a single investment property. At $475K, there is limited room for a concentrated bet that goes wrong.

Want to see how your numbers play out? Try the free Wealthlab super calculator to model your balance, spending, and Age Pension together.

How $475K plays out year by year

Here is an illustrative projection for a single homeowner spending $33,000 a year, with a balanced investment return of 5% per annum:

| Age | Super balance (approx.) | Drawdown from super | Age Pension | Total income |

|---|---|---|---|---|

| 60 | $475,000 | $33,000 | $0 | $33,000 |

| 63 | $375,000 | $33,000 | $0 | $33,000 |

| 67 | $265,000 | $7,000 | $31,000 | $38,000 |

| 72 | $240,000 | $7,000 | $31,000 | $38,000 |

| 80 | $180,000 | $7,000 | $31,000 | $38,000 |

| 85 | $145,000 | $7,000 | $31,000 | $38,000 |

These numbers are approximate and assume steady investment returns (real markets are lumpier). Drawdowns usually rise with inflation over time, so the pattern here is illustrative rather than exact. The important point is the shape of the plan: your super carries the full load between 60 and 67, then the Age Pension takes over as the main income source and your remaining super becomes the top-up.

Retiring at 60 vs 62 vs 65 with $475K

For someone at $475K at 60, the “one more year” question has real financial weight because each additional working year produces three stacked effects:

- Additional employer Superannuation Guarantee contributions at 12% of your earnings

- Compounding investment growth on the full balance you have not touched yet

- Fewer years of gap-year drawdown before the Age Pension arrives

Here is a rough illustrative comparison for someone earning $90,000 with $475K at 60:

| Retirement age | Approximate super at retirement | Years of gap-year drawdown | Balance arriving at 67 (approx.) |

|---|---|---|---|

| 60 | $475,000 | 7 years | $260,000 to $290,000 |

| 62 | $530,000 to $555,000 | 5 years | $355,000 to $385,000 |

| 65 | $600,000 to $650,000 | 2 years | $475,000 to $520,000 |

Working two more years typically shifts you close to the psychological $500K threshold at retirement and materially better balance heading into the pension years. Working to 65 typically shifts you within striking distance of the ASFA comfortable single benchmark of $630K.

Part-time or consulting work in those extra years is often the best of both worlds. Even 2 to 3 days per week generates income that removes the need to draw down super, while making the transition to full retirement less abrupt. Our post on the average super balance at 60 covers where $475K sits relative to the national picture in more detail.

Six strategies that generally make $475K stretch further

Part-time work in the gap years. Even $12,000 to $15,000 a year from casual or consulting work takes real pressure off the super drawdown. Two to three years of light work at this balance often adds a decade to how long the money lasts.

Controlled spending in the gap window. The 60 to 67 window is where this balance is under the most pressure. Spending in the $30,000 to $35,000 range for singles, or $38,000 to $44,000 for couples, is where we generally see the plan hold together.

Planning for the Age Pension from day one. At $475K, the Age Pension is not a small supplement. It is a core piece of the plan. Structuring drawdowns and asset allocation with pension eligibility in mind generally produces a better long-term result than treating super and pension as separate systems.

Healthcare cost planning. A healthy 60-year-old spends very little on healthcare. Specialists, medications, and procedures typically add up from the mid-70s onward. Episode 19 noted that healthcare consumes around 34% of lifetime retirement savings on average, with the final 24 months of life accounting for 50 to 80% of total lifetime healthcare spend.

Age Pension application timing. Services Australia accepts applications up to 13 weeks before you turn 67. Getting the paperwork in early avoids missing weeks of payments while your claim is being processed.

Downsizer contributions worth understanding. For homeowners with $475K in super and a valuable family home, the downsizer contribution rules let you put up to $300,000 per person ($600,000 per couple) from a home sale into super. Scott and Phil walked through the traps in Episode 2 of the podcast, including the 90-day deadline and how converting an exempt asset (the family home) into an assessable one (cash) affects Age Pension eligibility.

Retirement age in Australia: the three ages that matter

There is no compulsory retirement age in Australia. Three specific ages shape the retirement system:

Preservation age (60): When you can access your super tax-free, provided you meet a condition of release. For anyone born after 1 July 1964, preservation age is 60.

Age 65: Super becomes fully accessible regardless of employment status. No condition of release is required at 65.

Age Pension age (67): When you become eligible for the Age Pension, subject to means testing. Applies equally to men and women.

Scott and Phil covered the common myths around preservation age and retirement definitions in Episode 18 of the podcast, including the difference between preservation age and actual retirement, and how the “10 hours per week” test applies to conditions of release.

Frequently asked questions

Is $475K enough to retire at 60 in Australia?

For homeowners with modest spending expectations, yes. $475K sits well above the average super balance for Australians aged 60 to 64 and well above the ASFA modest benchmark. It falls short of the comfortable target ($630,000 for a single homeowner at February 2026), so your lifestyle sits between modest and comfortable, depending on how you manage the gap years.

How long will $475K super last at 60?

At $33,000 a year with balanced investment returns of around 5% per annum, $475K on its own lasts roughly 15 to 18 years. With the full Age Pension supplementing from 67, total retirement funding usually extends into the mid to late 80s or beyond.

How much Age Pension will I get with $475K at 67?

If you draw around $33,000 a year from super between 60 and 67, you would likely arrive at 67 with $260,000 to $290,000 remaining. For a single homeowner, that sits below the $321,500 full pension assets threshold at March 2026, which usually means the full Age Pension of $31,223 a year applies. For a homeowner couple with $475K combined and a similar balance at 67, the assets test threshold of $481,500 also generally means the full couple pension of $47,070 applies, subject to the income test.

What’s the best way to invest $475K in Australia for retirement?

For most retirees at this balance, an account-based pension with a balanced investment mix (around 60% growth, 40% defensive) is a common structure. It keeps the money invested, provides tax-free income from age 60, and allows control over the drawdown rate. Holding one to two years of expenses in cash helps manage sequencing risk. Sitting fully in cash is generally avoided at this balance because it tends to lose real purchasing power over a 25 to 30 year retirement.

Can a couple retire at 60 with $475K combined?

It is tighter than at higher balances, but workable for homeowner couples with modest spending expectations. Combined spending of $38,000 to $44,000 through the gap years, plus the full couple Age Pension of $47,070 from 67, generally supports a modest retirement lifestyle indefinitely for homeowners.

Is $475K enough if I’m still renting?

Renting adds $18,000 to $25,000 or more per year to retirement costs, which significantly compresses how far $475K stretches. The non-homeowner assets test threshold is higher ($579,500 for singles at March 2026), so renters may qualify for a larger part pension, but the ongoing rent cost usually outweighs that advantage. For renters at 60 with $475K, working a few more years or reducing housing costs before retirement generally makes a material difference.

Should I work another year or two if I’m at $475K?

At $475K, the “one more year” question has real weight. Two more working years at $90,000 typically adds around $55,000 to $80,000 to your super at retirement through employer contributions and compounding growth, plus you avoid two years of gap-year drawdown. Whether it is worth it depends on your health, work satisfaction, and lifestyle priorities, but the numbers themselves are meaningful.

How much super should I have at 60 in Australia?

The ASFA target for a comfortable retirement at 67 is $630,000 for singles and $730,000 for couples (February 2026 figures). At 60, working backwards, that suggests $500,000 to $600,000 for a single person targeting a comfortable retirement. Most Australians retire with less than these targets, which is why the Age Pension is designed to supplement retirement income for the majority of retirees.

Can I retire earlier than 60 with $475K?

Not usually, because super cannot be accessed before preservation age (60 for anyone born after 1 July 1964) unless you meet a specific condition of release such as severe financial hardship. Retiring before 60 typically requires alternative savings outside super to fund the gap between when you stop working and when super becomes accessible.

Your next step

$475,000 at 60 is a genuinely workable retirement position for homeowners, particularly single homeowners. It sits close enough to the psychological $500K threshold that small adjustments (spending discipline, investment mix, or working one to two more years) can shift the outcome meaningfully. The fundamentals are the same as at higher balances: control the drawdown, keep some growth in the portfolio, and understand how everything shifts once you reach 67.

Wealthlab works with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how the general principles here might apply to your circumstances.

To compare how the numbers shift at nearby balances, our posts on Can I Retire at 60 with $450K? and Can I Retire at 60 with $500K? cover similar ground.