At $650K in super, you are in a stronger position than many Australians approaching retirement. This is the first balance in the Wealthlab series that sits above the ASFA comfortable retirement benchmark for a single person, which means the question shifts slightly. It is less “can I make this work?” and more “how do I structure this well so it lasts and I do not leave anything on the table?”

For a homeowner with sensible spending habits, $650K at 60 can support a genuinely comfortable retirement for most of the posts in this series, the honest framing involved caveats. Here, the more useful framing is about what the money can do, what risks to manage over a 25 to 30 year retirement, and how the Age Pension interacts with a balance at this level.

Where $650K Sits Against the Retirement Benchmarks

The ASFA Retirement Standard estimates a single homeowner needs around $595,000 in super (plus the Age Pension) to fund a comfortable retirement, and a couple needs around $690,000. (Source: ASFA)

At $650K, a single retiree sits above the comfortable benchmark. A couple with $650K combined is slightly below it, but not by much. For most single homeowners at this balance, the comfortable ASFA lifestyle is achievable across retirement with reasonable planning. For couples, it is close and supported by the couple Age Pension from 67.

The ASFA comfortable standard covers things like private health insurance, regular domestic and some overseas travel, good food, leisure activities, and a reasonable car. It is not a lavish lifestyle, but it is a good one. At $650K, that lifestyle is generally within reach for a homeowner who manages spending sensibly.

The 60 to 67 Gap and What $650K Can Carry

The same seven-year bridge to the Age Pension applies here as with lower balances, but the balance has more room to absorb it.

Drawing $45,000 to $50,000 a year from age 60, with investment returns in a balanced or moderately growth-oriented portfolio, means the balance reduces over the bridge years but does so more gradually than at lower balances. Seven years of drawdown at $47,000 a year with a 5% return means the balance at 67 might be somewhere in the range of $450,000 to $500,000, though actual outcomes depend heavily on returns and spending.

At that remaining balance, the Age Pension assets test is relevant. A homeowner with around $450,000 to $500,000 in super at 67 and no other significant financial assets would sit in part-pension territory under current thresholds. Some structuring decisions before and around retirement can affect where the assets test lands.

The key insight at $650K is that the balance is large enough to support a comfortable spending level through the bridge years without depleting severely, but thoughtful structuring still matters for the Age Pension outcome.

Please note: All figures, projections and scenarios in this article are approximate and for illustrative purposes only. Individual outcomes will vary based on personal circumstances, investment returns, fees and current government policy. This is general information, not personal advice.

The Age Pension at 67: A Top-Up, Not the Foundation

At $650K, the Age Pension plays a different role than at lower balances in this series. For someone retiring at 60 with $250K or $320K, the Age Pension is the income foundation that super bridges toward. At $650K, it is more likely to be a meaningful top-up that supplements a super-funded retirement income.

Current maximum Age Pension rates from 20 March 2026 are:

- Single: approximately $31,223 a year

- Couple (combined): approximately $47,070 a year

(Source: Services Australia, current as at March 2026. Rates are updated each March and September.)

Whether a retiree with $650K at 60 qualifies for any Age Pension at 67 depends on the remaining balance at that point and what other assets they hold. A homeowner who has drawn from $650K for seven years and arrives at 67 with a remaining balance of $450,000 to $500,000, with no other significant financial assets, would likely qualify for a part pension under current assets-test thresholds.

Even a part pension of $10,000 to $15,000 a year on top of super income is meaningful. It reduces the annual super drawdown, extends how long the balance lasts, and provides a reliable government-backed income floor.

Our Pension and Centrelink page explains how the assets test and income test work in practice. Episode 20 of the Wealthlab podcast, Don’t Miss These Age Pension Opportunities, covers strategies for optimising Age Pension entitlements that many retirees with higher balances overlook. Episode 9, When Super Fund Advice Can Cost You the Age Pension, is also worth listening to,the case study involves a retiree losing pension entitlements through poor structuring decisions, which is a real risk at any balance.

What Retirement Life Looks Like at $650K

For a homeowner drawing around $45,000 to $50,000 a year, the ASFA comfortable lifestyle is within reach. That covers:

- All household essentials, groceries and insurance

- Private health cover and routine medical costs

- A newer car and some room for upkeep and replacement

- Regular domestic travel and an overseas trip every few years

- Hobbies, dining out, and a reasonable level of discretionary spending

- A buffer for unexpected expenses

This is not an unlimited lifestyle, but it is a genuinely comfortable one. The reader asking about $650K is not asking whether they can afford food and bills, they are asking whether they can afford to stop work at 60 and still live well. For a homeowner, the answer is generally yes, with the right structure.

Where it can unravel is spending significantly above $50,000 in the early years of retirement, taking large lump sums for one-off purposes without thinking through the sequencing impact, or holding the super in an investment option that is too conservative and loses ground to inflation over 25 years.

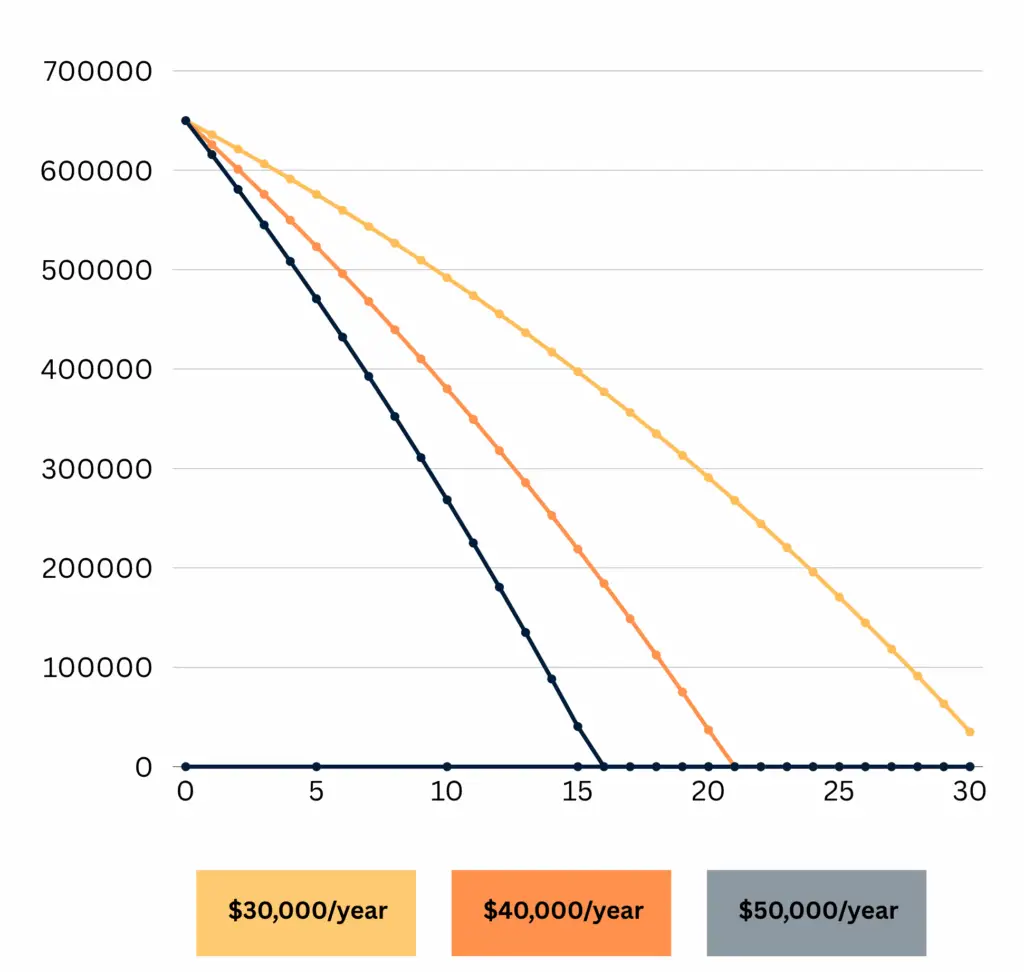

This Line Chart Show how $650K depletes under three annual spending scenarios $30K, $40K, and $50K per year over a 30-year period.

The Investment Mix Across a Long Retirement

At 60 with $650K and potentially 30 years of retirement ahead, the investment mix inside super matters more than many people realise. This is one of the more important points for retirees at this balance level.

A common default is shifting to a conservative or balanced option at retirement because it feels lower risk. The problem is that over 25 to 30 years, a portfolio with minimal growth exposure can lose purchasing power year by year. The money lasts longer in dollar terms but buys progressively less.

The Wealthlab podcast covered this directly in Episode 1: Why Playing It Safe in Retirement Can Cost You More. The episode worked through how a growth portfolio and a conservative portfolio with the same long-run average return produce dramatically different outcomes over 30 years based purely on when the bad years fall. For a $650K balance, the stakes of getting this wrong are higher in absolute dollar terms than at lower balances.

This does not mean all-growth is right for everyone at 60. It means the investment decision deserves deliberate thought rather than a default choice. Our superannuation page covers how Wealthlab approaches investment strategy in retirement.

What the Risks Look Like at $650K

At this balance level, the risks are different in character to the lower-balance posts. The question is less whether the money runs out and more whether it runs out earlier than it should because of avoidable mistakes.

Overspending in the first five to ten years. Early retirement often comes with new discretionary spending — travel, home improvements, lifestyle upgrades. A sustained spending level well above $50,000 a year in the early years draws the balance down more quickly than most projections assume, and the compounding effect of that plays out over decades.

Sequencing risk in a growth-oriented portfolio. A sharp market fall in the first two or three years of retirement, while drawing income from the portfolio, can permanently impair a balance even if the market recovers strongly. Having one to two years of income in a stable option as a buffer reduces the need to sell growth assets at a loss during downturns. The Wealthlab podcast covered sequencing risk in Episode 1.

Missing Age Pension entitlements through poor structuring. Many retirees at this balance assume they will not qualify for any Age Pension and never bother getting advice on structuring their assets. In practice, some decisions made in the years leading into retirement can meaningfully affect assets-test outcomes at 67. Episode 20 of the podcast, Don’t Miss These Age Pension Opportunities, is worth watching specifically for this.

Underestimating healthcare costs in later retirement. Healthcare spending tends to increase significantly from the mid-70s. Episode 19 of the podcast, Is Early Retirement a Trap? The $150K Gap Most Aussies Miss, noted that healthcare consumes around 34% of lifetime retirement savings on average, with the final two years of life accounting for the largest share. Building a realistic buffer for this is part of a sound retirement plan.

Run different scenarios through the free Wealthlab super calculator to see how your balance holds up under different spending and return assumptions.

A General Retirement Scenario

For a single homeowner at 60 with $650K in super and spending around $45,000 a year in a balanced investment mix:

- Age 60 to 67: Drawing from super while some investment growth offsets the drawdown. Balance reduces over this period, but the starting balance is sufficient to sustain this spending without significant depletion.

- Age 67+: Part Age Pension likely accessible depending on remaining balance and other assets. Combined income from pension and super drawdown potentially around $55,000 to $65,000 a year, depending on the means-test outcome.

- Later retirement: Healthcare costs rising from mid-70s is worth planning for. Spending can increase meaningfully in this period.

Individual outcomes vary considerably. This is an illustrative shape, not a projection for any specific person’s situation.

FAQ: Retiring at 60 with $650K in Australia

Can I retire at 60 with $650K in super? For many homeowning Australians with moderate spending habits, $650K at 60 is sufficient to support a comfortable retirement. This is the first balance in this series that sits above the ASFA comfortable retirement benchmark for a single person, which puts it in a meaningfully stronger position than the lower-balance posts. Individual circumstances vary.

How long will $650K last in retirement? At a sustainable drawdown rate with reasonable investment returns over 25 to 30 years, $650K can support comfortable retirement income for many people into their mid to late 80s, particularly once an Age Pension supplements the super from 67. Actual outcomes depend on investment returns, spending, fees and personal circumstances.

Will I qualify for the Age Pension with $650K at 67? It depends on the remaining super balance at 67, any other financial assets and the current assets-test thresholds. A homeowner who draws from $650K for seven years may arrive at 67 with a balance in partial pension territory depending on total assets. Eligibility is assessed by Services Australia. Figures are current as at March 2026.

What is the biggest financial risk at $650K in retirement? Overspending in the early years and poor sequencing of investment returns are the two most significant risks. A sustained spending level well above $50,000 a year, or a major market fall early in retirement without an income buffer, can shorten the retirement runway more than most people expect. Getting the investment structure right before retirement and setting realistic spending plans are the two most valuable things to address.

Is $650K enough for a couple to retire at 60? A couple with $650K combined sits slightly below the ASFA comfortable benchmark ($690,000 for couples). Combined with a couple Age Pension from 67, a comfortable retirement is generally achievable for homeowning couples at this balance with moderate spending. Individual circumstances vary.

Should I keep my super in growth or shift to conservative at 60? This depends on your risk tolerance, income needs and retirement timeline. Over a 25 to 30 year retirement, some growth exposure is generally beneficial to maintain purchasing power. A purely defensive portfolio can lose ground to inflation over time. Getting specific advice before making any changes is worthwhile.

Talk It Through with Wealthlab

If you are approaching 60 with around $650K and thinking about retirement, getting the structure right from the start tends to make the biggest difference. Investment mix, account-based pension setup, Age Pension positioning and drawdown strategy all interact, and decisions made early in retirement are harder to reverse later.

Wealthlab works with everyday Australians navigating exactly these questions. No jargon, no pressure. Book a free chat with the team to talk through how the general principles here might apply to your circumstances.

To compare how the numbers change at nearby balances, our posts on Can I Retire at 60 with $580K? and Can I Retire at 60 with $700K? cover similar ground.