Short answer: yes, for many Australians, $600K at 60 is enough to retire on, especially if you own your home and your annual spending sits in the $45,000 to $55,000 range. It funds a modest to mid-comfortable lifestyle through to Age Pension age, then transitions into a blend of super and pension income from 67.

The longer answer is more honest. $600K is below ASFA’s current benchmark of $630,000 for a single comfortable retirement, and well below the $730,000 figure for a couple. That doesn’t mean retirement isn’t possible. It just means how you spend, how your money is invested, and when the Age Pension kicks in all matter more than they would on a larger balance.

This guide walks through the 2026 numbers, how long $600K realistically lasts at different spending levels, where the Age Pension takes over, and the planning decisions that make the biggest difference at this balance.

What Retiring at 60 with $600K Actually Means

Preservation age in Australia is 60 for anyone born after 30 June 1964. Hitting 60 doesn’t automatically give you access to your super. You also need to meet a condition of release. The most common one is leaving an employment arrangement and not intending to return to substantial work, which Services Australia generally interprets as fewer than 10 hours a week.

Once that box is ticked, your $600K can move into an account-based pension, where the earnings inside the fund are tax-free. That’s a meaningful shift from accumulation phase, where earnings are taxed at 15%.

The seven-year window from 60 to 67 is the real planning challenge. You’re drawing down without any Age Pension support, so your super has to carry the full load. After 67, the Age Pension can absorb a significant portion of your income needs and your super can ease off.

We see this a lot in practice. A client retires at 60 thinking they need their $600K to last to 95 with no help. Once we map in the part Age Pension from 67, the picture changes considerably. The super only has to fully fund roughly seven years, then it shares the load with the government for the rest.

Scott and Phil walked through exactly this on the podcast. Their example was a couple with $500K spending $75,000 a year. A growth portfolio kept funding through to their late 90s. A conservative one ran out 15 years earlier. The point being that asset allocation at 60 matters as much as the balance itself. Watch the episode on YouTube.

How Long Will $600K Last?

How long your money lasts comes down to two levers: how much you spend each year and how the money is invested.

Using a balanced investment return of around 6% per annum and 2.5% inflation, here’s a rough guide for a single retiree starting at 60, drawing from super only (no Age Pension factored in yet):

| Annual spending | Approximate years $600K lasts |

|---|---|

| $35,000 | 25 to 28 years |

| $45,000 | 18 to 20 years |

| $55,000 | 14 to 16 years |

| $65,000 | 11 to 13 years |

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees, and current government policy. This is general information, not personal advice.

The numbers improve once the Age Pension joins in from 67. At a spending rate of $45,000 a year, a single retiree drawing a part pension from 67 can typically stretch $600K into their late 80s or beyond, depending on how the pension entitlement plays out.

The biggest risk at this balance isn’t running out at 95. It’s spending too aggressively in the first five to seven years and depleting the balance before the Age Pension kicks in. That’s the window where every $5,000 a year of extra spending compounds into a meaningful shortening of your runway.

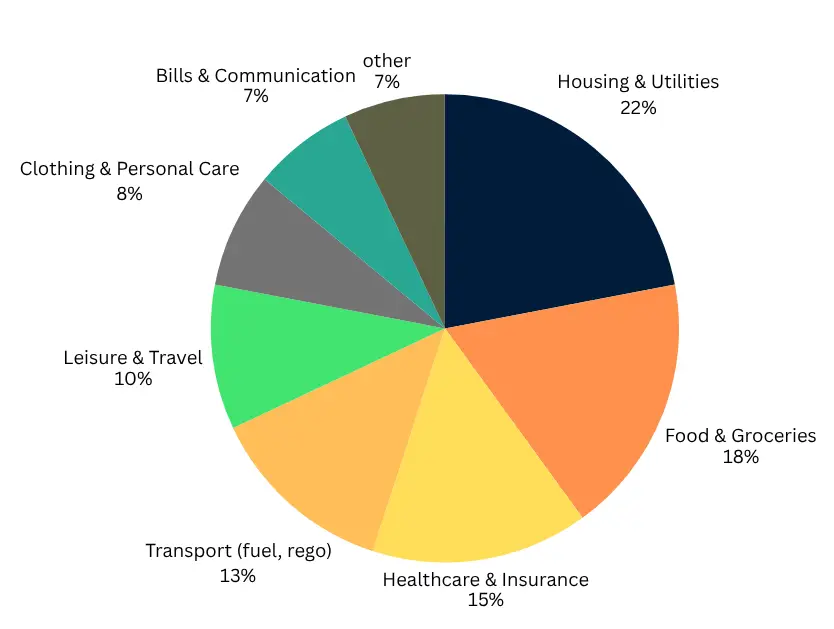

What a $30K/Year Budget Looks Like

Here’s how a retiree might distribute a $30K annual budget:

| Category | % of Budget |

|---|---|

| Housing & Utilities | 22% |

| Food & Groceries | 18% |

| Healthcare & Insurance | 15% |

| Transport | 13% |

| Leisure & Travel | 10% |

| Personal Care & Clothing | 8% |

| Bills & Communication | 7% |

| Miscellaneous & Buffer | 7% |

What $600K Looks Like Against the ASFA Standards

The Association of Superannuation Funds of Australia publishes benchmarks for what retirement actually costs. As at the September 2025 quarter:

| Lifestyle | Single (annual) | Couple (annual) |

|---|---|---|

| Modest | $35,199 | $50,866 |

| Comfortable | $54,240 | $77,375 |

ASFA’s current lump sum benchmarks (February 2026 update) are:

- Modest: $110,000 single / $120,000 couple

- Comfortable: $630,000 single / $730,000 couple

At $600K as a single retiree, you’re $30,000 short of the comfortable benchmark but more than five times the modest figure. As a couple, $600K combined puts you well above modest but well below comfortable. The realistic landing zone is somewhere in between, especially if you’re willing to spend a touch more before 67 and let the Age Pension lift you toward the comfortable line later.

How the Age Pension Changes the Picture at 67

This is the single most under-appreciated lever for anyone retiring at 60 with $600K.

Maximum Age Pension rates from 20 March 2026 (Services Australia):

- Single: $1,200.90 per fortnight, or roughly $31,223 a year

- Couple combined: $1,810.40 per fortnight, or roughly $47,070 a year

By the time you reach 67, your super balance will likely be lower than $600K because you’ve been drawing on it for seven years. A lower balance means you’re more likely to qualify for at least a part Age Pension under the assets and income tests.

Combine a part pension of, say, $15,000 to $20,000 a year with super drawdowns of $25,000 to $35,000, and a single retiree is already in the $40,000 to $55,000 zone. That’s modest to mid-comfortable territory by ASFA’s standards. Plus the Pensioner Concession Card, which we see saving clients another $2,000 to $5,000 a year in concessions across PBS medications, utilities, and council rates.

For more detail on how the tests work in practice, our pension and Centrelink page breaks them down.

What $45,000 a Year Actually Buys in Retirement

A lot of the panic around retirement numbers comes from people underestimating how much of their working-life budget goes to mortgages, kids, and commuting. None of which apply in the same way at 60.

Roughly, $45,000 a year for a homeowner covers:

- Utilities, council rates, home and contents insurance

- Groceries, household essentials, and a reasonable food budget

- A modest car, registration, fuel, and maintenance

- Private health cover (basic to mid-tier)

- Out-of-pocket healthcare and medications

- A weekly meal or two out, hobbies, and an annual domestic holiday

- A buffer for one-offs and replacements

This isn’t extravagant, but for the right person, it’s a genuinely good standard of living. The retirees we see who do best on $600K aren’t the ones tracking every dollar. They’re the ones who got their fixed costs low before retiring and protected that base.

Where People at This Balance Get It Wrong

A few recurring themes from practice experience at this balance level:

Going too conservative too early. A common instinct at 60 is to switch everything to cash to “protect” the balance. The trade-off is that you also lock in lower long-term returns at exactly the point when you need the money to last 25 to 30 years. The podcast example of the couple with $500K spending $75,000 illustrates this well. Same average return, but a defensive portfolio paired with a long retirement runs out years earlier.

Front-loading spending. The first few years of retirement often feel like the longest holiday of your life. Travel, renovations, helping the kids. By itself that’s fine. The risk is locking in habits that need to last another 20 years on a balance that won’t.

Ignoring healthcare in the later years. ABS and AIHW data suggests a meaningful portion of lifetime healthcare costs are concentrated in the final years. Episode 19 of the podcast covered this in detail. Healthcare can consume around 34% of retirement savings, with the final 24 months often consuming 50 to 80% of total lifetime healthcare spend. Planning for that buffer matters.

Poor structuring around the Age Pension. Small decisions about how you hold your money, whether assets sit in super versus outside, the timing of large purchases, can shift Age Pension entitlement by thousands of dollars a year. Phil unpacked a case study on the podcast where timing the sale of an investment property and using catch-up contributions reduced CGT from $98,000 to $11,000. The principle applies to pension structuring too. Watch Episode 10 here.

Forgetting about Phil’s “income shock.” Phil talks about the anxiety that hits when the fortnightly income stops landing in your bank account. It’s not just emotional. It changes spending behaviour, often in ways that hurt the plan. Building an income stream that mimics the pre-retirement experience (a regular drawdown from your account-based pension) makes the shift easier.

Want to see how your own numbers stack up? Try the free Wealthlab retirement calculator for a quick snapshot of where you stand.

Who Can Retire at 60 With $600K?

You’re likely in a good position if:

- You own your home outright or have very low housing costs

- Your annual spending target sits between $40,000 and $55,000

- You’re comfortable maintaining a balanced or growth-oriented investment allocation through retirement, not switching everything to cash

- You’re willing to draw moderately from super between 60 and 67, then transition to a blended income with the Age Pension

- You’ve accounted for inflation, healthcare in later years, and one-off costs like car replacement and home maintenance

The picture gets tighter if you’re still paying off a mortgage at 60, want to spend significantly more than $55,000 a year, or expect to be financially supporting adult children. In those cases, working a couple of extra years, doing part-time work into your mid-60s (which the Work Bonus actually rewards), or downsizing the home are levers worth weighing up.

FAQ: Retiring at 60 With $600K

Can I access my super at 60? Preservation age is 60 if you were born after 30 June 1964. Reaching that age doesn’t automatically release your super. You also need to meet a condition of release, the most common being leaving an employment arrangement with no intention to return to substantial work (generally 10 or more hours a week).

Is $600K enough to retire on at 60 in Australia? For a single homeowner spending around $40,000 to $50,000 a year, $600K can fund retirement through to Age Pension age at 67 and beyond, particularly when combined with a part Age Pension from 67. For a couple, $600K is tighter and may require part-time work or downsizing to bridge the gap to comfortable.

How does the Age Pension affect retirement at 60? You can’t access the Age Pension until 67. From 60 to 67, your super carries the full income load. At 67, the Age Pension can provide up to $31,223 a year for singles or $47,070 for couples combined (current as at 20 March 2026). Most retirees with $600K will qualify for at least a part pension by their late 60s.

How long will $600K last in retirement? Spending $45,000 a year, $600K typically lasts 18 to 20 years from super alone. Once a part Age Pension kicks in at 67, the same balance can typically support a retiree into their late 80s or beyond, depending on investment returns, inflation, and pension entitlement.

Should I move my super to cash when I retire at 60? We generally find that retirees who stay invested in a balanced portfolio through retirement see better long-term outcomes than those who shift fully to cash. Cash limits the sequencing risk in the very early years but locks in lower returns across a retirement that could span 25 to 30 years. Investment strategy at this balance should be considered carefully with a qualified adviser.

What lifestyle does $600K support? For a single homeowner, $600K plus a future part Age Pension supports a modest to mid-comfortable retirement by ASFA standards. That means private health cover, a reasonable car, a couple of meals out a week, hobbies, and an annual domestic holiday with occasional overseas travel. It is not a luxury retirement.

What if I work part-time after retiring at 60? Part-time work can significantly extend how long your super lasts and reduce early-retirement drawdowns. From Age Pension age, the Work Bonus means a single pensioner can earn around $518 a fortnight in employment income before the pension is reduced at all. Earlier in retirement, part-time earnings simply mean lower super drawdowns.

Do I need more than $600K to retire comfortably at 60? ASFA’s current benchmark for a comfortable retirement is $630,000 for singles and $730,000 for couples. $600K is just below the single benchmark and substantially below the couple benchmark, so a “comfortable” retirement is at the edge of reach for a single person and tighter for a couple. Modest to mid-comfortable is realistic for most people at this balance.

What to Do Next

$600K at 60 is not the storybook retirement number you see in headlines, but it’s a balance that many Australians retire on every year and live well from. The decisions that matter most aren’t about the balance itself. They’re about spending discipline in the first seven years, investment allocation, how you transition into the Age Pension at 67, and whether your home and lifestyle are set up to keep fixed costs low.

If you’d like to talk through how the maths might work for your situation, have a chat with the Wealthlab team. No pressure, no sales pitch. Or for a quick general read on where you stand, Take the free Wealthlab retirement quiz