The short answer: probably not in the way most people picture it, and not because $400K is too small. The bigger issue is that you can’t actually touch your super at 55. For anyone born after 1 July 1964, the preservation age is 60. That means a 55 year old retiring today has a gap of at least 5 years before they can access their super, and another 7 years after that before the Age Pension kicks in at 67.

So the real question isn’t “is $400K enough to retire on at 55?” It’s “can I bridge 12 years on $400K plus whatever I have outside super?” That’s a very different question, and the answer depends on what else you have to work with.

This post walks through the real numbers, the rules that trip people up, and the strategies people in this position actually use.

You Can’t Access Your Super at 55

This is the part most “retire at 55” articles skip past. Australian super has a preservation age, which is the minimum age you can access your balance, and for everyone retiring now or in the next decade, that age is 60.

According to Services Australia, preservation age is:

- 55 for people born before 1 July 1960 (already past)

- A sliding scale between 55 and 60 for those born July 1960 to June 1964

- 60 for anyone born after 30 June 1964

If you’re 55 today (May 2026), you were born around 1971. Your preservation age is 60. There’s no path to your super at 55 outside very narrow exceptions like terminal illness, severe financial hardship, or compassionate grounds.

Phil walked through this in our podcast episode Is 61 the New Retirement Age in Australia? and put it bluntly: “Preservation age does not mean you automatically have access to super, but it means you’re of an age where you can start ticking boxes.” At 55, you’re not even at the door.

The Real Question: Can $400K Bridge to 60, Then to 67?

If you walk away from work at 55 with $400K in super and nothing else, you’ve got two problems to solve:

Years 1 to 5 (age 55 to 60): The $400K is locked in super. Living expenses have to come from somewhere else. Years 5 to 12 (age 60 to 67): Your super is accessible, but the Age Pension hasn’t started. Age 67 onwards: Age Pension can begin (subject to assets and income tests), and super continues to support your spending.

The $400K will sit in super, untouched, for those first 5 years. With reasonable investment growth of say 6 to 7% per annum on a balanced or growth portfolio, $400K could grow to roughly $535K to $560K by the time you turn 60, assuming no further contributions and ignoring fees. That gives you a stronger starting position for years 5 to 12.

But you still need to fund years 1 to 5 without touching it. That’s where outside-super assets, part-time work, or a partner’s income matter enormously.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees, and current government policy. This is general information, not personal advice.

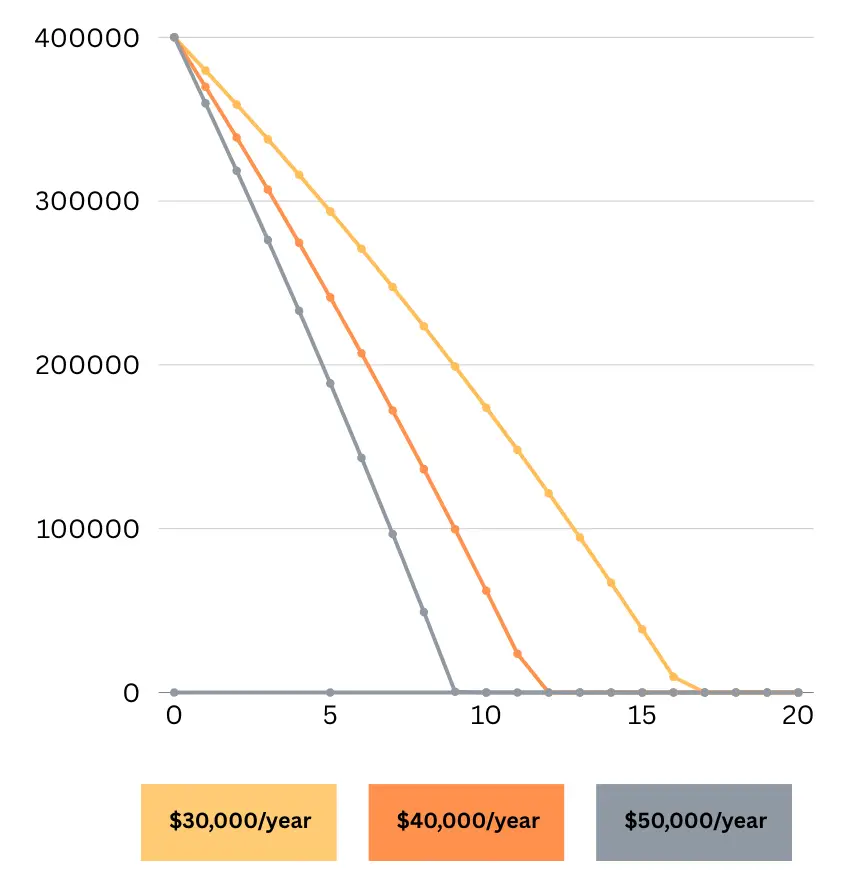

Graphice: This chart illustrates how a $400,000 super balance would deplete over time starting at age 60, depending on your annual spending.As shown, your annual lifestyle costs have a major impact on how long your super will sustain you.

How $400K Compares to What’s Considered “Enough”

According to the ASFA Retirement Standard, updated February 2026, the lump sums for a comfortable retirement at 67 are:

- $630,000 for a single homeowner

- $730,000 for a homeowner couple

For a modest retirement, ASFA estimates around $100,000 for both singles and couples, because most of a modest lifestyle is funded by the Age Pension.

The annual income those balances are designed to support, based on the ASFA December 2024 quarter expenditure breakdown, is roughly $51,805 a year for a comfortable single and $73,077 for a comfortable couple. A modest single needs around $32,897 a year, a modest couple around $47,470.

$400K at age 55 sits between modest and comfortable territory, especially if you’re a homeowner. It’s not a hopeless number. But it was designed to support spending from 67 onwards, not from 55. Pulling 12 years earlier changes the maths significantly.

For context, the average male super balance at ages 55 to 59 is roughly $319,743 and the average female balance is $242,945, according to ATO data analysed in late 2025. So $400K at 55 is actually above average. The problem isn’t that you’re behind on super. It’s that the system isn’t built for accessing it at 55.

What Most People in This Position Actually Do

In practice, we generally find that people targeting retirement at 55 fall into a few groups:

Group 1: Have non-super assets. A paid-off home, an investment property, shares outside super, or a meaningful inheritance. These assets can fund the 5 year gap to preservation age. Without something here, retiring at 55 on $400K super alone is very tight.

Group 2: Semi-retire rather than fully retire. Drop to 2 or 3 days a week, take contract work, or shift to something lower stress. The work bonus doesn’t apply yet (that’s an Age Pension feature) but any income reduces the drawdown on outside savings until preservation age.

Group 3: Stop work and live very lean for 5 years. Possible if the lifestyle goal is modest, the mortgage is paid off, and there are no dependants. Not many people find this realistic once they actually run the numbers.

Group 4: Wait the extra 5 years. The most common outcome we see. Working from 55 to 60, even part-time, makes a substantial difference. Continuing to contribute via concessional contributions, particularly using catch-up rules for those with balances under $500,000, can lift a $400K balance materially before preservation age.

We had a client recently in this exact position. Mid-50s, $390K in super, wanting to step away. After working through the numbers, they shifted to three days a week instead of fully retiring. That kept some income coming in, let them keep contributing to super through the concessional cap, and meant the $390K kept growing untouched. Five years later they have a much stronger position than they would have walking away at 55.

The Age Pension Side of the Equation

Even if you retire at 55, the Age Pension doesn’t start until 67. After the March 2026 indexation, the maximum Age Pension is $1,200.90 per fortnight for a single person (around $31,223 a year) and $1,810.40 per fortnight combined for a couple (around $47,070 a year), according to Services Australia.

These figures are set by the Australian Government and are typically updated each March and September.

To qualify for the full pension under the assets test from 20 March 2026, a single homeowner needs assessable assets below $321,500. A homeowner couple needs assessable assets below $481,500. Above those thresholds, the pension reduces by $3 a fortnight for every $1,000 of additional assets.

A homeowner with $400K in super at 67 would generally receive a part Age Pension, not the full rate. The interaction between super, the Age Pension, and your spending plan is what most retirement planning hinges on, and it’s worth running specific numbers rather than guessing.

If you want a quick snapshot of how your numbers fit together, the free Wealthlab super calculator takes a couple of minutes and gives you a much clearer picture than averages ever can.

Strategies That Can Help If You Want to Retire Earlier

A few options worth understanding if early retirement is the goal:

Transition to Retirement (TTR) at 60. Once you reach preservation age but haven’t fully stopped working, a TTR pension lets you draw between 4% and 10% of your super balance each year while you keep working. Earnings inside a TTR are still taxed at 15%, but it can free up cash flow and let you reduce hours.

Catch-up concessional contributions. If your super balance is below $500,000 at 30 June of the previous financial year, you can use unused concessional cap amounts from the previous 5 years. Phil walked through a real example of this on the podcast where a client used catch-up contributions to drop their capital gains tax bill from $98K to $11K. The same mechanism can be used to boost a balance in the final working years.

Sequencing your decisions. If you have an investment property or other CGT asset, the timing of when you sell can have a major tax impact. Selling in a working year is usually more expensive than selling in the first year of retirement when income drops.

Reviewing your investment mix. Scott and Phil unpacked this in our episode on growth versus conservative portfolios. A common worked example: a couple with $500K spending $75K a year. A growth portfolio funded retirement to their late 90s. A conservative one ran out 15 years earlier. Risk tolerance matters, but so does running out of money.

For more on when you can actually access your super, see our guide on preservation age and conditions of release. For where $400K sits compared to other balances, see the average super balance at 60 in Australia.

Frequently Asked Questions

Can I access my super at 55 in Australia?

No, not unless you were born before 1 July 1960. For anyone born after that date, the preservation age has been raised over time, and for everyone born after 30 June 1964 it sits at 60. At 55 today, your super is preserved and cannot be accessed except through very narrow exceptions like terminal medical condition, permanent incapacity, severe financial hardship, or compassionate grounds.

Is $400K in super enough to retire on?

$400K is above the average super balance for Australians aged 55 to 59 and well below the ASFA comfortable retirement target of $630,000 for a single homeowner and $730,000 for a homeowner couple. Whether it’s “enough” depends entirely on your home ownership, partner status, spending plans, and how many years it needs to last. Combined with a part Age Pension from age 67, $400K can support a modest to mid-range retirement for many homeowners. Individual circumstances vary substantially.

What is the Age Pension age in Australia?

The Age Pension age is 67 for all Australians born on or after 1 January 1957. It reached 67 on 1 July 2023 after a staged increase from 65. There is no current proposal to raise it further.

Can I retire early and live off non-super assets until I reach preservation age?

Yes, this is one of the more common paths to retiring before 60. You use savings, investment property income, share dividends, or other non-super assets to fund the gap years before you can access your super. The risk is that drawing heavily on outside assets in your 50s can leave you with too little to draw on later. Running scenarios with a financial adviser before making the leap helps to test whether the plan holds up over a 30 or 40 year retirement.

How much income does $400K in super produce in retirement?

Using a conservative 4 to 5% drawdown rate, $400K can generate around $16,000 to $20,000 a year of income before the Age Pension is considered. Combined with the maximum Age Pension at 67 ($31,223 a year for singles or $47,070 combined for couples after March 2026 indexation), this can lift total income meaningfully. Drawdown strategies, market returns, and longevity all change the picture.

Should I keep working until 60 to access super?

This is one of the most common questions we get from people in their mid-50s. There’s no one right answer. Working five extra years adds contributions, allows the existing balance to keep growing, and shortens the period your money needs to last. But health, energy, family circumstances, and personal goals all matter too. Many people find that a phased approach (full time to part time to retirement over a few years) works better than a hard stop at 55.

Talk Through Your Numbers

If you’re 55 and seriously considering retirement, the numbers are worth running properly rather than guessing. Want to talk through how this works for your situation? Book a free chat with the Wealthlab team. No pressure, no jargon, just clarity on where you actually stand.

You can also Take the free Wealthlab retirement quiz for a quick snapshot of your current position.